Greater China Macro Daily(Beta Mode)

Yuan Hits 3-Year High as FDI Weakens

Market Snapshot

| Asset | Level | Change |

|---|---|---|

| Shanghai Composite | 4,112.90 | +0.87% |

| CSI 300 | 4,845.10 | +1.30% |

| Hang Seng | 25,606.03 | +0.86% |

| TAIEX | 42,267.97 | +2.17% |

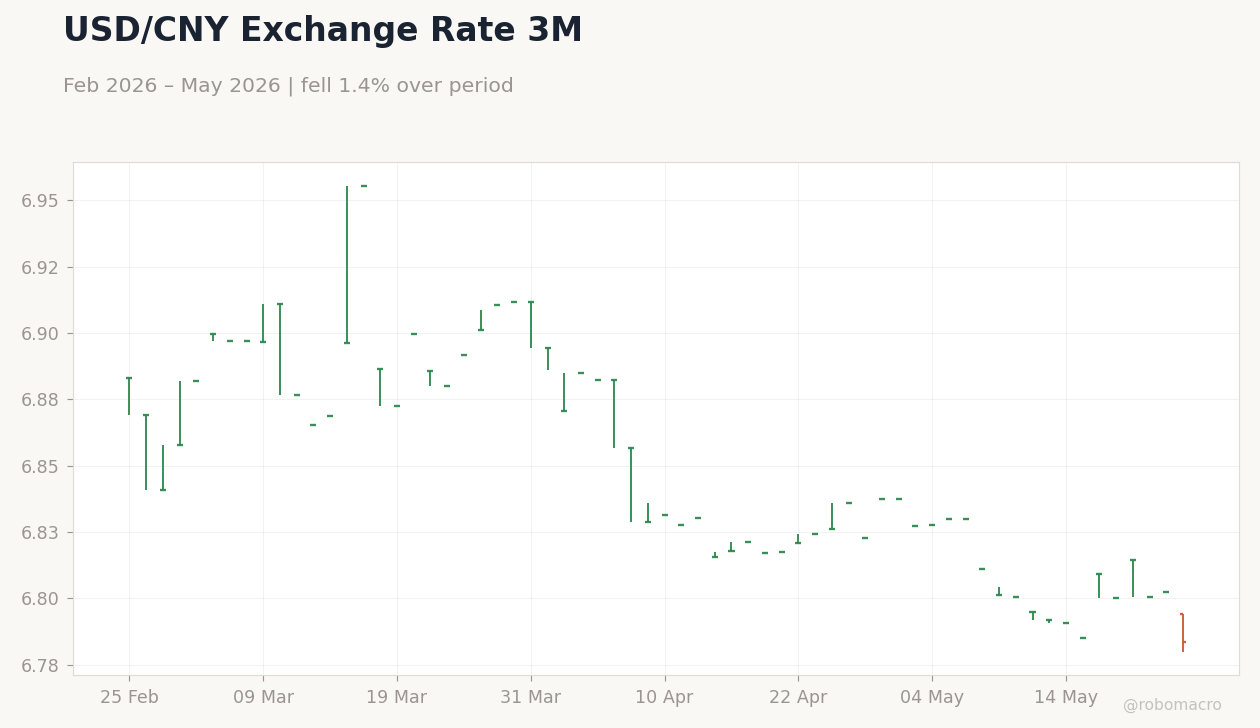

| USD/CNY | 6.78 | -0.28% |

| USD/HKD | 7.83 | -0.01% |

| Copper | 6.38 | +0.58% |

| Brent Crude | 100.21 | -3.22% |

| Gold | 4,523.20 | +0.05% |

| Bitcoin | 77,230.85 | +0.32% |

| China 2Y Govt Yield | - | - |

| China 10Y Govt Yield | - | - |

Prior Economic Events

| Data | Prior | Cons | Actual |

|---|---|---|---|

| FDI (YTD) Year-over-Year | -7.30 | - | -10.30 |

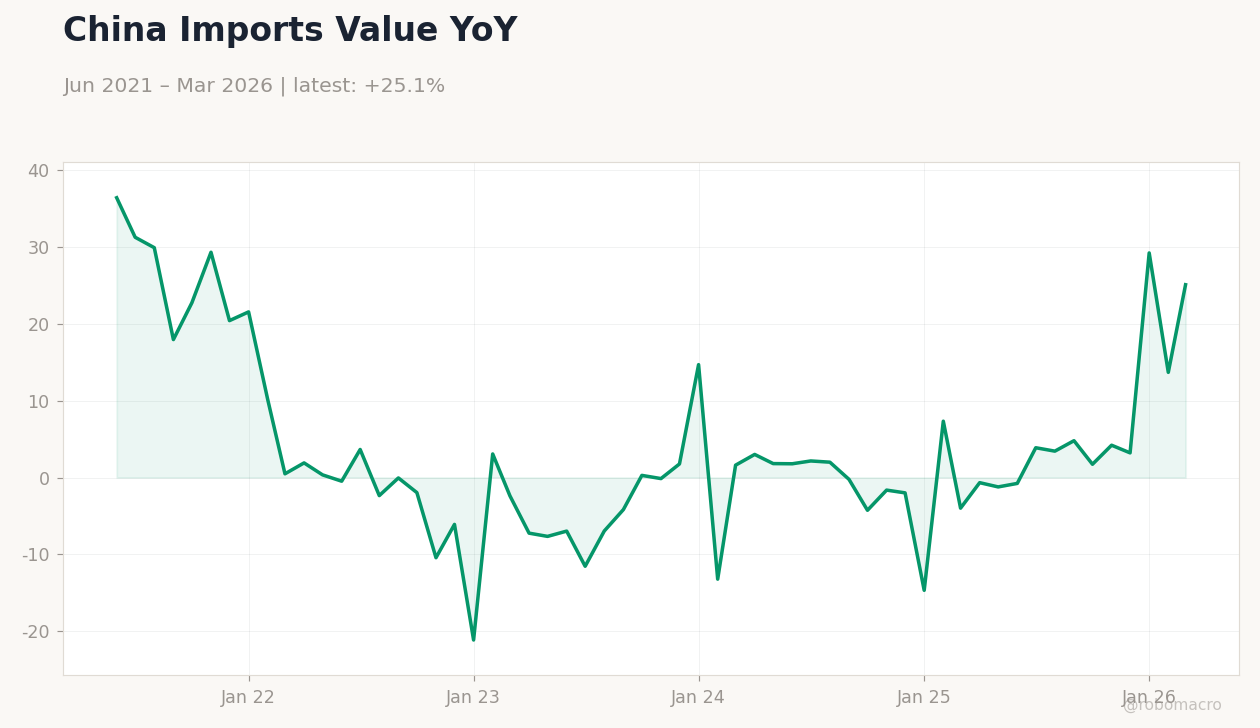

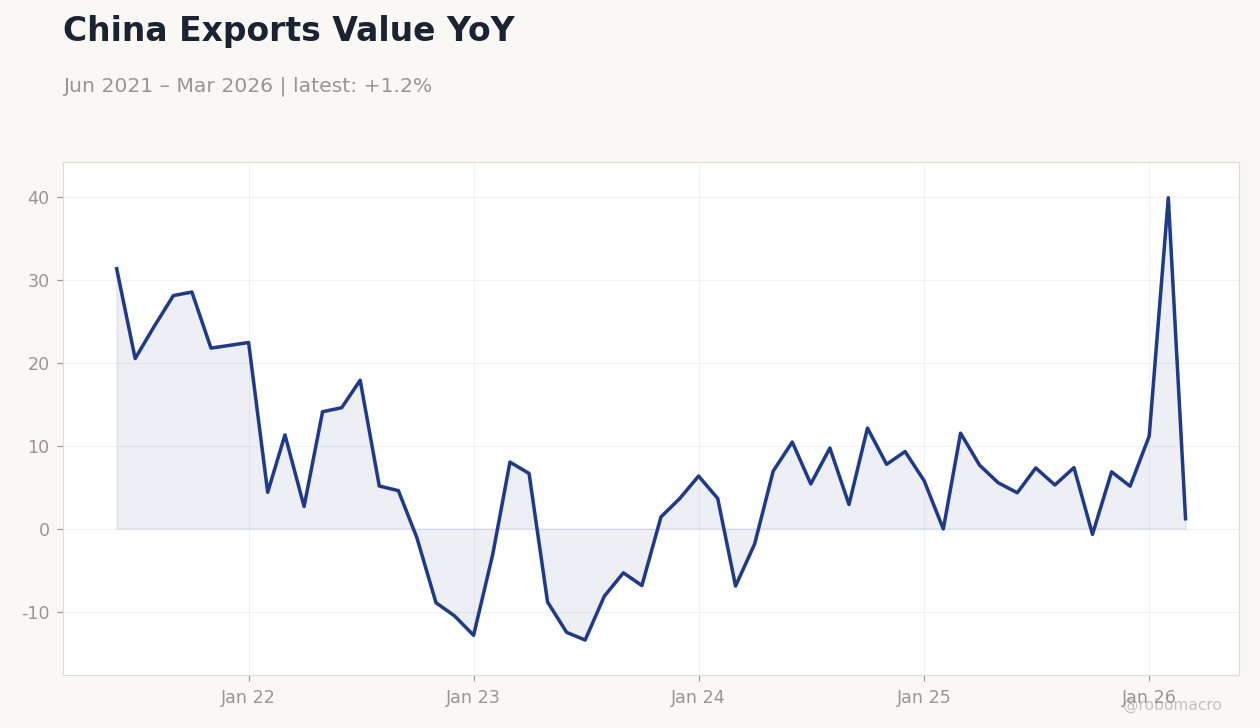

China Exports Value YoY | Type: macro_line | YoY %: 1.195 (2026-03-01) | Range: -13.41–39.86 | Trend(6pt): 31.32,5.14,-6.853,9.287,39.86,1.195

China Exports Value YoY | Type: macro_line | YoY %: 1.195 (2026-03-01) | Range: -13.41–39.86 | Trend(6pt): 31.32,5.14,-6.853,9.287,39.86,1.195

Today's Economic Events

| Data | Prior | Cons | Time |

|---|---|---|---|

| NBS Manufacturing PMI | 50.30 | - | 21:30 |

| NBS Non-Manufacturing PMI | 49.40 | - | 21:30 |

