Greater China Macro Daily(Beta Mode)

Equities Mixed on Stimulus Bets

Market Snapshot

| Asset | Level | Change |

|---|---|---|

| Shanghai Composite | 4,229.29 | +0.35% |

| CSI 300 | 4,973.54 | +0.52% |

| Hang Seng | 26,347.91 | -0.22% |

| TAIEX | 41,898.32 | +0.26% |

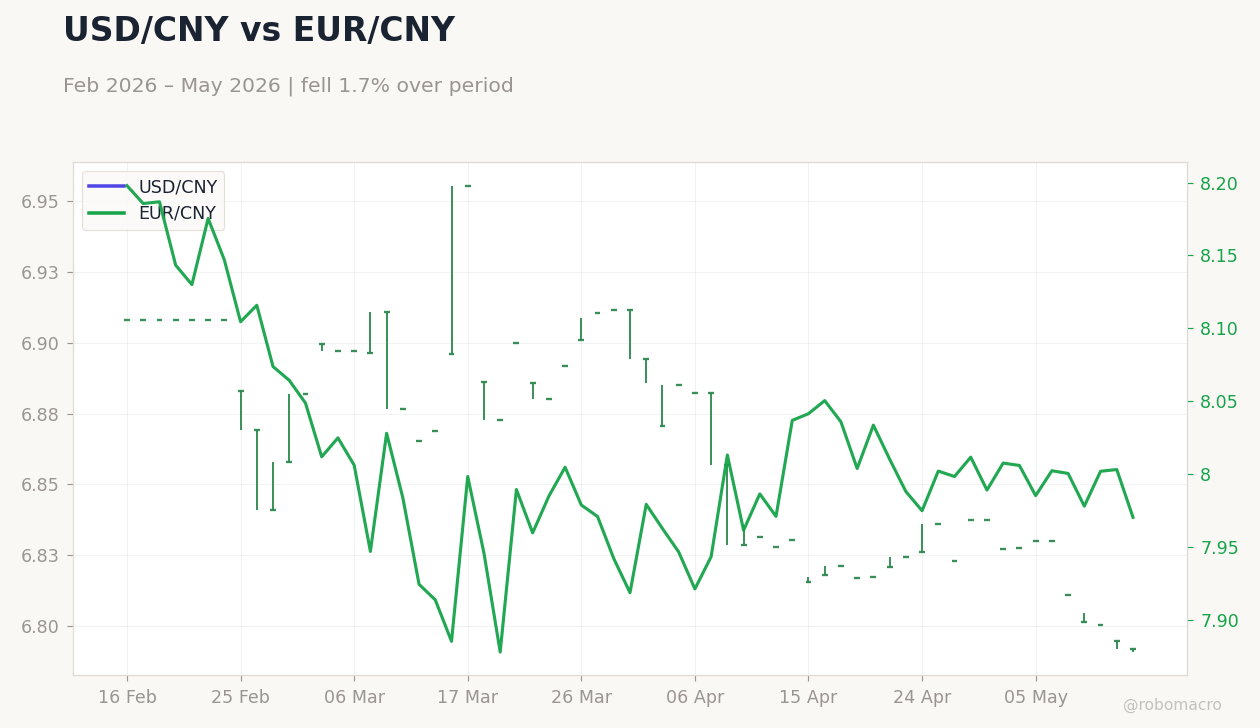

| USD/CNY | 6.79 | -0.04% |

| USD/HKD | 7.83 | +0.01% |

| Copper | 6.63 | +2.18% |

| Brent Crude | 105.46 | -2.14% |

| Gold | 4,704.50 | +0.58% |

| Bitcoin | 79,401.74 | -1.34% |

| China 2Y Govt Yield | - | - |

| China 10Y Govt Yield | - | - |

Prior Economic Events

| Data | Prior | Cons | Actual |

|---|---|---|---|

| No events available | |||

Shanghai Composite Index | Type: market_hloc | Price: 4214 (2026-05-12) | Range: 3813–4225 | Trend(5pt): 4082,4129,3892,4082,4214

Shanghai Composite Index | Type: market_hloc | Price: 4214 (2026-05-12) | Range: 3813–4225 | Trend(5pt): 4082,4129,3892,4082,4214

Today's Economic Events

| Data | Prior | Cons | Time |

|---|---|---|---|

| Current Account Prel | 243,800m | - | 05:00 |

| House Price Index Year-over-Year | -3.40 | - | 21:30 |

| Industrial Production Year-over-Year | 5.70 | - | 22:00 |

| Retail Sales Year-over-Year | 1.70 | - | 22:00 |

| Fixed Asset Investment (YTD) Year-over-Year | 1.70 | - | 22:00 |

| Loan Prime Rate 1Y | 3 | - | 21:15 |

| Loan Prime Rate 5Y | 3.50 | - | 21:15 |

- Greater China equities were mixed, with mainland indices up modestly on property support hopes, while Hong Kong dipped and Taiwan edged higher.

- Key upcoming China data includes industrial production, retail sales, and loan prime rates, amid calls for further easing.

- Geopolitical focus on Trump-Xi summit, Iran tensions driving oil prices, and China's imported inflation risks.

Yesterday's Recap

Mainland China's Shanghai Composite rose 0.35% to 4,229.29, buoyed by financials and materials on speculation of new property funding, while the CSI 300 gained 0.52% to 4,973.54, supported by copper price jumps signaling demand recovery. Hong Kong's Hang Seng fell 0.22% to 26,347.91, weighed by tech weakness and U.S.-China trade worries, plus local property headwinds. Taiwan's TAIEX rose 0.26% to 41,898.32, lifted by semiconductors despite broader Asian caution.

Currencies were steady, with USD/CNY down 0.04% to 6.79 on mild yuan gains, and USD/HKD up 0.01% to 7.83 in the peg range. Commodities showed China-linked strength, with copper up 2.18% to 6.63 on growth optimism, while Brent crude dropped 2.14% to 105.46 amid supply fears. Gold rose 0.58% to 4,704.50, and Bitcoin fell 1.34% to 79,401.74.

No major Greater China data releases yesterday, with markets reacting to news of Tesla's China financing push and G7 calls for China to curb surpluses. Volumes were moderate, up slightly in mainland on stimulus talk.

The Day Ahead

China's preliminary current account data is due May 15, with prior at 243.8 billion USD, offering trade surplus insights amid tensions. On May 17, high-impact industrial production (prev. 5.7%) and retail sales (prev.

1.7%) year-over-year will gauge demand, alongside fixed asset investment (prev. 1.7%) and house price index (prev. -3.4%).

Loan prime rates for 1Y (prev. 3%) and 5Y (prev. 3.5%) follow on May 19, likely holding steady absent new stimulus.

No key events for Hong Kong or Taiwan, though markets may respond to Trump-Xi talks on tariffs, Taiwan arms, and Hong Kong issues. These could shape PBoC easing views, with focus on potential RRR cuts.

Other Economic Notes

China's property market hints at stabilization via eased city restrictions, lifting transactions, but upcoming house price data will check deflation trends. Deflation persists, with April 2025 CPI at -0.10% year-over-year, pressing for fiscal boosts to consumption. Taiwan's growth rides semiconductor exports, tied to global tech, while Hong Kong faces retail hurdles from fuel surcharge cuts and airport shifts like 11 Skies handover.

<i>↓ p.2</i>