Greater China Macro Daily(Beta Mode)

Yuan Hits 3-Year High as TAIEX Surges

Market Snapshot

| Asset | Level | Change |

|---|---|---|

| Shanghai Composite | 4,145.37 | -0.17% |

| CSI 300 | 4,947.85 | +0.53% |

| Hang Seng | 25,606.03 | +0.86% |

| TAIEX | 43,644.40 | +3.26% |

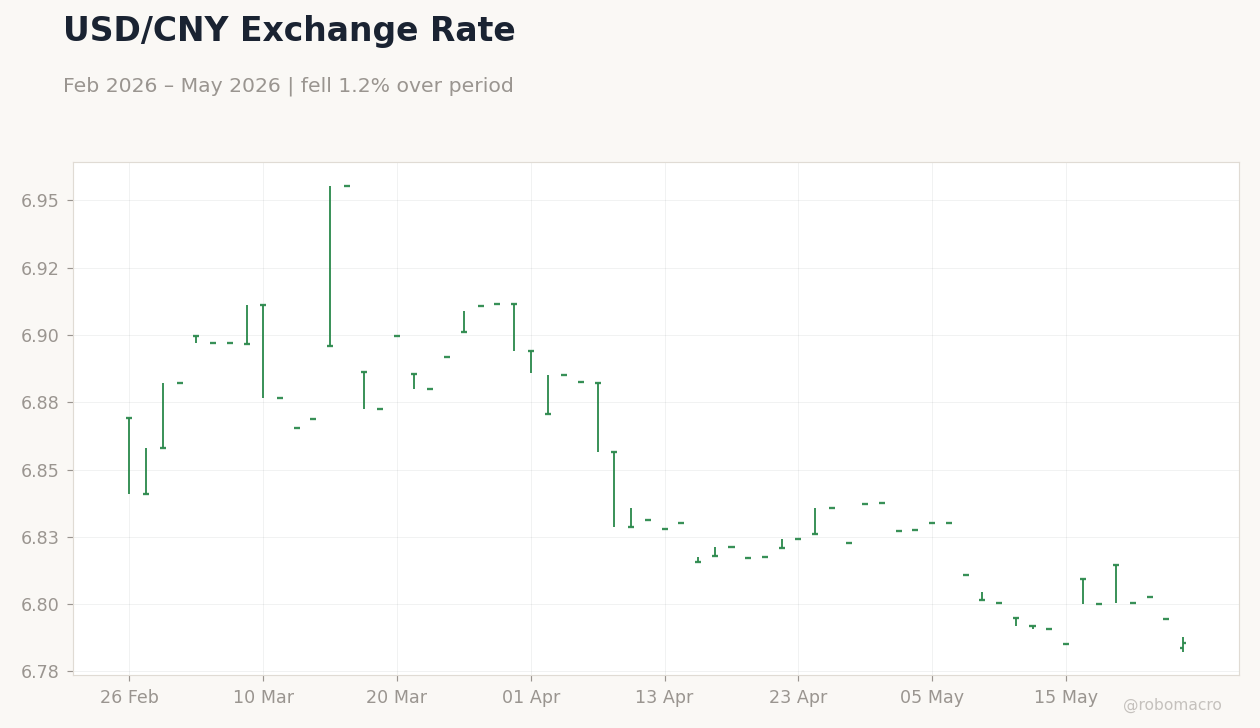

| USD/CNY | 6.79 | -0.13% |

| USD/HKD | 7.84 | +0.01% |

| Copper | 6.42 | +1.29% |

| Brent Crude | 96.59 | -6.71% |

| Gold | 4,507.30 | -0.30% |

| Bitcoin | 75,824.55 | -1.88% |

| China 2Y Govt Yield | - | - |

| China 10Y Govt Yield | - | - |

Prior Economic Events

| Data | Prior | Cons | Actual |

|---|---|---|---|

| No events available | |||

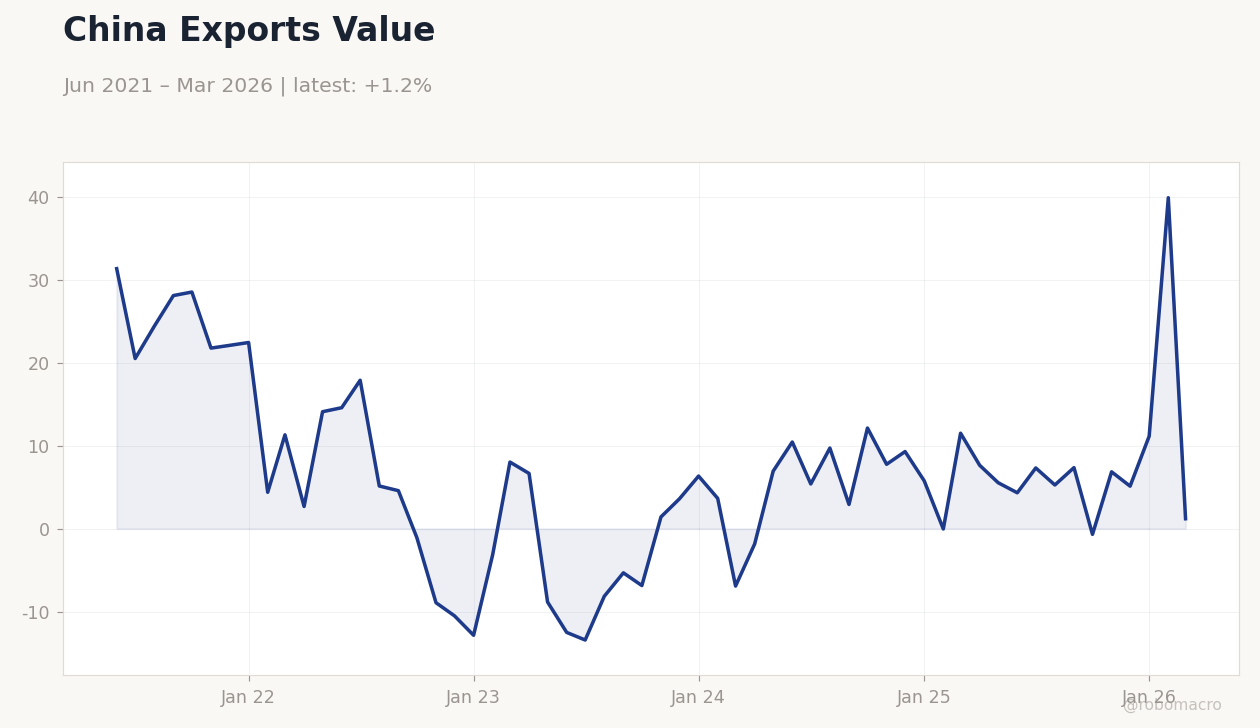

China Exports Value | Type: macro_line | Exports (USD mn): 1.195 (2026-03-01) | Range: -13.41–39.86 | Trend(6pt): 31.32,5.14,-6.853,9.287,39.86,1.195

China Exports Value | Type: macro_line | Exports (USD mn): 1.195 (2026-03-01) | Range: -13.41–39.86 | Trend(6pt): 31.32,5.14,-6.853,9.287,39.86,1.195

Today's Economic Events

| Data | Prior | Cons | Time |

|---|---|---|---|

| NBS Manufacturing PMI | 50.30 | - | 17:30 |

| NBS Non-Manufacturing PMI | 49.40 | - | 17:30 |

- Mainland equities closed mixed with CSI 300 rising 0.53% to 4,947.85 while Shanghai Composite fell 0.17% to 4,145.37 on stimulus hopes.

- TAIEX jumped 3.26% to 43,644.40, overtaking India as the world’s fifth-largest stock market amid semiconductor strength.

- USD/CNY fell 0.13% to 6.79, reaching its strongest level in three years as risk appetite improved.

Yesterday's Recap

Mainland China markets showed divergence as CSI 300 advanced on reports of expanded local-government bond quotas while Shanghai Composite eased modestly. Hong Kong’s Hang Seng rose 0.86% to 25,606.03, supported by improved sentiment toward property names. Taiwan’s TAIEX posted a sharp 3.26% gain to 43,644.40, driven by Taiwan Semiconductor Manufacturing Co.

