Greater China Macro Daily(Beta Mode)

PBoC Holds LPR Steady as Equities Slip

Market Snapshot

| Asset | Level | Change |

|---|---|---|

| Shanghai Composite | 4,077.28 | -2.04% |

| CSI 300 | 4,783.10 | -1.39% |

| Hang Seng | 25,651.12 | -0.57% |

| TAIEX | 40,020.82 | -0.39% |

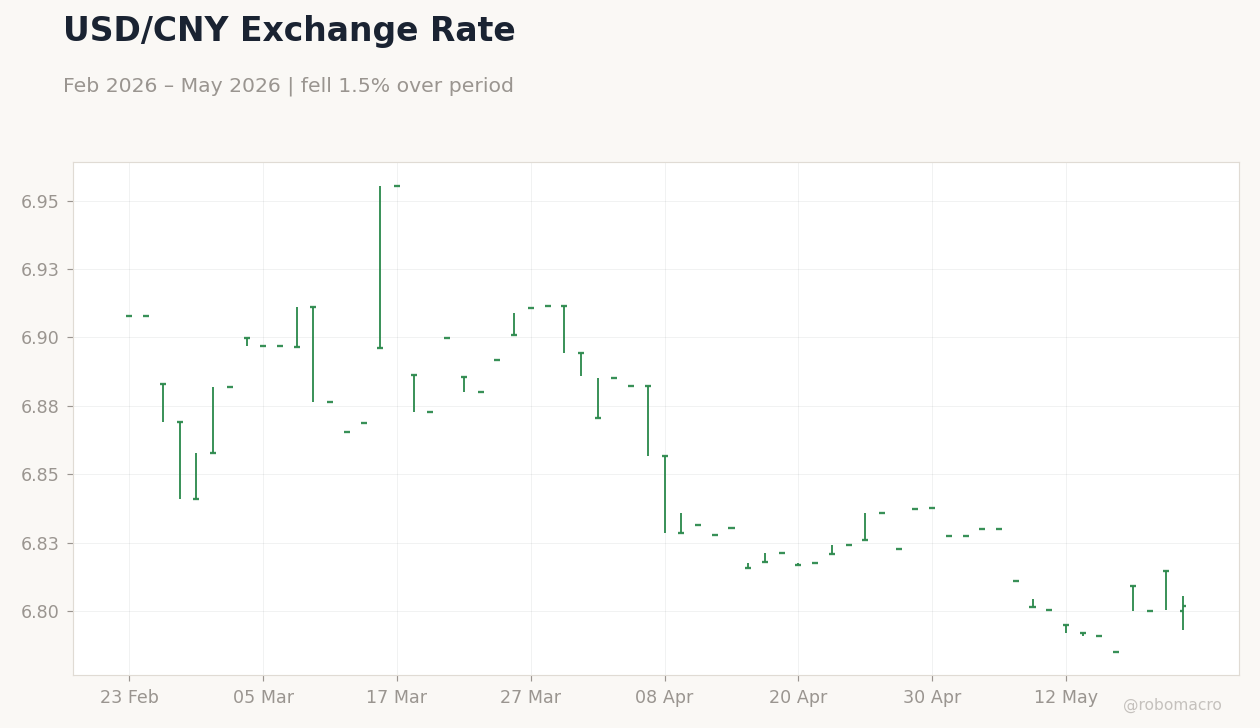

| USD/CNY | 6.80 | -0.18% |

| USD/HKD | 7.83 | +0.01% |

| Copper | 6.34 | +0.87% |

| Brent Crude | 104.88 | -0.13% |

| Gold | 4,544.20 | +0.28% |

| Bitcoin | 77,553.01 | +0.12% |

| China 2Y Govt Yield | - | - |

| China 10Y Govt Yield | - | - |

Prior Economic Events

| Data | Prior | Cons | Actual |

|---|---|---|---|

| Loan Prime Rate 1Y | 3 | 3 | 3 |

| Loan Prime Rate 5Y | 3.50 | 3.50 | 3.50 |

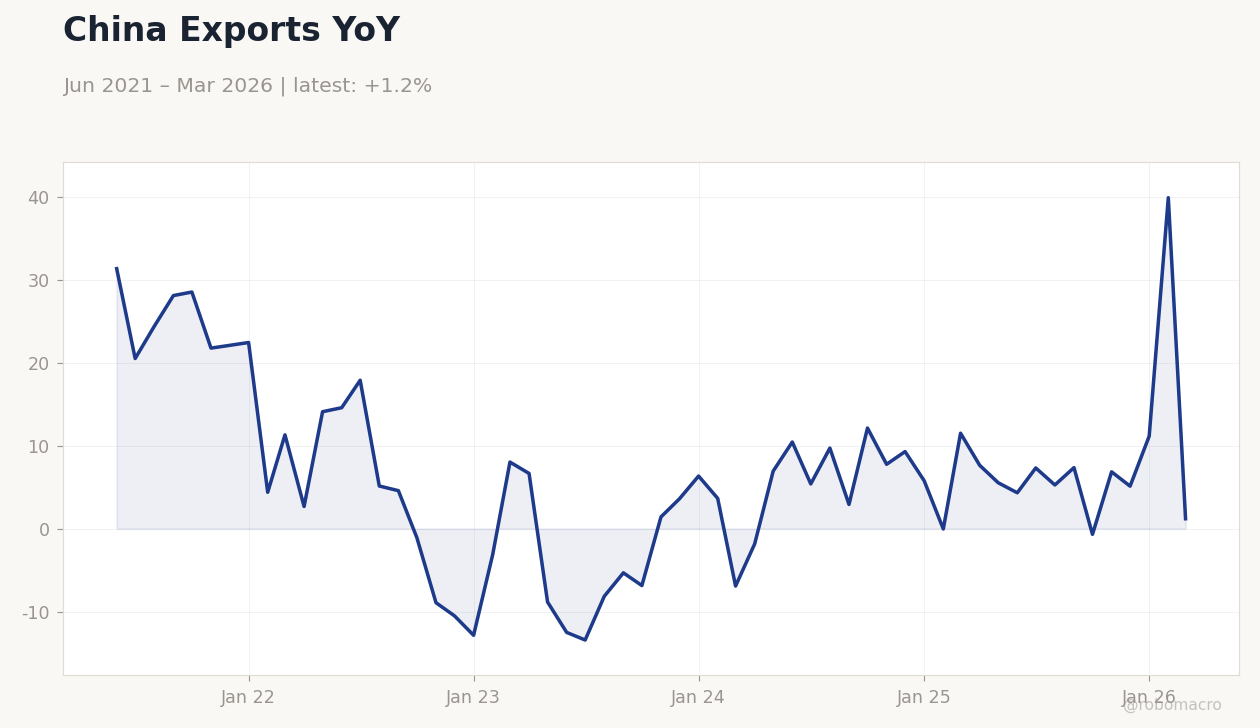

China Exports YoY | Type: macro_line | YoY %: 1.195 (2026-03-01) | Range: -13.41–39.86 | Trend(6pt): 31.32,5.14,-6.853,9.287,39.86,1.195

China Exports YoY | Type: macro_line | YoY %: 1.195 (2026-03-01) | Range: -13.41–39.86 | Trend(6pt): 31.32,5.14,-6.853,9.287,39.86,1.195

Today's Economic Events

| Data | Prior | Cons | Time |

|---|---|---|---|

| No events available | |||

- PBoC kept 1Y and 5Y Loan Prime Rates unchanged at 3% and 3.5%, signaling a cautious policy stance amid mixed growth signals.

- Mainland Chinese equities declined sharply, with Shanghai Composite falling 2.04% to 4,077.28 and CSI 300 dropping 1.39% to 4,783.10.

- Hong Kong advanced its gold-clearing system launch targeted for July to strengthen bullion trading hub status.

Yesterday's Recap

The PBoC held both Loan Prime Rates steady in May, matching consensus and prior levels, which reinforced market views of measured easing rather than aggressive stimulus. Mainland equities extended losses on the decision, with the Shanghai Composite closing at 4,077.28 and the CSI 300 at 4,783.10 as investors digested limited policy follow-through. Hong Kong’s Hang Seng Index eased 0.57% to 25,651.12 while Taiwan’s TAIEX declined 0.39% to 40,020.82 amid semiconductor sector rotation.

