Greater China Macro Daily(Beta Mode)

China Exports Surge, Stocks Dip

Market Snapshot

| Asset | Level | Change |

|---|---|---|

| Shanghai Composite | 4,179.95 | -0.00% |

| CSI 300 | 4,871.91 | -0.58% |

| Hang Seng | 26,393.71 | -0.87% |

| TAIEX | 41,603.94 | -0.79% |

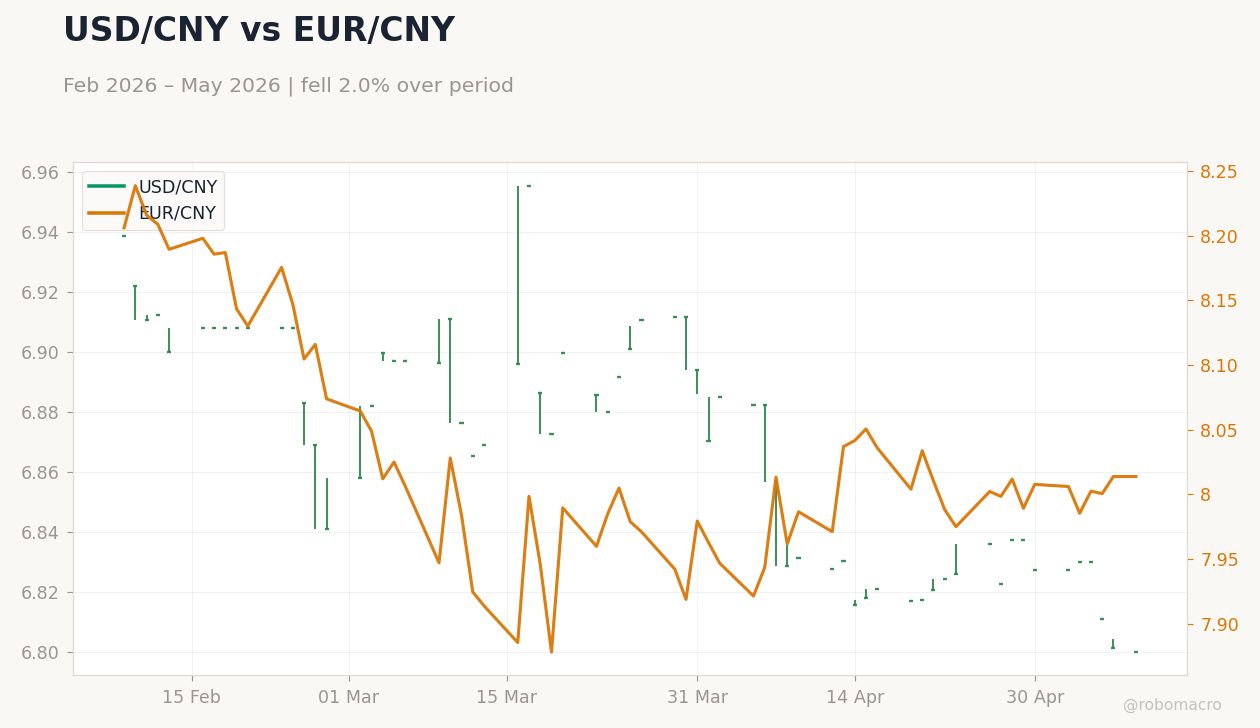

| USD/CNY | 6.80 | -0.02% |

| USD/HKD | 7.83 | -0.07% |

| Copper | 6.30 | +2.76% |

| Brent Crude | 101.29 | +1.23% |

| Gold | 4,730.70 | +0.66% |

| Bitcoin | 80,908.91 | +0.30% |

| China 2Y Govt Yield | - | - |

| China 10Y Govt Yield | - | - |

Prior Economic Events

| Data | Prior | Cons | Actual |

|---|---|---|---|

| Trade Balance | 51,130m | 83,300m | 84,820m |

| Exports Year-over-Year | 2.50 | 7.90 | 14.10 |

| Imports Year-over-Year | 27.80 | 15.20 | 25.30 |

Copper Prices | Type: market_hloc | Price: 6.297 (2026-05-08) | Range: 5.343–6.297 | Trend(6pt): 5.896,5.855,5.529,6.067,6.128,6.297

Copper Prices | Type: market_hloc | Price: 6.297 (2026-05-08) | Range: 5.343–6.297 | Trend(6pt): 5.896,5.855,5.529,6.067,6.128,6.297

Today's Economic Events

| Data | Prior | Cons | Time |

|---|---|---|---|

| Inflation Rate Year-over-Year | 1 | 0.80 | 21:30 |

| Inflation Rate Month-over-Month | -0.70 | -0.10 | 21:30 |

| Producer Price Index Year-over-Year | 0.50 | 1.50 | 21:30 |

| Current Account Prel | 243,800m | - | 05:00 |

- China's April exports jumped 14.1% YoY, topping 7.9% consensus, with imports up 25.3% YoY vs 15.2% expected, yielding a $84.82 billion surplus against $83.3 billion forecast.

- Mainland stocks mixed, Shanghai Composite flat at 4,179.95 (0.00%), CSI 300 down 0.58% to 4,871.91; Hang Seng fell 0.87% to 26,393.71, TAIEX dropped 0.79% to 41,603.94.

- Commodities rose amid trade strength: copper +2.76% to 6.30, Brent +1.23% to 101.29, gold +0.66% to 4,730.70; USD/CNY eased 0.02% to 6.80, USD/HKD down 0.07% to 7.83.

Yesterday's Recap

China's April trade figures outperformed forecasts, with exports accelerating to 14.1% YoY growth, exceeding the 7.9% consensus and highlighting strong external demand despite US tariff threats. Imports rose 25.3% YoY, beating the 15.2% estimate, fueled by commodity stockpiling but constrained by Strait of Hormuz disruptions impacting energy flows. The trade surplus expanded to $84.82 billion, above the $83.3 billion consensus, underscoring trade's role in stabilizing the economy amid domestic challenges.

Mainland markets ended mixed, with the Shanghai Composite unchanged at 4,179.95 (0.00% change), while the CSI 300 declined 0.58% to 4,871.91 on financial sector weakness. Hong Kong's Hang Seng Index dropped 0.87% to 26,393.71, weighed by tech and real estate amid debt worries. Taiwan's TAIEX fell 0.79% to 41,603.94, despite semiconductor resilience, as opposition efforts to trim defense spending introduced uncertainty.

Currencies remained steady, with USD/CNY slipping 0.02% to 6.80 and USD/HKD easing 0.07% to 7.83 within the peg range. Commodities gained: copper rose 2.76% to 6.30 on China demand signals, Brent climbed 1.23% to 101.29, and gold advanced 0.66% to 4,730.70.

The Day Ahead

China's April inflation metrics are due at 21:30 ET, with YoY CPI forecasted at 0.8% versus previous 1%, indicating potential softening in price pressures from subdued demand. MoM CPI is expected at -0.1% after -0.7% prior, while PPI YoY is projected at 1.5% from 0.5%, capturing rising input costs. These data could shape PBoC policy, particularly if deflation signals emerge.

Preliminary Q1 current account figures arrive May 15, providing capital flow insights without available consensus. No major releases for Hong Kong or Taiwan today, though markets may track Taiwan defense budget developments amid cross-strait dynamics. Expect monitoring of State Council updates on local debt mitigation following recent commitments to balance risk and growth.

Other Economic Notes

China's energy imports dropped sharply in April due to Hormuz Strait blockages, heightening supply risks and potentially hindering industrial rebound. <i>↓ p.2</i>