Greater China Macro Daily(Beta Mode)

China Data Misses Fuel LPR Hold Bets

Market Snapshot

| Asset | Level | Change |

|---|---|---|

| Shanghai Composite | 4,142.23 | +0.26% |

| CSI 300 | 4,818.41 | -0.31% |

| Hang Seng | 25,675.18 | -1.11% |

| TAIEX | 40,891.82 | -0.68% |

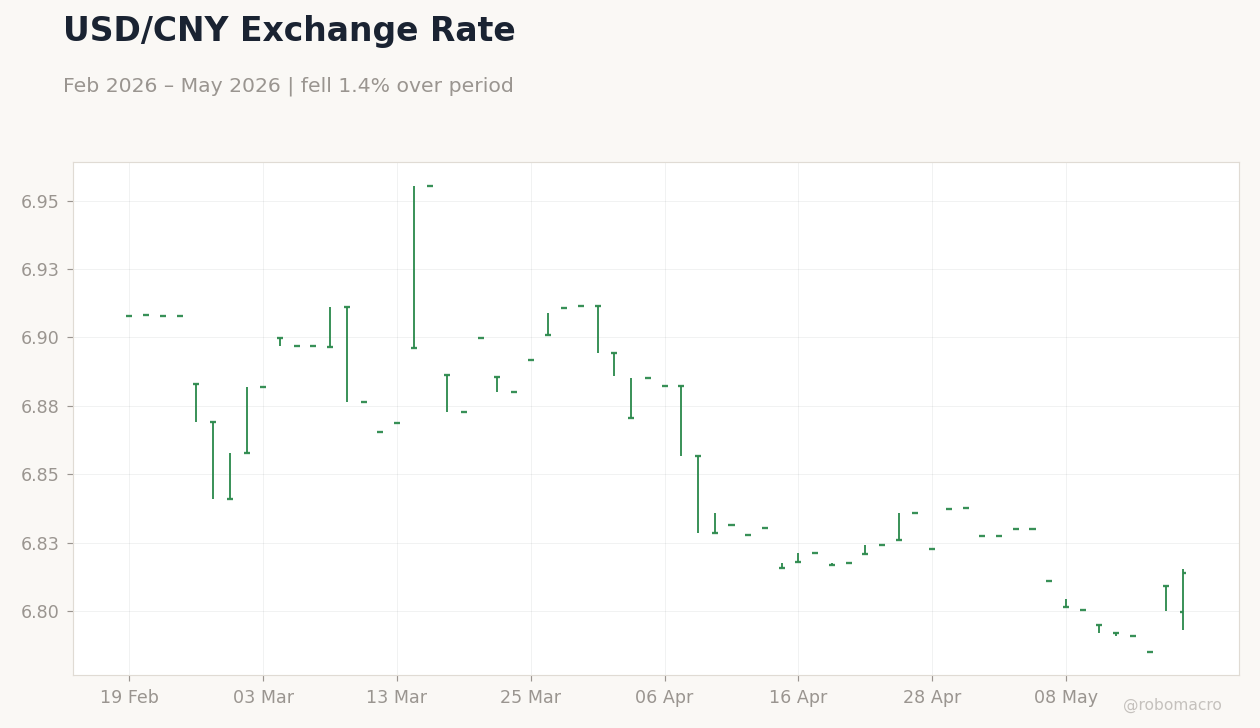

| USD/CNY | 6.81 | +0.07% |

| USD/HKD | 7.83 | +0.03% |

| Copper | 6.19 | -1.24% |

| Brent Crude | 111.00 | -0.98% |

| Gold | 4,485.40 | -1.47% |

| Bitcoin | 76,816.95 | -0.18% |

| China 2Y Govt Yield | - | - |

| China 10Y Govt Yield | - | - |

Prior Economic Events

| Data | Prior | Cons | Actual |

|---|---|---|---|

| No events available | |||

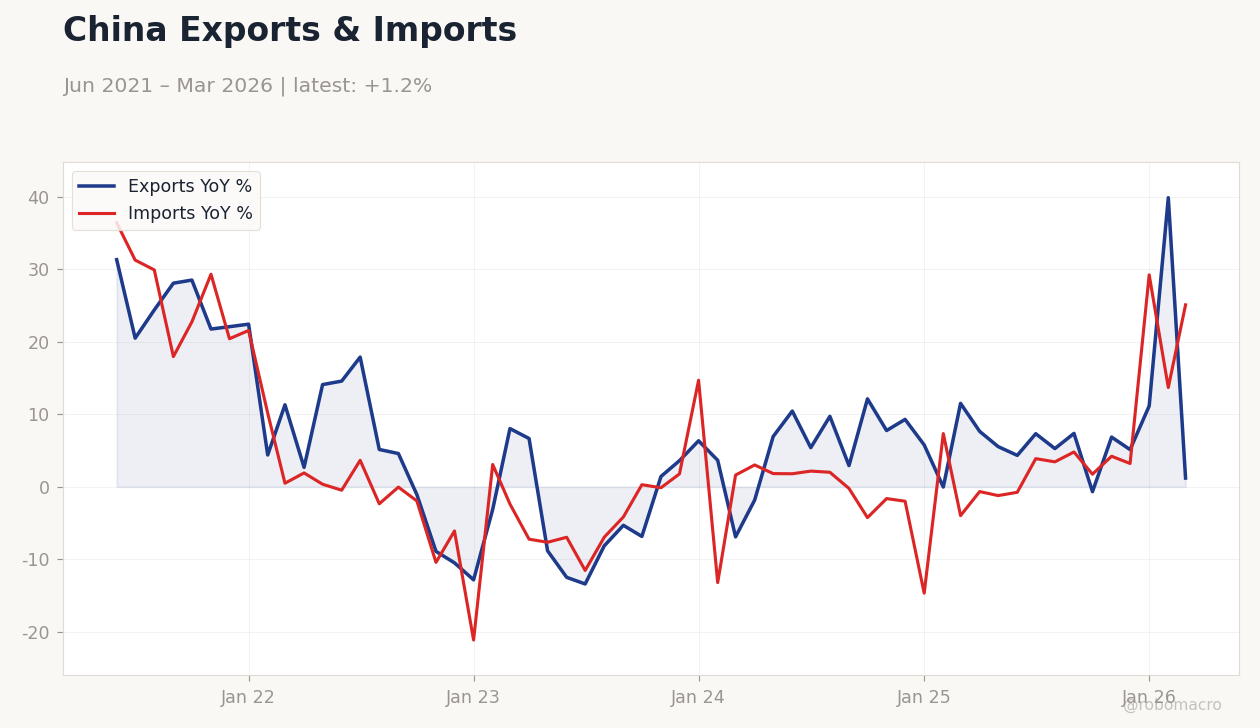

China Exports & Imports | Type: macro_line | Exports YoY %: 1.195 (2026-03-01) | Range: -13.41–39.86 | Trend(6pt): 31.32,5.14,-6.853,9.287,39.86,1.195 | Imports YoY %: 25.09 (2026-03-01) | Range: -21.14–36.4 | Trend(6pt): 36.4,-2.352,0.2797,-1.995,13.68,25.09

China Exports & Imports | Type: macro_line | Exports YoY %: 1.195 (2026-03-01) | Range: -13.41–39.86 | Trend(6pt): 31.32,5.14,-6.853,9.287,39.86,1.195 | Imports YoY %: 25.09 (2026-03-01) | Range: -21.14–36.4 | Trend(6pt): 36.4,-2.352,0.2797,-1.995,13.68,25.09

Today's Economic Events

| Data | Prior | Cons | Time |

|---|---|---|---|

| Loan Prime Rate 1Y | 3 | 3 | 17:15 |

| Loan Prime Rate 5Y | 3.50 | 3.50 | 17:15 |

- April industrial output and retail sales missed forecasts, prompting fresh stimulus speculation.

- PBoC set weaker USD/CNY fix while markets price limited LPR cuts today.

- Equities mixed as Shanghai rose 0.26% but Hang Seng fell 1.11% on growth concerns.

Yesterday's Recap

Mainland China April industrial production and retail sales both disappointed, with fixed-asset investment resuming declines and underscoring broad-based slowdown. The PBoC reinforced depreciation expectations by fixing USD/CNY weaker, while still defending the 6.8 level amid stimulus hopes. Shanghai Composite closed at 4,142.23, up 0.26%, whereas CSI 300 slipped 0.31% to 4,818.41 as investors rotated defensively.