| RatingDog Manufacturing PMI | 52.20 | - | 21:45 |

- China FDI (YTD) YoY fell to -10.3% in the latest reading, worse than the prior -7.3% and signaling persistent foreign investor caution.

- Equities across Greater China advanced, with CSI 300 up 1.30% and TAIEX surging 2.17%, while USD/CNY eased 0.28% to 6.78.

- HKMA maintained the USD/HKD peg near 7.83 amid stable aggregate balance and issued fresh warnings on banking scams.

Yesterday's Recap

Mainland China reported FDI (YTD) YoY at -10.3%, extending the contraction and underscoring subdued inbound investment. Equity markets posted solid gains, with Shanghai Composite rising 0.87% and CSI 300 climbing 1.30% on improved risk sentiment. The yuan strengthened to its strongest level in three years against the dollar, supported by Hormuz Strait negotiations that lifted broader risk appetite.

Hong Kong’s Hang Seng index advanced 0.86%, while Taiwan’s TAIEX outperformed with a 2.17% rally. Copper gained 0.58% to 6.38, contrasting with Brent crude’s 3.22% drop to 100.21. No major data releases emerged from Hong Kong or Taiwan.

Cross-strait trade promotion events in Fuzhou highlighted ongoing investment flows.

The Day Ahead

Markets await China’s May NBS Manufacturing PMI and Non-Manufacturing PMI, both scheduled for release on 30 May at 21:30 ET. The RatingDog Manufacturing PMI follows later the same evening. Traders will monitor any signals on factory activity amid ongoing property sector weakness and external tariff shifts.

Hong Kong and Taiwan calendars remain light, with focus likely staying on yuan volatility and regional equity flows. No central-bank meetings are flagged for the immediate session.

Other Economic Notes

China’s removal of tariffs on African goods aims to offset U.S. trade restrictions and secure alternative export markets. Domestic consumers are shifting toward homegrown luxury products, including high-end EVs, as foreign brands lose ground.

New export controls on chemical precursors to the U.S., Mexico and Canada reflect Beijing’s cooperation on fentanyl-related enforcement. Coal output remains robust yet faces scrutiny after a deadly mine blast that tests energy-security priorities. These developments collectively point to a policy mix favoring domestic resilience and selective trade realignment.

Global Macro News

Global risk appetite improved following progress in U.S.-Iran talks, supporting yuan strength and equity inflows into Greater China. U.S. <i>↓ p.2</i>