Greater China Macro Daily(Beta Mode)

China Exports Beat Forecasts as CPI Stalls

Market Snapshot

| Asset | Level | Change |

|---|---|---|

| Shanghai Composite | 3,993.23 | -0.42% |

| CSI 300 | 4,748.59 | -1.11% |

| Hang Seng | 24,565.90 | -0.37% |

| TAIEX | 44,704.44 | +2.76% |

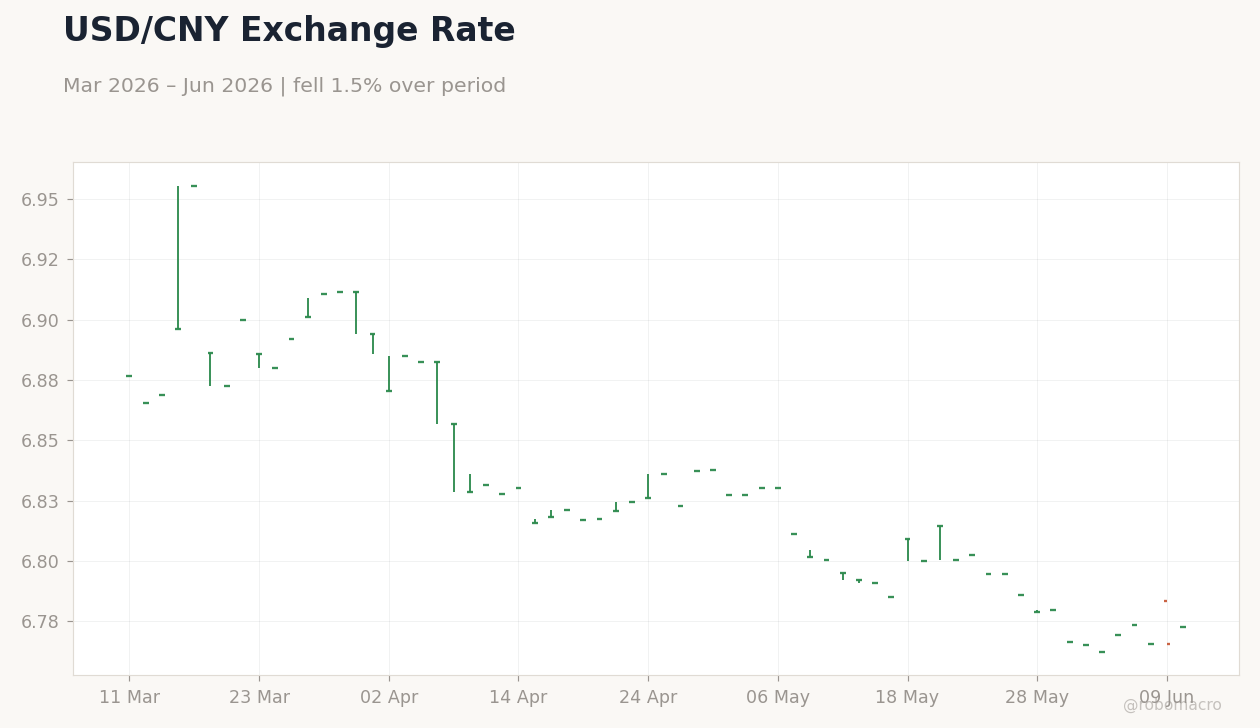

| USD/CNY | 6.77 | +0.10% |

| USD/HKD | 7.84 | -0.02% |

| Copper | 6.19 | -1.81% |

| Brent Crude | 95.58 | +4.52% |

| Gold | 4,081.30 | -4.19% |

| Bitcoin | 61,304.14 | -0.55% |

| China 2Y Govt Yield | - | - |

| China 10Y Govt Yield | - | - |

Prior Economic Events

| Data | Prior | Cons | Actual |

|---|---|---|---|

| Exports Year-over-Year | 14.10 | 15 | 19.40 |

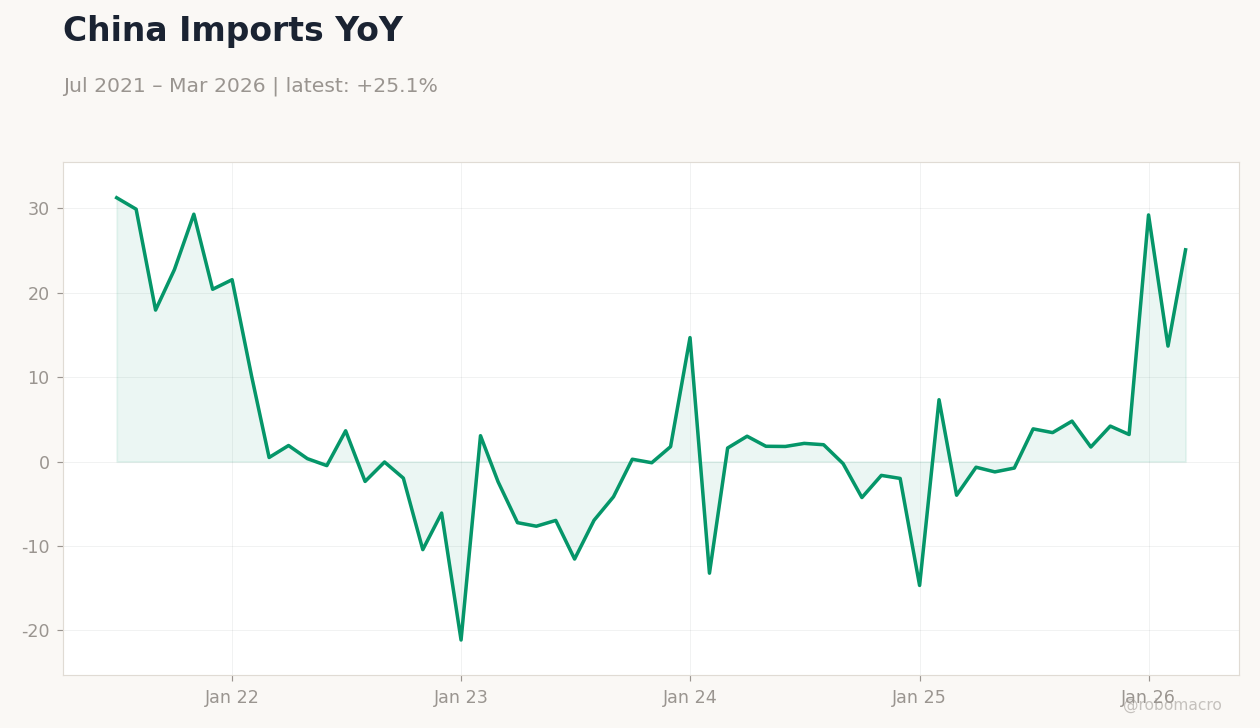

| Imports Year-over-Year | 25.30 | 25 | 27.40 |

| Trade Balance | 84,800m | 92,100m | 105,430m |

| Inflation Rate Year-over-Year | 1.20 | 1.30 | 1.20 |

| Inflation Rate Month-over-Month | 0.30 | -0.20 | -0.10 |

| Producer Price Index Year-over-Year | 2.80 | 3.90 | 3.90 |

China Exports YoY | Type: macro_line | YoY %: 1.195 (2026-03-01) | Range: -13.41–39.86 | Trend(5pt): 20.5,4.577,1.416,5.768,1.195

China Exports YoY | Type: macro_line | YoY %: 1.195 (2026-03-01) | Range: -13.41–39.86 | Trend(5pt): 20.5,4.577,1.416,5.768,1.195

Today's Economic Events

| Data | Prior | Cons | Time |

|---|---|---|---|

| No events available | |||

- China May exports jumped 19.4% YoY and imports rose 27.4% YoY, both exceeding forecasts and lifting the trade surplus to $105.4 billion.

- Mainland CPI held at -0.10% YoY while PPI accelerated to 3.9% YoY, signaling firm factory prices amid stable consumer demand.

- TAIEX rallied 2.76% on semiconductor strength; Shanghai Composite fell 0.42% and CSI 300 dropped 1.11%.

Yesterday's Recap

Mainland China trade data for May showed exports rising 19.4% YoY against a 15% consensus while imports climbed 27.4% YoY versus 25% expected, widening the surplus to $105.4 billion. CPI printed -0.10% YoY, matching the prior reading and below the 1.3% forecast, with the month-on-month rate at -0.1%. PPI accelerated to 3.9% YoY, confirming the fastest factory-price gain in nearly four years.

