Greater China Macro Daily(Beta Mode)

China Data Looms as Equities Slide

Market Snapshot

| Asset | Level | Change |

|---|---|---|

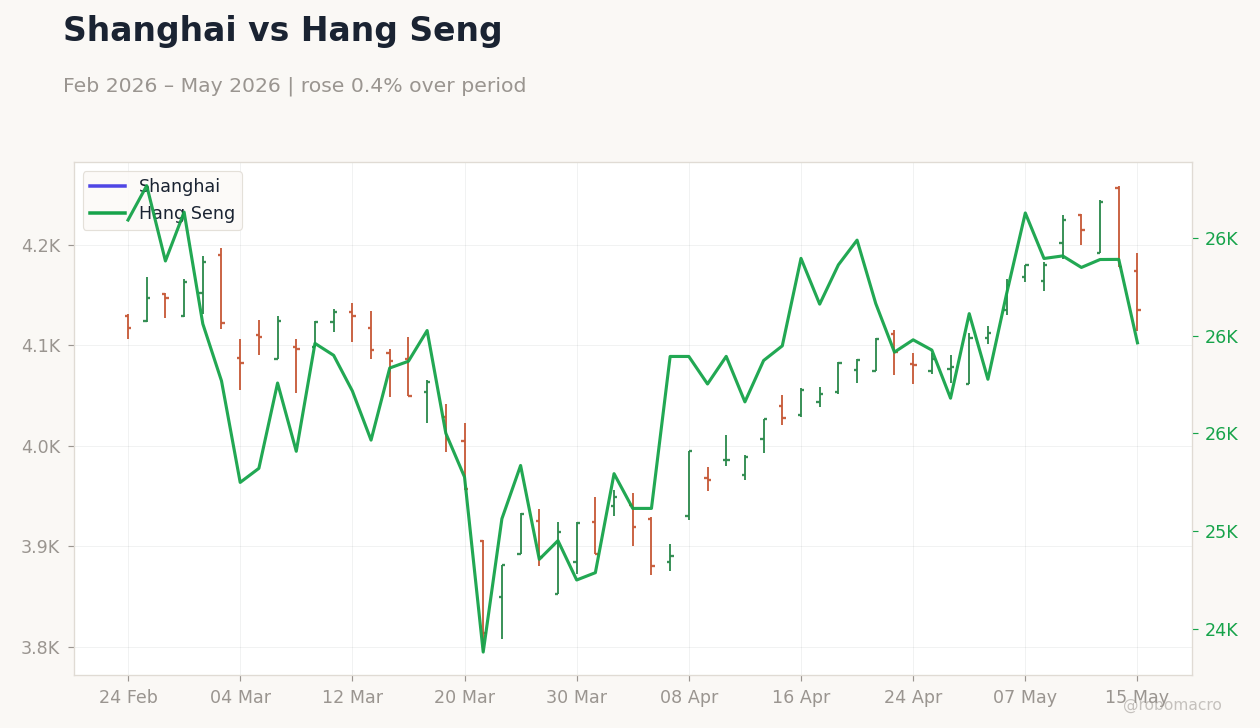

| Shanghai Composite | 4,135.39 | -1.02% |

| CSI 300 | 4,859.59 | -1.12% |

| Hang Seng | 25,962.73 | -1.62% |

| TAIEX | 41,172.36 | -1.39% |

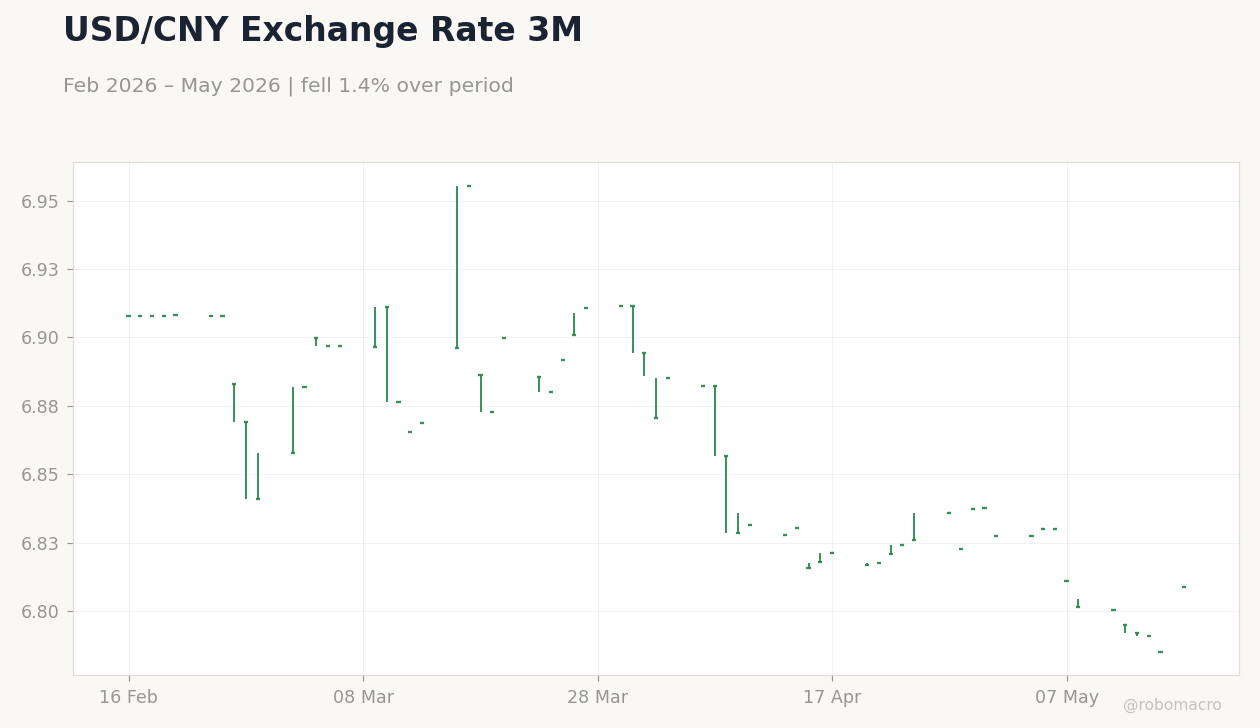

| USD/CNY | 6.81 | +0.35% |

| USD/HKD | 7.83 | -0.02% |

| Copper | 6.30 | -4.15% |

| Brent Crude | 109.26 | +3.35% |

| Gold | 4,561.90 | -2.48% |

| Bitcoin | 78,298.99 | +0.21% |

| China 2Y Govt Yield | - | - |

| China 10Y Govt Yield | - | - |

Prior Economic Events

| Data | Prior | Cons | Actual |

|---|---|---|---|

| No events available | |||

Hang Seng Index 3M | Type: market_hloc | Index Level: 2.596e+04 (2026-05-15) | Range: 2.438e+04–2.708e+04 | Trend(6pt): 2.671e+04,2.59e+04,2.479e+04,2.592e+04,2.639e+04,2.596e+04

Hang Seng Index 3M | Type: market_hloc | Index Level: 2.596e+04 (2026-05-15) | Range: 2.438e+04–2.708e+04 | Trend(6pt): 2.671e+04,2.59e+04,2.479e+04,2.592e+04,2.639e+04,2.596e+04

Today's Economic Events

| Data | Prior | Cons | Time |

|---|---|---|---|

| House Price Index Year-over-Year | -3.40 | - | 21:30 |

| Industrial Production Year-over-Year | 5.70 | 5.90 | 22:00 |

| Retail Sales Year-over-Year | 1.70 | 2 | 22:00 |

| Fixed Asset Investment (YTD) Year-over-Year | 1.70 | 1.60 | 22:00 |

| Loan Prime Rate 1Y | 3 | 3 | 21:15 |

| Loan Prime Rate 5Y | 3.50 | 3.50 | 21:15 |

- China industrial production and retail sales releases tonight expected to show modest gains, with IP consensus at 5.9% y/y.

- Regional equities fall sharply, Hang Seng down 1.62% and CSI 300 off 1.12%, as copper drops 4.15%.

- PBoC set to hold 1Y and 5Y LPR steady at 3% and 3.5% on May 19 after recent liquidity additions.

Yesterday's Recap

