Greater China Macro Daily(Beta Mode)

PBoC Signals Steepening Amid Mixed Stocks

Market Snapshot

| Asset | Level | Change |

|---|---|---|

| Shanghai Composite | 4,079.90 | -0.33% |

| CSI 300 | 4,769.37 | -0.35% |

| Hang Seng | 25,978.07 | +0.24% |

| TAIEX | 38,932.40 | +3.23% |

| USD/CNY | 6.84 | +0.14% |

| USD/HKD | 7.84 | +0.03% |

| Copper | 6.03 | -0.80% |

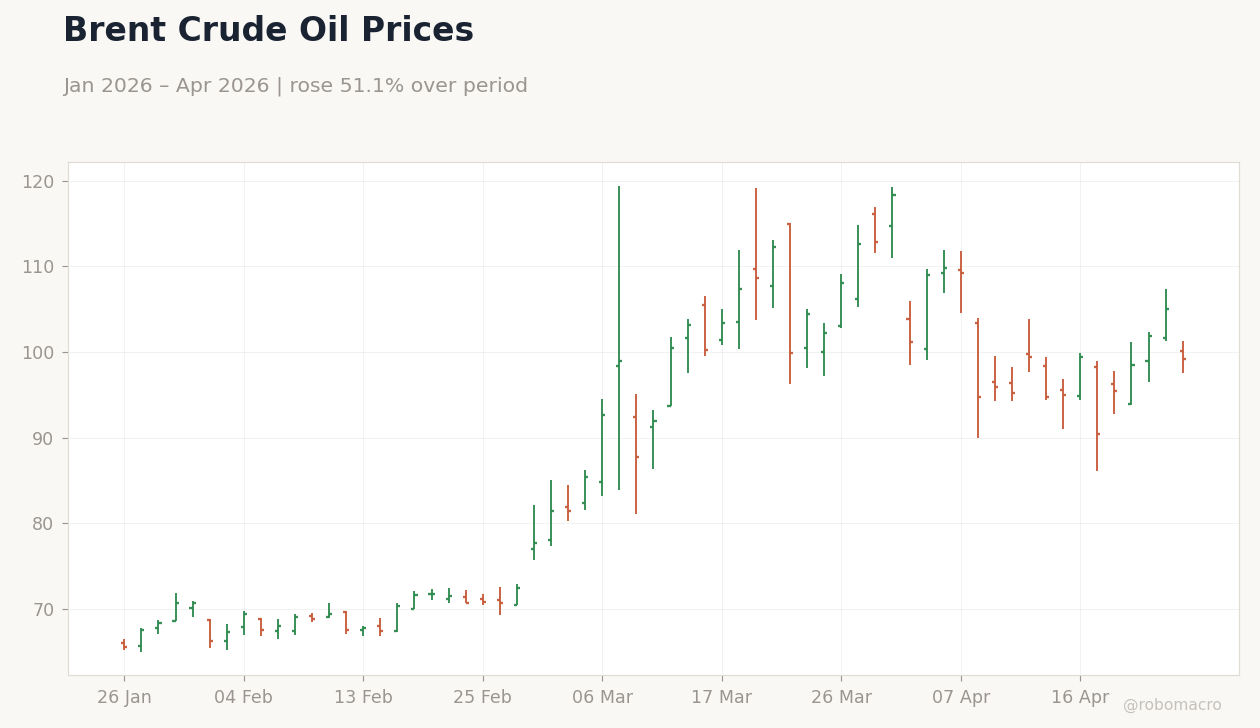

| Brent Crude | 99.13 | -5.65% |

| Gold | 4,740.90 | +0.76% |

| Bitcoin | 78,436.56 | +1.06% |

| China 2Y Govt Yield | - | - |

| China 10Y Govt Yield | - | - |

Prior Economic Events

| Data | Prior | Cons | Actual |

|---|---|---|---|

| No events available | |||

Shanghai Composite Index | Type: market_hloc | Shanghai Composite: 4080 (2026-04-24) | Range: 3813–4183 | Trend(6pt): 4133,4082,4095,3919,4093,4080

Shanghai Composite Index | Type: market_hloc | Shanghai Composite: 4080 (2026-04-24) | Range: 3813–4183 | Trend(6pt): 4133,4082,4095,3919,4093,4080

Today's Economic Events

| Data | Prior | Cons | Time |

|---|---|---|---|

| NBS Manufacturing PMI | 50.40 | 50.20 | 21:30 |

| NBS Non-Manufacturing PMI | 50.10 | 49.90 | 21:30 |

| RatingDog Manufacturing PMI | 50.80 | 50.50 | 21:45 |

- Mainland equities dipped on property woes, while Taiwan surged on semi strength.

- PBoC signals steepening bias as industrial activity stabilizes.

- Global tensions boost China's RMB push and oil stockpiles.

Yesterday's Recap

Greater China equities showed mixed performance on April 25, with mainland China's Shanghai Composite closing at 4,079.90 after a 0.33% decline, driven by ongoing property sector pressures and profit-taking. The CSI 300 fell 0.35% to 4,769.37, reflecting weakness in financials amid fiscal stimulus pullbacks reported in recent analyses. Hong Kong's Hang Seng edged up 0.24% to 25,978.07, supported by tech sympathy trades despite broader caution.

Taiwan's TAIEX jumped 3.23% to 38,932.40, fueled by semiconductor export optimism following regulatory easing for local investors in TSMC shares. Currency markets remained stable, with USD/CNY rising 0.14% to 6.84 on PBoC's reference rate adjustment signaling cautious policy shifts. Commodities relevant to China softened, including copper down 0.80% to 6.03 and Brent crude dropping 5.65% to 99.13, amid war disruptions in the Middle East.

No major data releases occurred, but DBS analysis highlighted steady industrial activity in mainland China supporting PBoC's easing inclinations.

The Day Ahead

Attention turns to mainland China's key PMI releases on April 29, with NBS Manufacturing PMI expected at 50.2 versus prior 50.4, potentially signaling sustained factory momentum amid global supply chain strains. The NBS Non-Manufacturing PMI is forecast at 49.9 from 50.1, which could underscore service sector vulnerabilities tied to property drags. Caixin Manufacturing PMI, due shortly after at 21:45 ET, is anticipated at 50.5 against previous 50.8, offering private-sector insights into export-oriented industries.

No events are slated for Hong Kong or Taiwan, but cross-strait trade flows may react to any PMI surprises. Geopolitical developments, including Australia's energy talks with China, could influence commodity proxies like copper. Overall, these indicators will shape expectations for PBoC liquidity moves.

Other Economic Notes

Mainland China's fiscal stimulus slowdown in March, as the economy rebounded despite Iran war disruptions, points to a shift toward targeted support rather than broad spending. Property sector fragility persists, with recent data previews exacerbating equity pressures, though high-tech manufacturing resilience offers a counterbalance. Broader themes include China's push for RMB internationalization, accelerated by global sanctions and petroyuan discussions, aiming to reduce dollar dependence.

(cont...)