Greater China Macro Daily(Beta Mode)

Equities Rally as China Stimulus Hopes Build

Market Snapshot

| Asset | Level | Change |

|---|---|---|

| Shanghai Composite | 4,112.90 | +0.87% |

| CSI 300 | 4,845.10 | +1.30% |

| Hang Seng | 25,606.03 | +0.86% |

| TAIEX | 42,267.97 | +2.17% |

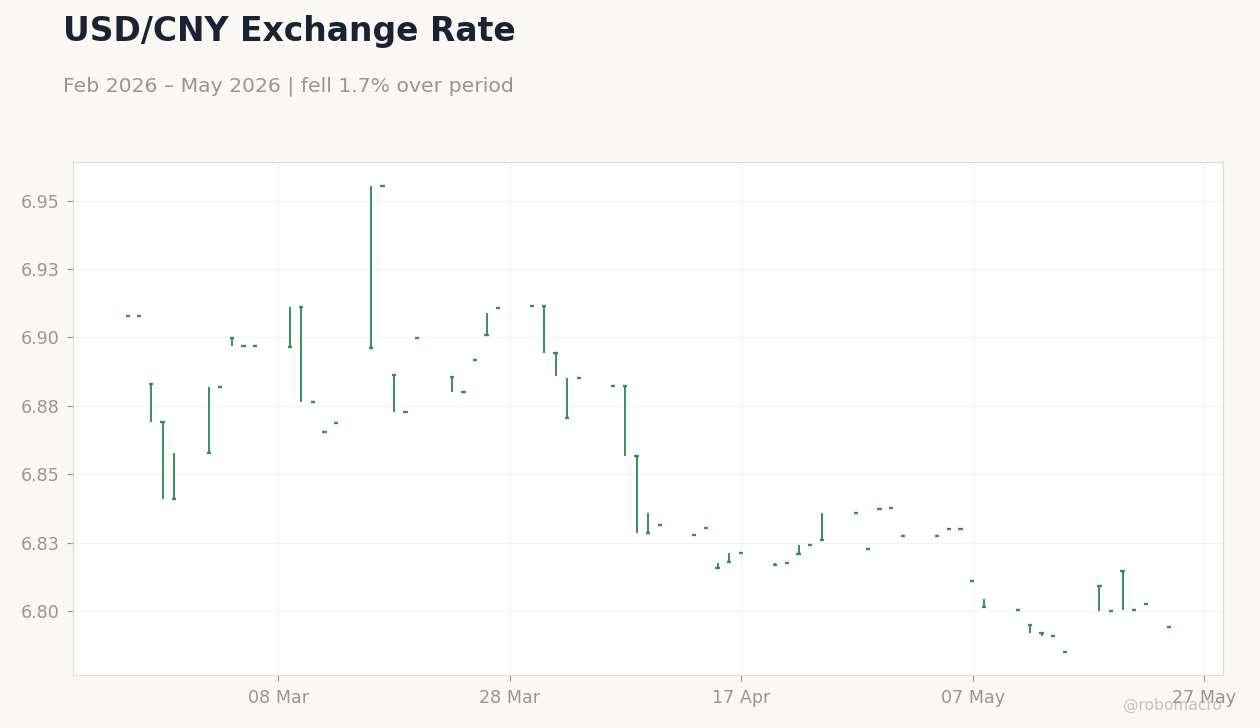

| USD/CNY | 6.79 | -0.12% |

| USD/HKD | 7.84 | +0.02% |

| Copper | 6.38 | +1.95% |

| Brent Crude | 100.21 | -2.31% |

| Gold | 4,523.20 | -0.37% |

| Bitcoin | 76,227.60 | -0.58% |

| China 2Y Govt Yield | - | - |

| China 10Y Govt Yield | - | - |

Prior Economic Events

| Data | Prior | Cons | Actual |

|---|---|---|---|

| No events available | |||

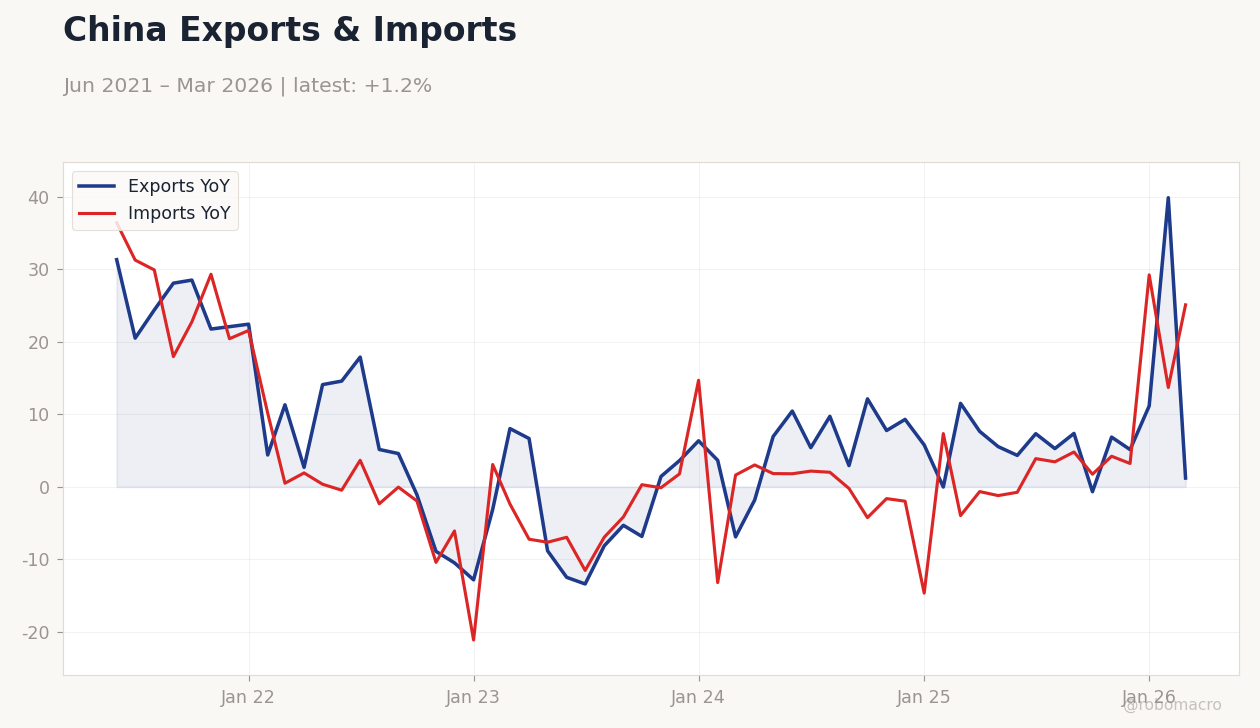

China Exports & Imports | Type: macro_line | Exports YoY: 1.195 (2026-03-01) | Range: -13.41–39.86 | Trend(6pt): 31.32,5.14,-6.853,9.287,39.86,1.195 | Imports YoY: 25.09 (2026-03-01) | Range: -21.14–36.4 | Trend(6pt): 36.4,-2.352,0.2797,-1.995,13.68,25.09

China Exports & Imports | Type: macro_line | Exports YoY: 1.195 (2026-03-01) | Range: -13.41–39.86 | Trend(6pt): 31.32,5.14,-6.853,9.287,39.86,1.195 | Imports YoY: 25.09 (2026-03-01) | Range: -21.14–36.4 | Trend(6pt): 36.4,-2.352,0.2797,-1.995,13.68,25.09

Today's Economic Events

| Data | Prior | Cons | Time |

|---|---|---|---|

| NBS Manufacturing PMI | 50.30 | - | 21:30 |

| NBS Non-Manufacturing PMI | 49.40 | - | 21:30 |

- Mainland and Taiwan equities posted strong gains on stimulus expectations and semiconductor strength.

- China-Africa trade ties deepened with tariff removals while export curbs on chemicals signaled US cooperation.

- HKMA maintained the USD/HKD peg with no stress evident in aggregate balance or interbank rates.

Yesterday's Recap

