Greater China Macro Daily(Beta Mode)

Yuan Hits 3-Year High on Iran Ceasefire

Market Snapshot

| Asset | Level | Change |

|---|---|---|

| Shanghai Composite | 3,966.17 | -0.72% |

| CSI 300 | 4,566.22 | -0.64% |

| Hang Seng | 25,893.02 | +3.09% |

| TAIEX | 34,761.38 | +4.61% |

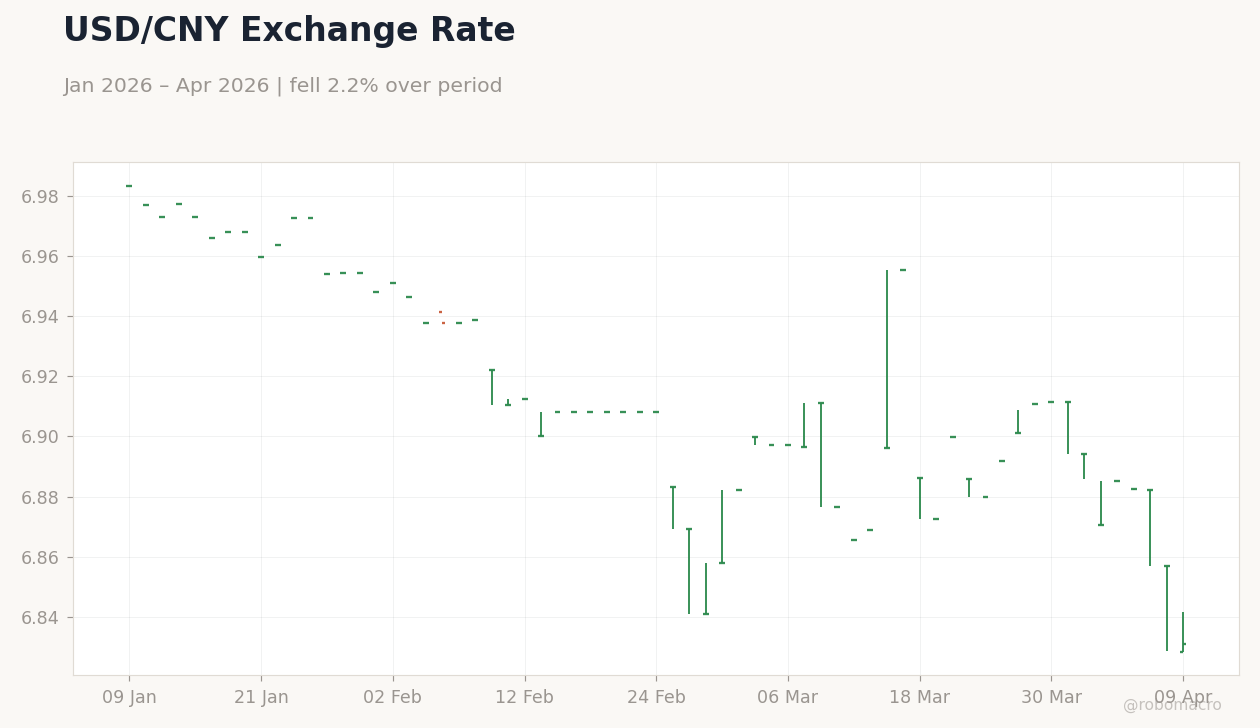

| USD/CNY | 6.83 | -0.38% |

| USD/HKD | 7.83 | +0.01% |

| Copper | 5.76 | -0.07% |

| Brent Crude | 96.44 | +1.78% |

| Gold | 4,790.50 | +0.86% |

| Bitcoin | 72,279.48 | +1.63% |

| China 2Y Govt Yield | - | - |

| China 10Y Govt Yield | - | - |

Prior Economic Events

| Data | Prior | Cons | Actual |

|---|---|---|---|

| No events available | |||

USD/CNY Exchange Rate | Type: market_hloc | USD/CNY: 6.831 (2026-04-09) | Range: 6.831–6.984 | Trend(5pt): 6.984,6.951,6.908,6.886,6.831

USD/CNY Exchange Rate | Type: market_hloc | USD/CNY: 6.831 (2026-04-09) | Range: 6.831–6.984 | Trend(5pt): 6.984,6.951,6.908,6.886,6.831

Today's Economic Events

| Data | Prior | Cons | Time |

|---|---|---|---|

| Inflation Rate Year-over-Year | 1.30 | 1.20 | 17:30 |

| Inflation Rate Month-over-Month | 1 | -0.20 | 17:30 |

| Producer Price Index Year-over-Year | -0.90 | 0.40 | 17:30 |

- Yuan surges to three-year high as Middle East ceasefire eases tensions, lifting Hong Kong and Taiwan equities amid bullish bets.

- Mainland China stocks slip on weak sentiment, while Beijing eyes aid for airlines and refiners hit by oil shocks.

- Taiwan reserves drop sharply on interventions, offsetting semiconductor strength; inflation data eyed for PBoC cues.

Yesterday's Recap

Greater China markets displayed mixed results on April 8, with mainland indices declining amid persistent property woes and deflation signals. The Shanghai Composite dropped 0.72% to 3,966.17, and the CSI 300 fell 0.64% to 4,566.22, as investors weighed stimulus hopes against weak producer prices. Conversely, Hong Kong's Hang Seng rose 3.09% to 25,893.02, buoyed by reduced geopolitical risks from the Iran ceasefire.

Taiwan's TAIEX advanced 4.61% to 34,761.38, supported by robust AI and semiconductor demand. The yuan appreciated notably, with USD/CNY declining 0.38% to 6.83, reaching a three-year high on eased tensions. USD/HKD inched up 0.01% to 7.83, staying within the peg.

Commodities were firm: copper dipped 0.07% to 5.76, Brent crude gained 1.78% to 96.44, gold rose 0.86% to 4,790.50, and Bitcoin climbed 1.63% to 72,279.48. No key data was released, but reports highlighted China's plans for airline aid and extra crude quotas for refiners to counter Iran-related oil disruptions. China 2Y and 10Y yields were unavailable.

The Day Ahead

Focus shifts to China's inflation releases at 17:30 ET on April 9. Year-over-year CPI is consensus at 1.2% (previous 1.3%), potentially showing mild cooling. Month-over-month CPI is expected at -0.2% (previous 1%), suggesting seasonal demand dips.

Producer Price Index year-over-year is forecasted at 0.4% (previous -0.9%), which could signal an end to deflation if met. These metrics may shape PBoC easing expectations, especially with yuan gains. No events for Hong Kong or Taiwan, though markets could respond to China's data surprises or ceasefire updates.

Broader sentiment may hinge on energy price moves and global risk appetite.

Other Economic Notes

Efforts to boost the yuan's global role intensify, with banks advocating wider use amid its appreciation and bullish analyst views. Energy challenges linger: China's LNG demand recovery stalls despite the ceasefire, as high oil costs strain sectors. Beijing's aid for airlines and quotas for teapot refiners aim to stabilize fuels amid Iran fallout.

(cont...)