Greater China Macro Daily(Beta Mode)

China PMI Steady Amid Digital Yuan Push

Market Snapshot

| Asset | Level | Change |

|---|---|---|

| Shanghai Composite | 4,068.57 | -0.73% |

| CSI 300 | 4,892.12 | -0.45% |

| Hang Seng | 25,182.39 | +0.70% |

| TAIEX | 44,732.94 | +2.51% |

| USD/CNY | 6.77 | -0.20% |

| USD/HKD | 7.84 | +0.04% |

| Copper | 6.39 | -0.11% |

| Brent Crude | 91.12 | -2.76% |

| Gold | 4,593.00 | +2.08% |

| Bitcoin | 73,806.40 | +0.07% |

| China 2Y Govt Yield | - | - |

| China 10Y Govt Yield | - | - |

Prior Economic Events

| Data | Prior | Cons | Actual |

|---|---|---|---|

| NBS Manufacturing PMI | 50.30 | 50 | 50 |

| NBS Non-Manufacturing PMI | 49.40 | 49.50 | 50.10 |

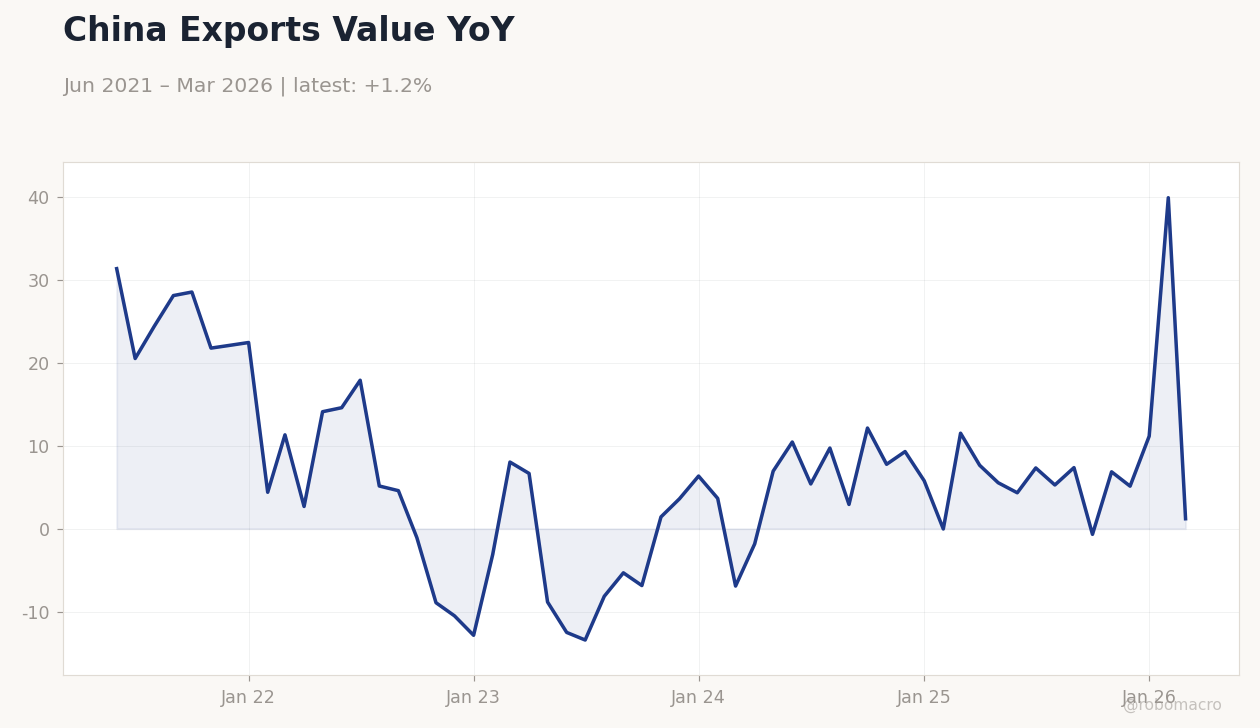

China Exports Value YoY | Type: macro_line | YoY %: 1.195 (2026-03-01) | Range: -13.41–39.86 | Trend(6pt): 31.32,5.14,-6.853,9.287,39.86,1.195

China Exports Value YoY | Type: macro_line | YoY %: 1.195 (2026-03-01) | Range: -13.41–39.86 | Trend(6pt): 31.32,5.14,-6.853,9.287,39.86,1.195

Today's Economic Events

| Data | Prior | Cons | Time |

|---|---|---|---|

| RatingDog Manufacturing PMI | 52.20 | 51.40 | 21:45 |

| RatingDog Services PMI | 52.60 | 52.30 | 21:45 |

| Monday (2026-06-01) | |||

| RatingDog Manufacturing PMI | 52.20 | 51.40 | 21:45 |

- NBS Manufacturing PMI printed at 50.0 in May, in line with consensus but below April’s 50.3, while Non-Manufacturing PMI rose to 50.1.

- PBoC expanded digital-yuan pilots to lottery payouts and fiscal transfers, lifting licensed banks to 22 and widening cross-border use cases.

- Equities diverged as Shanghai Composite fell 0.73 percent while TAIEX rose 2.51 percent; USD/CNY eased 0.20 percent to 6.77.

Yesterday's Recap

Mainland China’s official PMI data showed manufacturing activity flat at the 50 threshold, confirming the slowdown flagged by the five-day holiday disruption and softer external demand. Non-manufacturing activity improved modestly to 50.1, supported by services resilience. Equities diverged sharply: Shanghai Composite fell 0.73 percent and CSI 300 slipped 0.45 percent on growth concerns, while Hang Seng gained 0.70 percent and TAIEX surged 2.51 percent.

USD/CNY eased 0.20 percent to 6.77 as the PBoC maintained its daily fixing near recent levels. HKMA released April foreign-reserve and liquidity data, showing the aggregate balance stable and the USD/HKD peg holding at 7.84. Copper edged down 0.11 percent, consistent with muted China industrial readings.

The Day Ahead

Markets will focus on the RatingDog Manufacturing PMI release tonight, expected to print 51.4 after April’s 52.2 and provide a private-sector gauge of factory momentum. RatingDog Services PMI is also due, with consensus at 52.3. No PBoC or HKMA policy announcements are scheduled, though liquidity operations remain on watch.

Investors will monitor any State Council signals on property easing ahead of the weekend.

Other Economic Notes

China’s factory activity slowdown adds downside risk to Q2 GDP, with input-cost pressures from global energy prices compounding domestic demand weakness. Hong Kong’s position as the world’s largest cross-border wealth hub, per BCG, continues to draw inflows that support HKD liquidity and equity turnover. Property-sector deleveraging remains the dominant medium-term constraint on mainland credit demand.

Global Macro News

Brent crude fell 2.76 percent, easing imported inflation pressures for China while supporting real-income prospects. Gold rose 2.08 percent on safe-haven demand, benefiting PBoC reserve diversification. Global semiconductor demand continues to lift Taiwan and South Korea export prices, breaking China’s prior streak of falling export prices.

RBA and RBNZ signals of earlier or steeper hikes underscore divergent policy paths that could widen yield differentials versus Chinese bonds. Weak Canadian Q1 growth and rising unemployment elsewhere reinforce external demand risks for China’s manufacturing sector. <i>↓ p.2</i>