Hong Kong’s Hang Seng dropped 1.11% to 25,675.18 and TAIEX fell 0.68% to 40,891.82, pressured by regional risk-off flows. USD/CNY edged 0.07% higher to 6.81 while USD/HKD held steady near 7.83, reflecting contained HKMA intervention. Copper declined 1.24% to 6.19 on softer China demand signals, and Brent Crude fell 0.98% to 111.00.

China’s April CPI at -0.10% y/y highlighted persistent deflationary pressures across the mainland economy.

The Day Ahead

Markets await the PBoC’s 1-year and 5-year Loan Prime Rate announcements scheduled for 17:15 ET today, with consensus pointing to unchanged prints at 3.00% and 3.50%. No major data releases are slated for Hong Kong or Taiwan tomorrow. Traders will monitor any State Council commentary for fresh property-sector support measures.

Yuan fixings and liquidity operations will remain in focus after yesterday’s weaker midpoint. Cross-strait trade data and semiconductor export updates from Taiwan are expected later this week.

Other Economic Notes

China’s thermal power generation rose for a fourth consecutive month even as coal output declined, highlighting energy-transition frictions. New-home prices in 70 cities extended their decline, keeping pressure on developers despite targeted bank lending. Swap Connect volumes are approaching 1 trillion yuan as foreign investors hedge rising yuan-debt holdings.

Broader stimulus expectations center on incremental RRR or LPR adjustments rather than large-scale fiscal packages.

Global Macro News

G7 finance ministers gathered in Paris amid mounting headwinds from tariffs and geopolitical tensions that threaten global growth. The US dollar index paused its recent rally as attention shifts to upcoming Fed minutes and PMI prints. <i>↓ p.2</i>