Greater China Macro Daily(Beta Mode)

China Stocks Rise on Stimulus Hopes

Market Snapshot

| Asset | Level | Change |

|---|---|---|

| Shanghai Composite | 3,944.83 | +1.36% |

| CSI 300 | 4,517.52 | +1.52% |

| Hang Seng | 25,116.53 | -0.70% |

| TAIEX | 32,572.43 | -1.82% |

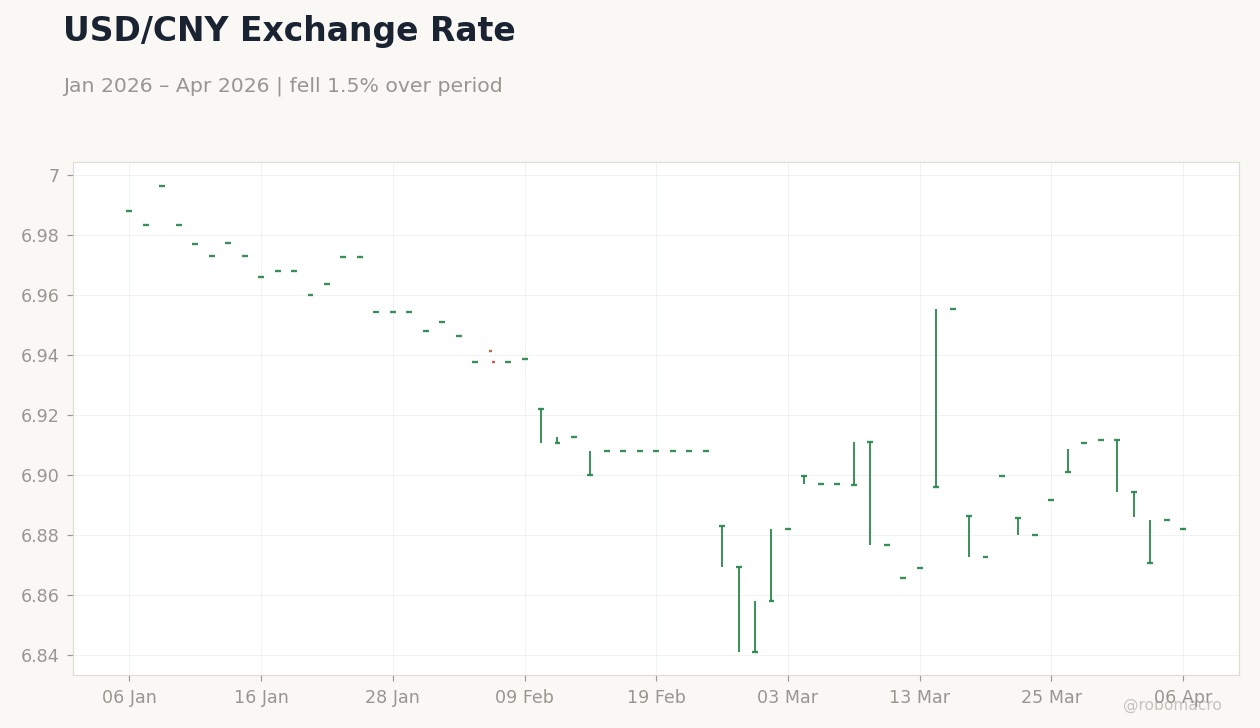

| USD/CNY | 6.88 | -0.05% |

| USD/HKD | 7.84 | -0.00% |

| Copper | 5.61 | +0.76% |

| Brent Crude | 109.63 | +0.55% |

| Gold | 4,676.10 | +0.53% |

| Bitcoin | 69,491.98 | +0.74% |

| China 2Y Govt Yield | - | - |

| China 10Y Govt Yield | - | - |

Prior Economic Events

| Data | Prior | Cons | Actual |

|---|---|---|---|

| No events available | |||

USD/CNY Exchange Rate | Type: market_hloc | Rate: 6.882 (2026-04-06) | Range: 6.841–6.997 | Trend(5pt): 6.988,6.955,6.908,6.869,6.882

USD/CNY Exchange Rate | Type: market_hloc | Rate: 6.882 (2026-04-06) | Range: 6.841–6.997 | Trend(5pt): 6.988,6.955,6.908,6.869,6.882

Today's Economic Events

| Data | Prior | Cons | Time |

|---|---|---|---|

| Inflation Rate Year-over-Year | 1.30 | 1.20 | 21:30 |

| Inflation Rate Month-over-Month | 1 | -0.30 | 21:30 |

| Producer Price Index Year-over-Year | -0.90 | 0.40 | 21:30 |

- Mainland indices gained on property support and lending optimism, offsetting HK and TW declines.

- Yuan gains traction in global payments via Hormuz tolls and digital yuan growth.

- Focus on upcoming China inflation data amid US trade tensions.

Yesterday's Recap

Mainland China equities advanced, with the Shanghai Composite climbing 1.36% to 3,944.83 and the CSI 300 rising 1.52% to 4,517.52, driven by optimism over property sector support and bank lending acceleration. Hong Kong's Hang Seng fell 0.70% to 25,116.53, pressured by property and tech drags amid regulatory concerns. Taiwan's TAIEX dropped 1.82% to 32,572.43, reflecting export slowdown fears tied to semiconductor supply chains.

The USD/CNY edged down 0.05% to 6.88, signaling PBoC firmness, while USD/HKD held steady at 7.84 with no change. Copper prices, a key China growth proxy, increased 0.76% to 5.61, supported by demand recovery signals. No major macro data releases occurred across Greater China, but cross-strait trade flows remained in focus amid US tariff escalations.

Brent crude rose 0.55% to 109.63, indirectly bolstering energy-linked investments in the region.

The Day Ahead

Investors await China's inflation data release on April 9, with YoY CPI consensus at 1.2% following a prior 1.3%, potentially influencing PBoC easing bets. MoM CPI is expected at -0.3% from 1.0%, signaling possible demand softening amid property woes. PPI YoY consensus stands at 0.4% versus -0.9% prior, which could reflect narrowing deflation in manufacturing.

No immediate events for Hong Kong or Taiwan, but semiconductor export outlooks may react to global AI demand cues. Broader attention turns to any State Council signals on fiscal support. Geopolitical developments, including US-China trade tensions, could drive intraday volatility in equities and FX.

Other Economic Notes

China's zero-tariff promise to Africa highlights deepening trade imbalances, potentially exacerbating mainland export dependencies amid US tariffs at 145%. Taiwan benefits from US-China trade war shifts, with reports indicating gains in supply chains alongside Mexico and the EU. Property sector dynamics in mainland China continue to stabilize, supported by accelerated bank lending, while Hong Kong faces volume-driven pressures in real estate.

Cross-strait investment flows remain resilient, buoyed by Taiwan's semiconductor strength despite export flatness. Bangladesh overtook China in US apparel exports for January-February 2026, reflecting tariff-driven diversions. (cont...)