The USD/CNY rate tightened 0.18% to 6.80, reflecting modest yuan support from steady rates and ongoing trade surplus reduction calls. Copper rose 0.87% to 6.34 on fresh China demand signals, while Brent crude slipped 0.13% to 104.88 and gold advanced 0.28% to 4,544.20. HKMA aggregate balance remained stable near the peg level of 7.83 for USD/HKD, with no intervention reported.

The Day Ahead

No major data releases or central bank decisions are scheduled for mainland China, Hong Kong or Taiwan today or tomorrow. Markets will monitor follow-up comments from the PBoC on liquidity operations and any State Council signals on property easing. Traders will also watch USD/CNY flows for signs of further yuan strengthening after recent ex-mayor remarks on tariff cuts.

Hong Kong’s preparations for the July gold-clearing system launch may generate incremental market commentary. Cross-strait trade data and semiconductor export trends from Taiwan remain the next potential catalysts.

Other Economic Notes

China’s bond market continued to diverge from global peers, with yields anchored near nine-month lows on fragile recovery and ample liquidity. Calls from former officials for a stronger yuan and tariff reductions aim to narrow the trade surplus while supporting domestic consumption. Property sector support measures, including accelerated mortgage rate cuts in tier-2 cities, remain the primary near-term policy lever.

Indonesia’s decision to allow exporters to hold yuan earnings adds a new layer to regional currency usage and commodity trade flows.