Greater China Macro Daily(Beta Mode)

AI Exports Ease Yuan Pressure Ahead of China PMI

Market Snapshot

| Asset | Level | Change |

|---|---|---|

| Shanghai Composite | 4,098.64 | +0.12% |

| CSI 300 | 4,914.21 | +0.12% |

| Hang Seng | 25,328.23 | -1.06% |

| TAIEX | 44,256.80 | +1.68% |

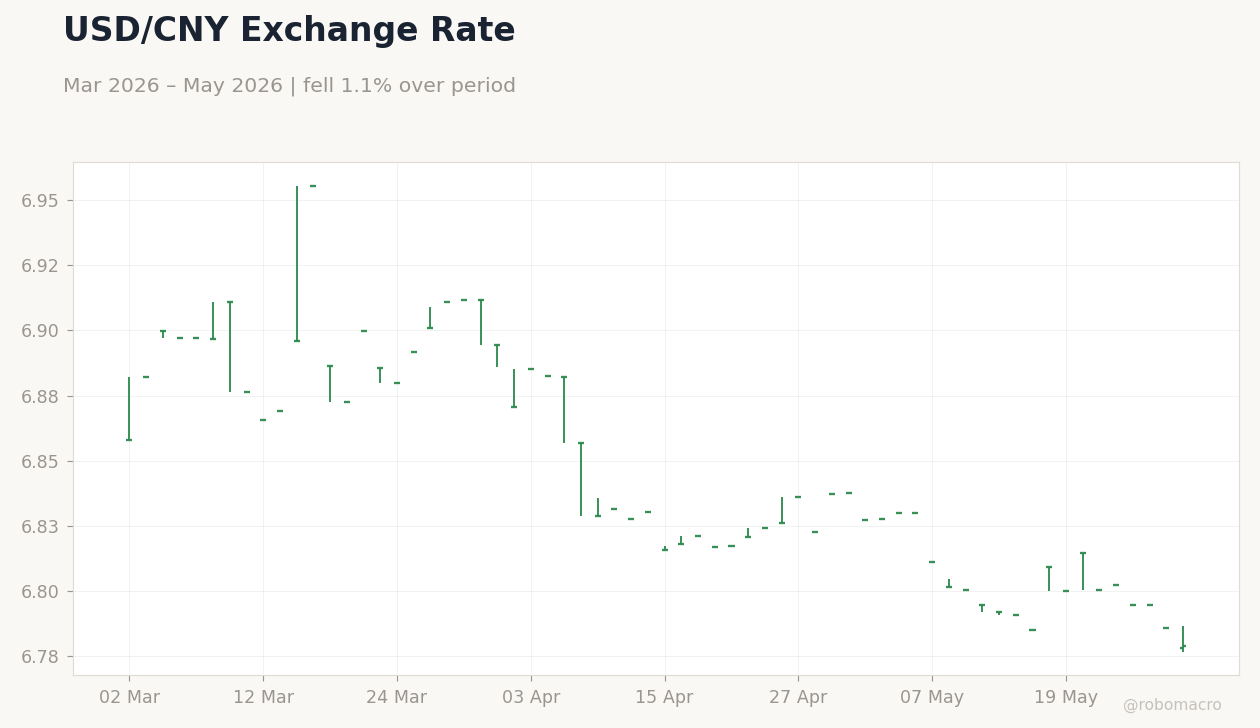

| USD/CNY | 6.78 | -0.10% |

| USD/HKD | 7.83 | -0.03% |

| Copper | 6.42 | +1.90% |

| Brent Crude | 92.48 | -1.92% |

| Gold | 4,527.30 | +1.79% |

| Bitcoin | 73,825.86 | -0.70% |

| China 2Y Govt Yield | - | - |

| China 10Y Govt Yield | - | - |

Prior Economic Events

| Data | Prior | Cons | Actual |

|---|---|---|---|

| No events available | |||

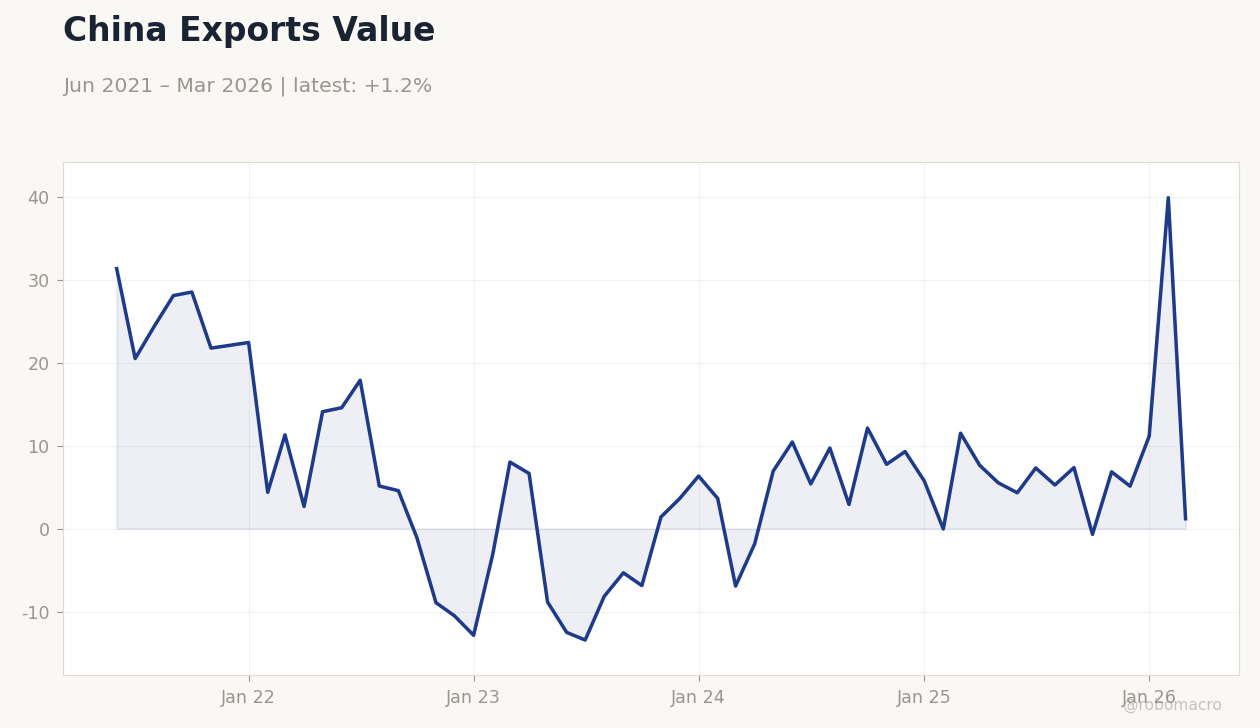

China Exports Value | Type: macro_line | USD bn: 1.195 (2026-03-01) | Range: -13.41–39.86 | Trend(6pt): 31.32,5.14,-6.853,9.287,39.86,1.195

China Exports Value | Type: macro_line | USD bn: 1.195 (2026-03-01) | Range: -13.41–39.86 | Trend(6pt): 31.32,5.14,-6.853,9.287,39.86,1.195

Today's Economic Events

| Data | Prior | Cons | Time |

|---|---|---|---|

| NBS Manufacturing PMI | 50.30 | - | 17:30 |

| NBS Non-Manufacturing PMI | 49.40 | - | 17:30 |

- China equities rose modestly as AI-driven exports eased yuan pressure, while Hong Kong shares fell on new HKMA account rules.

- PBOC fixed USD/CNY at 6.8240; pork prices at 16-year lows signal persistent weak domestic demand.

- TAIEX surged 1.68% on Nvidia’s $150bn annual Taiwan investment pledge; copper rallied 1.90% on China growth hopes.

Yesterday's Recap

Mainland China markets closed higher with the Shanghai Composite gaining 0.12% to 4,098.64 and CSI 300 also up 0.12% to 4,914.21. Hong Kong’s Hang Seng declined 1.06% to 25,328.23 after the HKMA ordered banks to review mainland-linked investment accounts with verification rules retroactive to January 2023. Taiwan’s TAIEX jumped 1.68% to 44,256.80 on Nvidia’s commitment to invest roughly $150 billion yearly in the island as the epicenter of AI supply chains.

