Greater China Macro Daily(Beta Mode)

Equities Slip Ahead of China PMI; Brent Plunges

Market Snapshot

| Asset | Level | Change |

|---|---|---|

| Shanghai Composite | 4,093.73 | -1.25% |

| CSI 300 | 4,908.17 | -0.80% |

| Hang Seng | 25,599.45 | -0.03% |

| TAIEX | 43,525.37 | -0.27% |

| USD/CNY | 6.78 | -0.11% |

| USD/HKD | 7.83 | -0.02% |

| Copper | 6.33 | -0.43% |

| Brent Crude | 93.60 | -6.01% |

| Gold | 4,481.60 | -0.42% |

| Bitcoin | 74,210.47 | -2.13% |

| China 2Y Govt Yield | - | - |

| China 10Y Govt Yield | - | - |

Prior Economic Events

| Data | Prior | Cons | Actual |

|---|---|---|---|

| No events available | |||

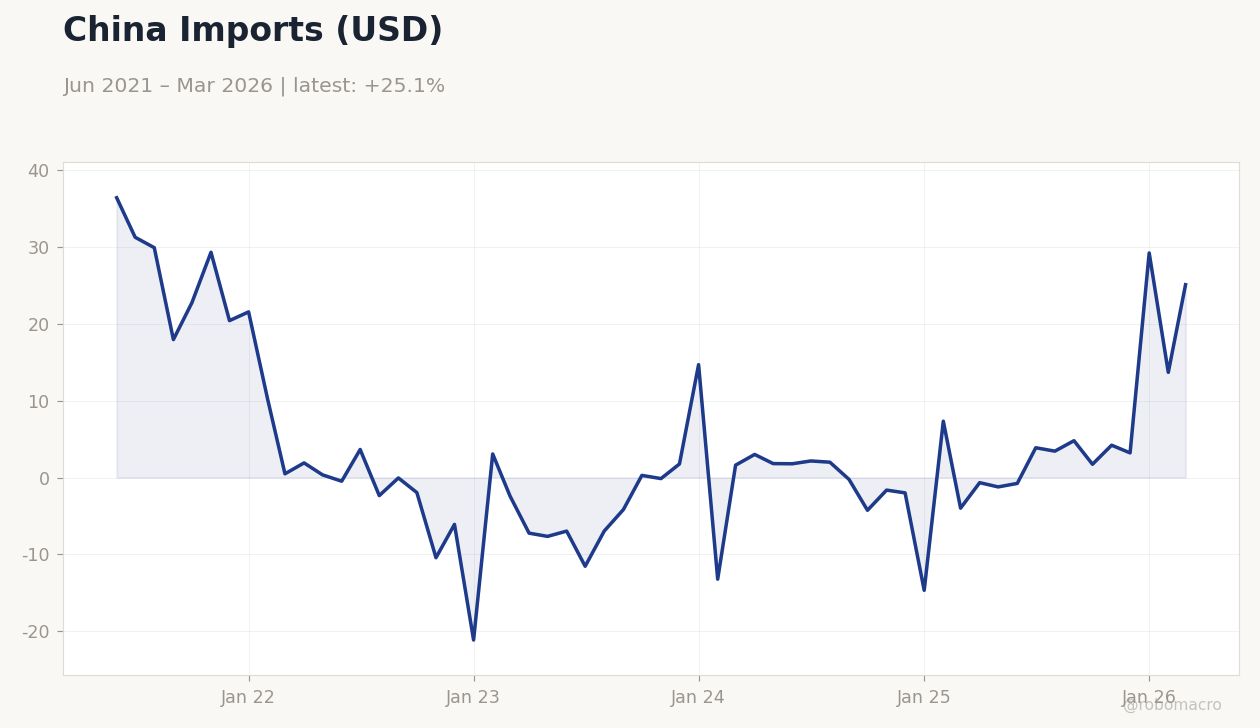

China Imports (USD) | Type: macro_line | USD bn: 25.09 (2026-03-01) | Range: -21.14–36.4 | Trend(6pt): 36.4,-2.352,0.2797,-1.995,13.68,25.09

China Imports (USD) | Type: macro_line | USD bn: 25.09 (2026-03-01) | Range: -21.14–36.4 | Trend(6pt): 36.4,-2.352,0.2797,-1.995,13.68,25.09

Today's Economic Events

| Data | Prior | Cons | Time |

|---|---|---|---|

| NBS Manufacturing PMI | 50.30 | - | 17:30 |

| NBS Non-Manufacturing PMI | 49.40 | - | 17:30 |

- Shanghai Composite fell 1.25% to 4,093.73 while CSI 300 declined 0.80% to 4,908.17 on weak sentiment.

- Brent crude dropped 6.01% to 93.60 amid Middle East tensions and China-Japan Treasury selling.

- NBS Manufacturing and Non-Manufacturing PMI releases due May 30 will test growth momentum.

Yesterday's Recap

Mainland Chinese equities posted broad losses on May 26 with the Shanghai Composite closing at 4,093.73, down 1.25%, and the CSI 300 at 4,908.17, down 0.80%. Hong Kong’s Hang Seng index edged 0.03% lower to 25,599.45 while Taiwan’s TAIEX slipped 0.27% to 43,525.37. USD/CNY eased 0.11% to 6.78 and USD/HKD held near 7.83 with no peg pressure evident.

Copper fell 0.43% to 6.33 as growth concerns resurfaced, while Brent crude plunged 6.01% to 93.60 on geopolitical shockwaves. News flow highlighted China’s K-shaped industrial profit split favoring AI-linked sectors and new HKMA rules tightening verification for mainland investment accounts retroactive to January 2023. No macro data prints occurred in Greater China on the session.

The Day Ahead

Markets will focus on the May 30 release of China’s NBS Manufacturing PMI, previously 50.3, and Non-Manufacturing PMI, previously 49.4, both due at 17:30 ET. No data releases are scheduled for mainland China, Hong Kong or Taiwan on May 28. PBoC liquidity operations and any State Council policy signals will be monitored for RRR hints.

Taiwan semiconductor export figures due later in the week could move TAIEX and supply-chain names. HKMA aggregate balance and USD/HKD peg mechanics remain in focus but no policy meetings are planned.

Other Economic Notes

China’s industrial profits continue showing K-shaped divergence with gains concentrated in AI-exposed sectors while broader manufacturing lags. Beijing’s decision to eliminate tariffs on African imports aims to offset U.S. trade barriers and secure raw-material flows.

Elevated global aluminum prices risk triggering record Chinese exports as domestic consumption faces price caps. Property-sector support measures announced earlier have yet to lift broader credit demand or reverse deflationary CPI prints near -0.10% YoY.

Global Macro News

Surging U.S. long-term yields prompted China and Japan to reduce Treasury holdings, adding pressure on global duration markets. The flashing-red U.S.

bond market is now pricing fiscal and policy volatility more typical of emerging economies. Minneapolis Fed’s Kashkari warned that inflation risks remain elevated, complicating any near-term pivot. <i>↓ p.2</i>