Greater China Macro Daily(Beta Mode)

Mainland Dips, Bonds Rally on Cash

Market Snapshot

| Asset | Level | Change |

|---|---|---|

| Shanghai Composite | 4,209.22 | -0.79% |

| CSI 300 | 4,955.58 | -0.86% |

| Hang Seng | 26,388.44 | +0.15% |

| TAIEX | 41,374.50 | -1.25% |

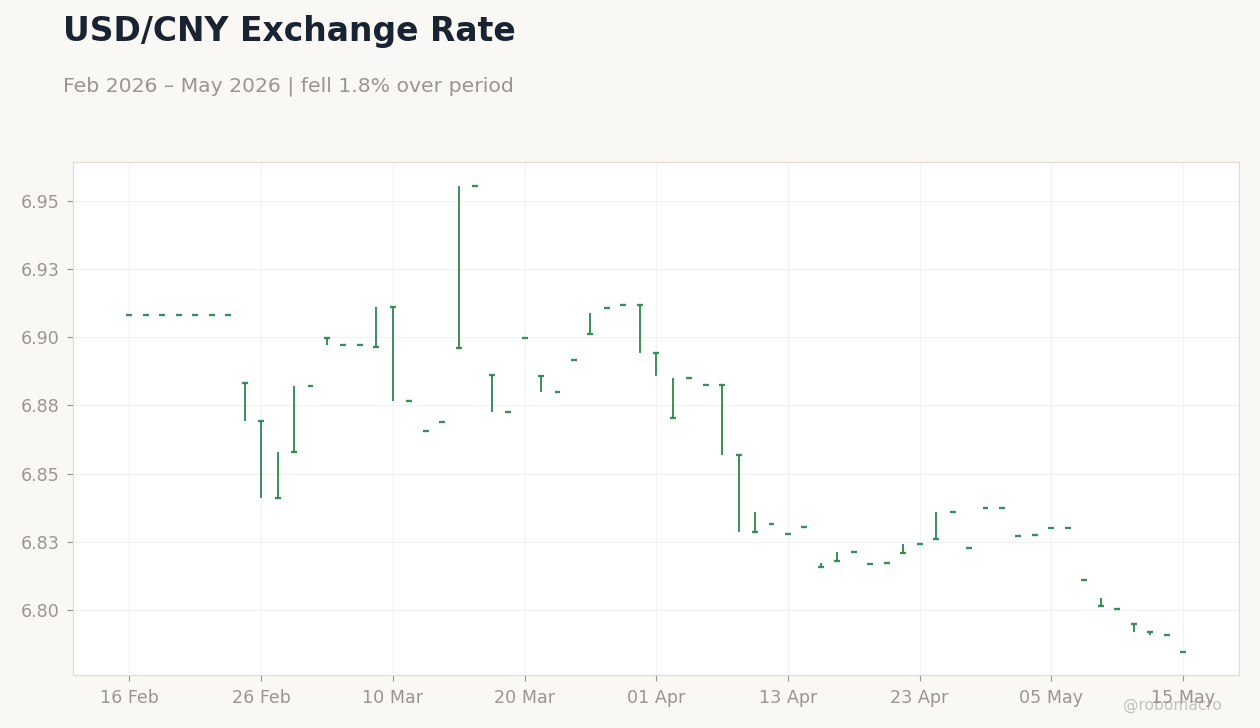

| USD/CNY | 6.79 | -0.02% |

| USD/HKD | 7.83 | +0.04% |

| Copper | 6.58 | -0.84% |

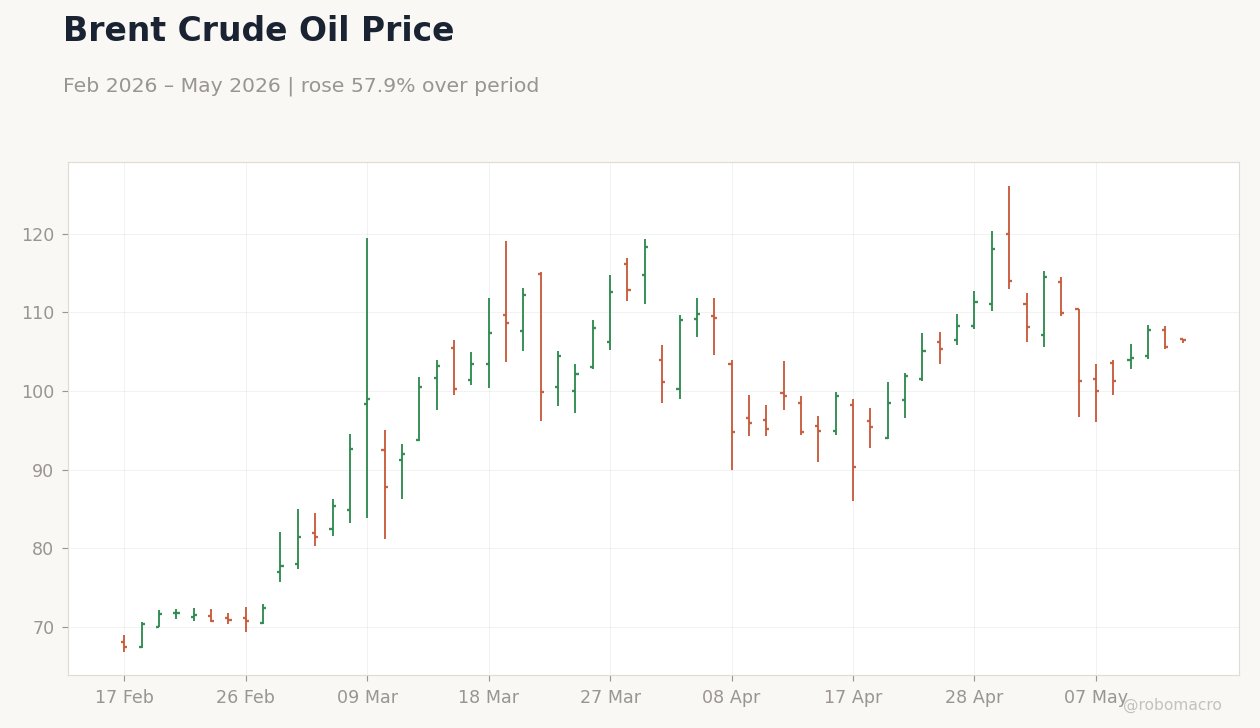

| Brent Crude | 106.20 | +0.54% |

| Gold | 4,664.90 | -0.70% |

| Bitcoin | 81,373.76 | +2.64% |

| China 2Y Govt Yield | - | - |

| China 10Y Govt Yield | - | - |

Prior Economic Events

| Data | Prior | Cons | Actual |

|---|---|---|---|

| No events available | |||

Shanghai Composite Index | Type: market_hloc | Price: 4243 (2026-05-13) | Range: 3813–4243 | Trend(5pt): 4117,4095,3949,4085,4243

Shanghai Composite Index | Type: market_hloc | Price: 4243 (2026-05-13) | Range: 3813–4243 | Trend(5pt): 4117,4095,3949,4085,4243

Today's Economic Events

| Data | Prior | Cons | Time |

|---|---|---|---|

| Current Account Prel | 243,800m | - | 05:00 |

| House Price Index Year-over-Year | -3.40 | - | 21:30 |

| Industrial Production Year-over-Year | 5.70 | - | 22:00 |

| Retail Sales Year-over-Year | 1.70 | - | 22:00 |

| Fixed Asset Investment (YTD) Year-over-Year | 1.70 | - | 22:00 |

| Loan Prime Rate 1Y | 3 | - | 21:15 |

| Loan Prime Rate 5Y | 3.50 | - | 21:15 |

- Shanghai Comp -0.8%, CSI 300 -0.9% as mainland equities slipped; Hang Seng +0.2%, TAIEX -1.3%.

- PBoC warns of imported inflation from Middle East-driven oil surge to $106/bbl.

- Xi-Trump summit signals US-China stability, revives tech rally hopes.

Yesterday's Recap

Mainland China equities declined amid global caution, with Shanghai Composite falling 0.79% to 4,209.22 and CSI 300 dropping 0.86% to 4,955.58. Hong Kong's Hang Seng bucked the trend, rising 0.15% to 26,388.44 amid local stability signals. Taiwan's TAIEX fell 1.25% to 41,374.50 on tech sector watch.

