Yesterday's Recap

China's March trade data disappointed as exports rose only 2.5% YoY against expectations of 8.3%, reflecting fallout from the US-Israeli war in Iran that disrupted global supply chains and elevated energy prices, leading to a sharply narrower trade surplus of CNY 51.13 billion compared to the CNY 112 billion consensus. Imports, however, jumped 27.8% YoY, surpassing the 11.1% forecast, fueled by increased commodity purchases including oil amid fears of Middle East supply halts, with Saudi crude sales to China expected to halve next month per industry reports. New yuan loans came in at CNY 2.99 trillion, missing the CNY 3.4 trillion estimate, indicating banks' restraint in extending credit amid property sector woes and deflationary pressures, where verified China CPI YoY stood at -0.10% as of early 2025.

Mainland markets showed resilience with the Shanghai Composite climbing 0.20% to 3,996.67 and CSI 300 advancing 0.36% to 4,662.83, supported by hopes for PBoC stimulus and a rebound in copper prices up 1.77% to 6.08 as a China growth proxy. Hong Kong's Hang Seng dropped 0.90% to 25,660.85, pressured by tech sector weakness and USD/HKD edging up 0.04% to 7.83 near the peg's upper band. Taiwan's TAIEX rose 0.11% to 35,457.29, buoyed by semiconductor export optimism despite geopolitical tensions, with cross-strait trade flows remaining stable.

The Day Ahead

China's key Q1 data releases on April 15 will dominate attention, including GDP growth YoY expected at 4.8% versus prior 4.5%, alongside quarter-over-quarter at 1.4% from 1.2%, providing insights into the economy's resilience amid the Iran war's global shocks. Industrial production YoY is forecasted at 5.6% down from 6.3%, while retail sales YoY may slip to 2.3% from 2.8%, highlighting consumer demand trends in mainland China. Fixed asset investment YTD YoY is anticipated at 1.9% up slightly from 1.8%, with house price index YoY lacking consensus but following prior -3.2%, potentially signaling ongoing property stabilization efforts.

Later on April 19, the PBoC's loan prime rates for 1Y and 5Y are due, with previous levels at 3% and 3.5% respectively, where markets watch for any cuts to support growth. No major Hong Kong or Taiwan data is scheduled immediately.

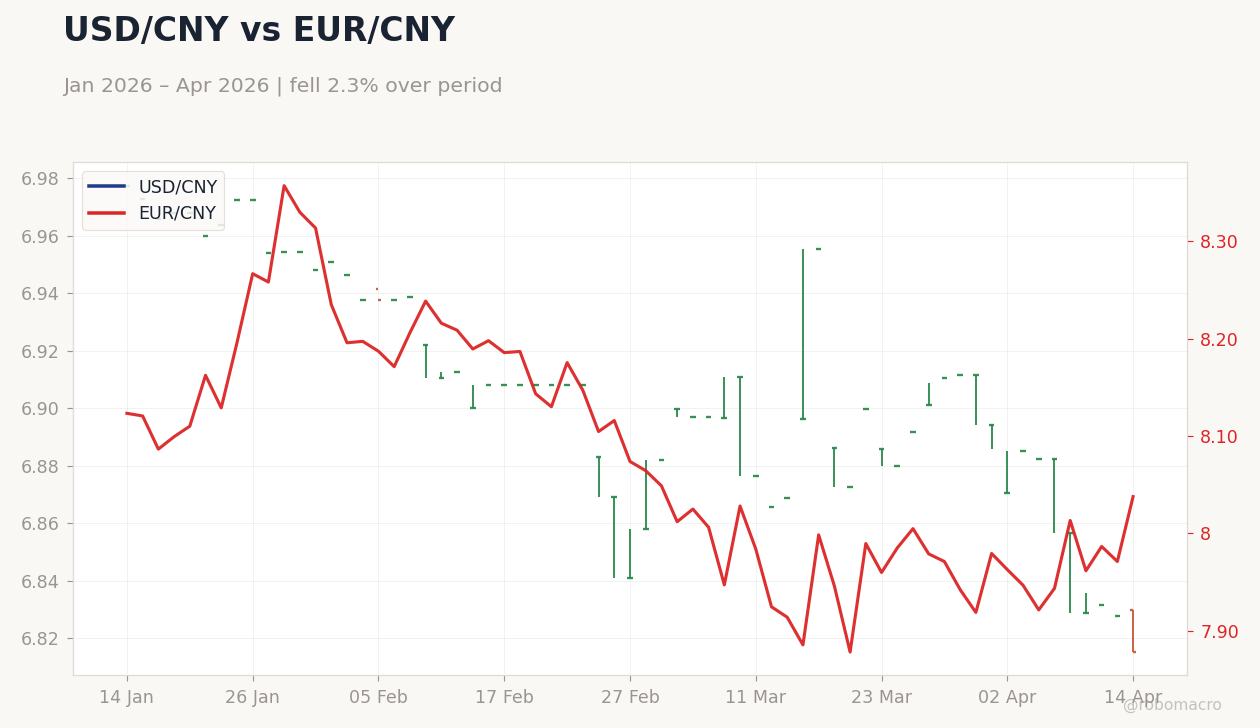

USD/CNY vs EUR/CNY | Type: market_hloc | USD/CNY: 6.815 (2026-04-14) | Range: 6.815–6.977 | Trend(5pt): 6.977,6.938,6.841,6.886,6.815 | EUR/CNY: 8.038 (2026-04-14) | Range: 7.878–8.357 | Trend(5pt): 8.123,8.187,8.074,7.96,8.038

USD/CNY vs EUR/CNY | Type: market_hloc | USD/CNY: 6.815 (2026-04-14) | Range: 6.815–6.977 | Trend(5pt): 6.977,6.938,6.841,6.886,6.815 | EUR/CNY: 8.038 (2026-04-14) | Range: 7.878–8.357 | Trend(5pt): 8.123,8.187,8.074,7.96,8.038