Equity markets diverged: Shanghai Composite closed at 3,993.23 (-0.42%) and CSI 300 at 4,748.59 (-1.11%), while TAIEX advanced 2.76% to 44,704.44 on AI-driven chip demand. USD/CNY edged up 0.10% to 6.77; USD/HKD held near 7.84 with minimal HKMA intervention. Copper fell 1.81% to 6.19 while Brent crude rose 4.52% to 95.58.

The Day Ahead

No major data releases are scheduled for mainland China, Hong Kong or Taiwan today. Markets will monitor PBoC liquidity operations and any State Council comments on local-government bond quotas. Hong Kong investors await further details on the planned Hong Kong dollar stablecoin launches by HSBC and Anchor Technology.

Taiwan will track TSMC sales trends and any updates on export-control rules for advanced packaging equipment. Cross-strait trade flows and rare-earth supply-chain developments may also influence sentiment.

Other Economic Notes

Strong AI hardware demand continues to underpin mainland export momentum and Taiwan semiconductor shipments. Property-sector stress persists as developers seek maturity extensions, though Beijing remains focused on targeted support rather than broad stimulus. Hong Kong’s aggregate balance stayed ample, supporting the USD/HKD peg without extraordinary measures.

Tokenisation pilots by the HKMA highlight ongoing efforts to modernise corporate treasury functions in the region.

Global Macro News

Global risk appetite stayed mixed as U.S.–China technology tensions and tariff debates weighed on sentiment. Brent crude’s sharp gain reflected supply concerns that could feed into mainland import costs. Gold’s 4.19% drop signaled reduced safe-haven demand, while copper’s decline pointed to softer near-term growth expectations for China.

OpenAI’s ban on China-linked accounts using ChatGPT for influence campaigns added friction to U.S.–China tech relations. <i>↓ p.2</i>