USD/CNY edged lower 0.02% to 6.79, supporting yuan stability, while USD/HKD rose 0.04% to 7.83 with peg intact. Copper retreated 0.84% to 6.58, signaling softer China demand proxies, as Brent climbed 0.54% to 106.20 on Middle East risks. Gold dipped 0.70% to 4,664.90; Bitcoin surged 2.64% to 81,374.

No major data releases occurred across Greater China yesterday.

The Day Ahead

China's Q1 Current Account preliminary data releases tomorrow at 05:00 ET (medium impact, prior 244bn USD surplus). Key April prints follow on May 17: Industrial Production YoY (high, prior 5.7%), Retail Sales YoY (high, prior 1.7%), Fixed Asset Investment YTD YoY (medium, prior 1.7%), House Price Index YoY (medium, prior -3.4%). PBoC Loan Prime Rates (1Y prior 3%, 5Y 3.5%) due May 19 could signal easing if CPI remains soft.

Watch HKMA aggregate balance for USD/HKD peg strains amid dollar volatility. No major Taiwan or Hong Kong data scheduled.

Other Economic Notes

China’s benchmark bonds are heading for their best month since October, as abundant liquidity offsets debt supply concerns. Hong Kong public rental housing wait times fell to 4.7 years as of March, easing social pressures. Xi-Trump summit underscores US-China stability amid global tensions.

Global Macro News

Bank of Canada rate announcement at 09:45 ET today, with Business Outlook Survey and Consumer Expectations at 11:30 ET. Dollar index fell 0.03% after erasing early gains on stronger-than-expected US April existing home sales. Xi-Trump summit emphasizes bilateral stability with caution, reviving China tech rally hopes via reported US clearance of Nvidia H200 sales.

Middle East conflict drives Brent to 106.20, prompting PBoC imported inflation warning on oil and commodities. Trump’s war in Iran boosts petroyuan prospects as dollar rival. <i>↓ p.2</i>