order visibility and the island overtaking India in market capitalization. The yuan strengthened to 6.79 against the dollar, its highest level since 2023, aided by higher risk appetite following Hormuz Strait negotiations. Copper climbed 1.29% to 6.42 as a China growth proxy while Brent crude dropped 6.71% to 96.59.

No high-impact data releases occurred in Greater China on 25 May. HKMA aggregate balance stayed steady with no intervention required to defend the peg.

The Day Ahead

Markets will focus on China’s 30 May NBS Manufacturing PMI, expected to build on the prior 50.3 print and clarify the strength of the recent recovery. The accompanying Non-Manufacturing PMI will be watched for signs of stabilization in services after the last reading of 49.4. PBoC will conduct 7-day reverse repos and a 1-year MLF operation, with liquidity injections likely to remain ample ahead of month-end.

No rate decisions are scheduled from HKMA or CBC this week. Taiwan will release updated semiconductor export figures on 3 June that could reinforce the island’s supply-chain resilience.

Other Economic Notes

China’s decision to eliminate tariffs on African imports is widening trade channels as U.S. access tightens for those economies. Domestic luxury demand is shifting toward homegrown brands, reflecting slower overall consumption growth.

Aluminum prices are approaching four-year highs on fears of further output curbs in top producer China. Property developer Country Garden resumed interest payments on two USD bonds, easing near-term default concerns. Broader fixed-income markets continue to price higher long-term yields, increasing pressure on regional capital flows.