Greater China markets declined across the board on May 16 with no major data releases. Shanghai Composite fell 1.02% to 4,135.39 while CSI 300 dropped 1.12% to 4,859.59 amid thin trading. Hang Seng slid 1.62% to 25,962.73 and TAIEX eased 1.39% to 41,172.36.

USD/CNY rose 0.35% to 6.81, reflecting mild yuan softening, while USD/HKD held near the peg at 7.83. Copper tumbled 4.15% to 6.30, flagging softer mainland demand, and Brent crude advanced 3.35% to 109.26 on global supply concerns. Gold declined 2.48% to 4,561.90 as investors rotated out of safe havens.

The Day Ahead

China House Price Index y/y prints at 21:30 ET followed by high-impact industrial production, retail sales and fixed-asset investment figures at 22:00 ET. Markets will parse whether IP accelerates to the 5.9% consensus and whether retail sales lift above 1.7% prior. PBoC conducts 7-day reverse-repo operations with potential net liquidity injection.

Attention then shifts to the May 19 Loan Prime Rate decision where both 1Y and 5Y rates are expected to remain unchanged at 3% and 3.5%. Taiwan semiconductor export trends and HKMA aggregate balance updates will also feature.

Other Economic Notes

Beijing continues to favor upgrading older manufacturing sectors rather than phasing them out, underscoring the sector’s role as economic backbone. Property transaction volumes rose in second-tier cities after expanded mortgage easing, yet fixed-asset investment remains soft. US-China agricultural purchase commitments of at least $17 billion annually through 2028 provide modest trade stability.

Cross-strait semiconductor supply-chain talks resumed, focusing on talent flows without new tariff escalations.

Global Macro News

Fallout from the Iran conflict continues to lift Brent prices and complicate inflation outlooks worldwide. US-China trade relations stabilized after the Trump-Xi summit, with preliminary agreements to reduce agricultural barriers now moving toward finalization. America’s AI race with China faces shifting dynamics around export controls and technology access.

<i>↓ p.2</i>