USD/CNY eased 0.10% to 6.78 while the PBOC set the daily reference rate at 6.8240. Low pork prices at 16-year lows underscored anemic consumer spending and hog oversupply in mainland China. Copper’s 1.90% advance to 6.42 reflected optimism around Chinese industrial demand despite the absence of fresh data releases.

The Day Ahead

Markets will focus on the May 30 release of NBS Manufacturing PMI, last at 50.3, and Non-Manufacturing PMI, last at 49.4, both due at 17:30 ET. Any print below 50 would reinforce concerns over domestic demand weakness already visible in pork prices. Traders will also monitor PBoC liquidity operations and any State Council signals on growth support.

In Taiwan, semiconductor export volumes remain the key watch item given their direct link to growth forecasts. Hong Kong liquidity conditions stay anchored to the USD/HKD peg near 7.83.

Other Economic Notes

Industrial profits in mainland China show a pronounced K-shape, with gains concentrated in AI-related sectors while broader manufacturing lags. Global aluminum price strength risks drawing record Chinese exports, potentially adding to trade tensions. Miniso’s Q1 profit tripling to 1.25 billion yuan illustrates resilient consumer-facing niches amid overall spending softness.

The -0.10% China CPI YoY reading from April continues to highlight deflationary pressures that complicate policy calibration.

Global Macro News

The Fed’s Musalem noted that an easing bias no longer fits current U.S. conditions, supporting a firmer dollar outlook that could test yuan stability. Bank of Canada warnings on household stress and economy vulnerability to shocks add to global growth caution.

<i>↓ p.2</i>