Greater China Macro Daily(Beta Mode)

China Slowdown Revives Stimulus Hopes

Market Snapshot

| Asset | Level | Change |

|---|---|---|

| Shanghai Composite | 4,135.39 | -1.02% |

| CSI 300 | 4,859.59 | -1.12% |

| Hang Seng | 25,962.73 | -1.62% |

| TAIEX | 41,172.36 | -1.39% |

| USD/CNY | 6.80 | +0.21% |

| USD/HKD | 7.83 | -0.03% |

| Copper | 6.34 | +1.35% |

| Brent Crude | 109.28 | +0.02% |

| Gold | 4,570.80 | +0.33% |

| Bitcoin | 77,023.02 | -0.52% |

| China 2Y Govt Yield | - | - |

| China 10Y Govt Yield | - | - |

Prior Economic Events

| Data | Prior | Cons | Actual |

|---|---|---|---|

| No events available | |||

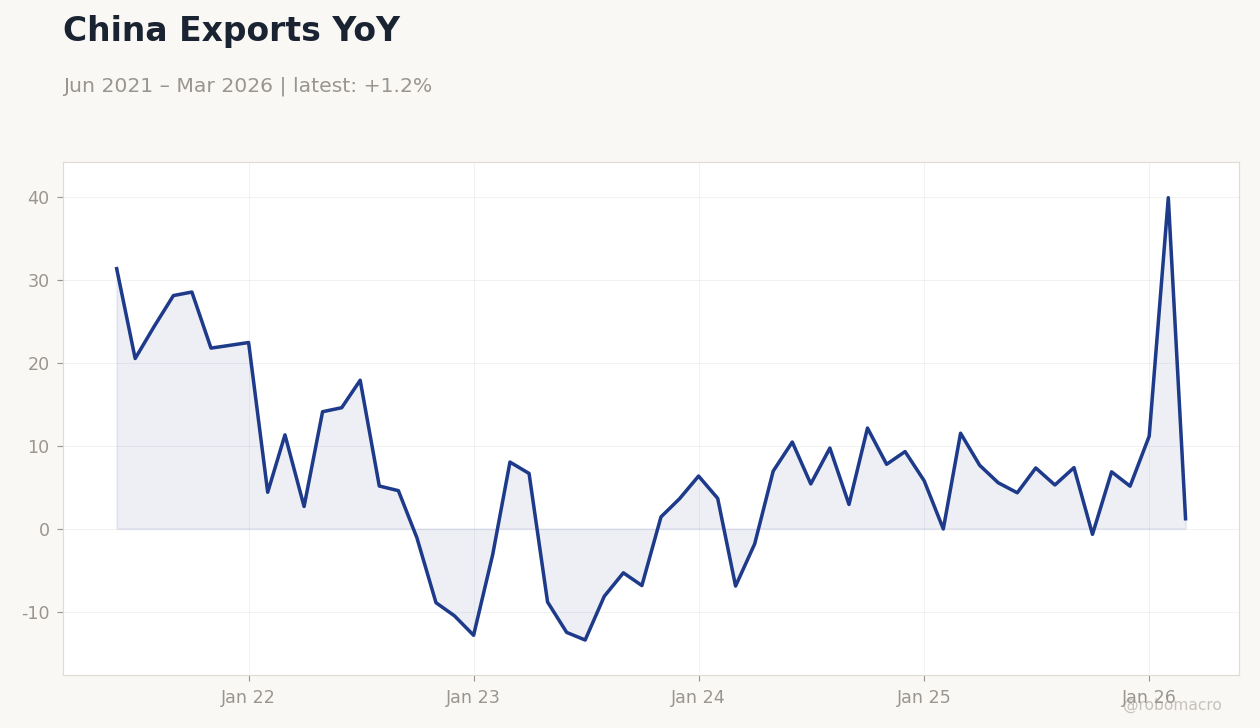

China Exports YoY | Type: macro_line | YoY %: 1.195 (2026-03-01) | Range: -13.41–39.86 | Trend(6pt): 31.32,5.14,-6.853,9.287,39.86,1.195

China Exports YoY | Type: macro_line | YoY %: 1.195 (2026-03-01) | Range: -13.41–39.86 | Trend(6pt): 31.32,5.14,-6.853,9.287,39.86,1.195

Today's Economic Events

| Data | Prior | Cons | Time |

|---|---|---|---|

| Loan Prime Rate 1Y | 3 | 3 | 17:15 |

| Loan Prime Rate 5Y | 3.50 | 3.50 | 17:15 |

| Tuesday (2026-05-19) | |||

| Loan Prime Rate 1Y | 3 | 3 | 17:15 |

| Loan Prime Rate 5Y | 3.50 | 3.50 | 17:15 |

- China April activity data missed forecasts across investment, retail sales and industrial output, reigniting stimulus expectations.

- Equities fell 1-1.6% across Shanghai, CSI 300, Hang Seng and TAIEX while USD/CNY held near 6.80 after a weaker PBoC fix.

- Loan Prime Rate decision due tomorrow with markets pricing no change to the 1-year rate at 3% or 5-year at 3.5%.

Yesterday's Recap

Mainland China April data confirmed a broad-based slowdown, with fixed-asset investment resuming declines and both retail sales and industrial production falling short of consensus. Markets reacted with the Shanghai Composite closing at 4,135.39, down 1.02%, while the CSI 300 fell 1.12% to 4,859.59. Hong Kong’s Hang Seng dropped 1.62% to 25,962.73 and Taiwan’s TAIEX declined 1.39% to 41,172.36.

The PBoC set a weaker USD/CNY fixing, reinforcing expectations of gradual yuan depreciation as it defended the 6.80 level. Swap Connect trading volumes continued to build toward the 1 trillion yuan mark on rising hedging demand for yuan debt. Copper rose 1.35% to 6.34, reflecting resilient physical demand despite softer macro prints.

Thermal power generation rose for a fourth consecutive month even as coal output slipped, underscoring Beijing’s continued reliance on fossil fuels.

The Day Ahead

Markets will focus on the PBoC’s Loan Prime Rate announcement scheduled for 17:15 local time tomorrow, with both the 1-year and 5-year rates expected to remain unchanged at 3% and 3.5%. Analysts will parse any accompanying statement for signals on further policy easing amid the recent growth weakness. Hong Kong markets will monitor HKMA aggregate balance data for any shifts in liquidity conditions under the currency peg.

Taiwan will release export orders, providing an early read on semiconductor supply-chain momentum ahead of month-end trade figures.

Other Economic Notes

Property-sector concerns resurfaced after Evergrande liquidators filed an $8.4 billion claim against PwC entities in Hong Kong. Agricultural purchase commitments of at least $17 billion annually through 2028 under the US-China phase-one framework provide a modest offset to external demand risks. Cross-strait investment flows remain subdued amid ongoing geopolitical tensions.

China’s thermal power generation grew for a fourth straight month in April even as coal output fell, highlighting the challenges Beijing faces in controlling emissions while meeting electricity demand.