Mainland equities advanced with the Shanghai Composite rising 0.87% to 4,112.90 and the CSI 300 climbing 1.30% to 4,845.10 amid reports of expanded local-government bond quotas. Hong Kong’s Hang Seng Index gained 0.86% to 25,606.03 while Taiwan’s TAIEX surged 2.17% to 42,267.97 on robust semiconductor export orders. USD/CNY eased 0.12% to 6.79, reflecting mild yuan strength, and USD/HKD held steady at 7.84 inside the peg band.

Copper climbed 1.95% to 6.38 on China demand optimism while Brent crude fell 2.31% to 100.21. No major data releases occurred on 23 May across Greater China. HKMA urged Standard Chartered to clarify its CEO’s “lower-value human capital” remarks and separately warned the public on banking scams.

The Day Ahead

Markets will monitor the 30 May release of NBS Manufacturing PMI and Non-Manufacturing PMI, both due at 21:30 ET, for fresh readings on mainland activity. Industrial production and retail-sales figures scheduled for later in the week remain the next high-frequency indicators. Cross-strait investment flows may draw attention at the ongoing Fuzhou Cross-Strait Fair.

No policy meetings are calendared for the PBoC, HKMA or CBC this week. Traders will also track any follow-through on China’s new chemical export controls to the US.

Other Economic Notes

Guangzhou and Shenzhen expanded developer white-list financing, supporting property-sector sentiment. China removed tariffs on African imports to counter US trade restrictions and expand sourcing of coffee and other commodities. A deadly coal-mine blast highlighted limits to Beijing’s energy-security drive despite record domestic output.

Taiwan advanced plans to scale drone manufacturing to 100,000 units monthly by 2030, strengthening supply-chain resilience.

Global Macro News

Global factory activity weakened further under persistent inflation and energy-price pressure linked to the Iran conflict. US Fed Chair Powell noted resilient domestic demand while signaling caution on consumer spending. Japan’s solid Q1 GDP faces downside risks from higher energy costs and potential yen intervention near 160.

<i>↓ p.2</i>