Greater China Macro Daily(Beta Mode)

China Trade Surplus Surges as CPI Stalls

Market Snapshot

| Asset | Level | Change |

|---|---|---|

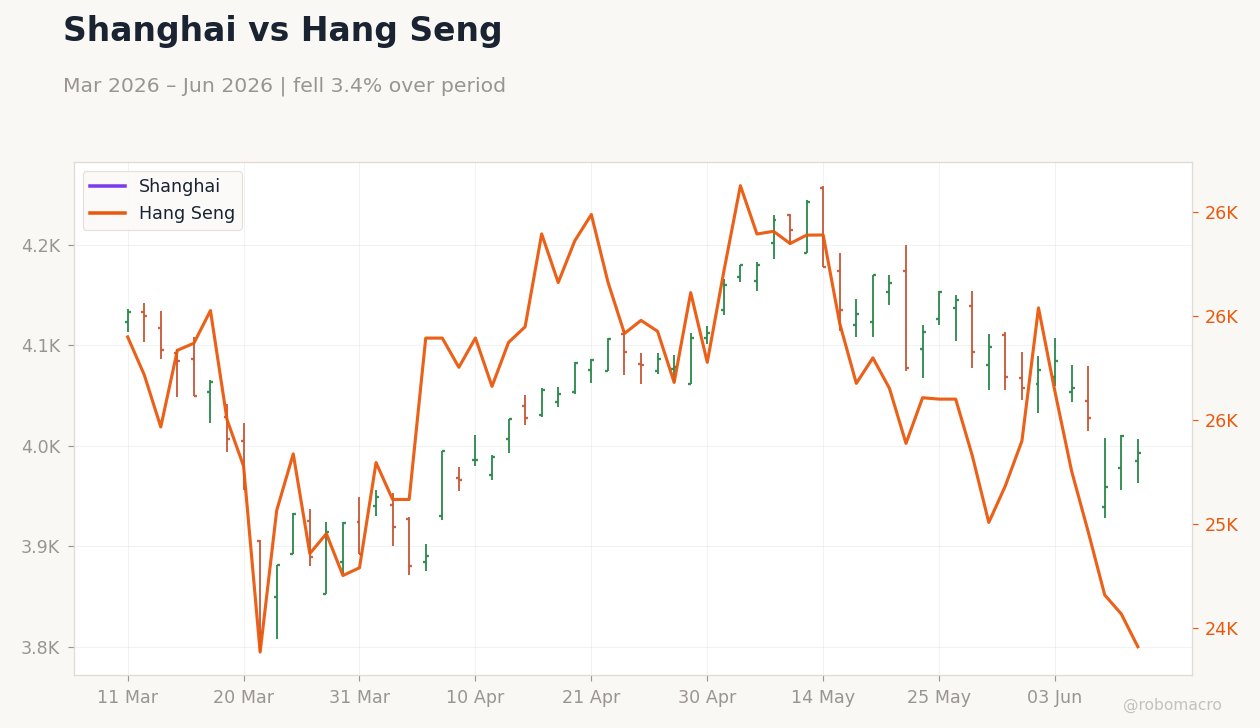

| Shanghai Composite | 3,987.01 | -0.16% |

| CSI 300 | 4,722.41 | -0.55% |

| Hang Seng | 24,407.96 | -0.64% |

| TAIEX | 43,225.54 | -3.31% |

| USD/CNY | 6.78 | +0.04% |

| USD/HKD | 7.84 | -0.02% |

| Copper | 6.39 | +2.28% |

| Brent Crude | 89.09 | -4.31% |

| Gold | 4,233.80 | +3.06% |

| Bitcoin | 63,507.93 | +3.35% |

| China 2Y Govt Yield | - | - |

| China 10Y Govt Yield | - | - |

Prior Economic Events

| Data | Prior | Cons | Actual |

|---|---|---|---|

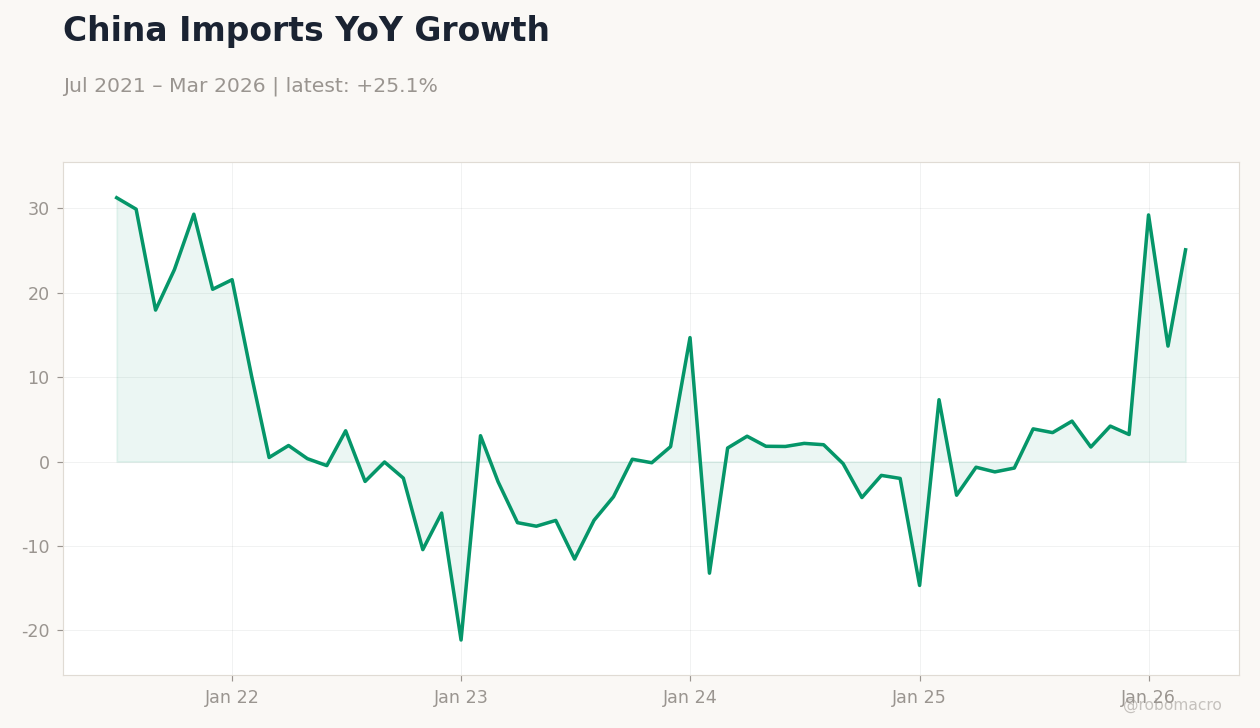

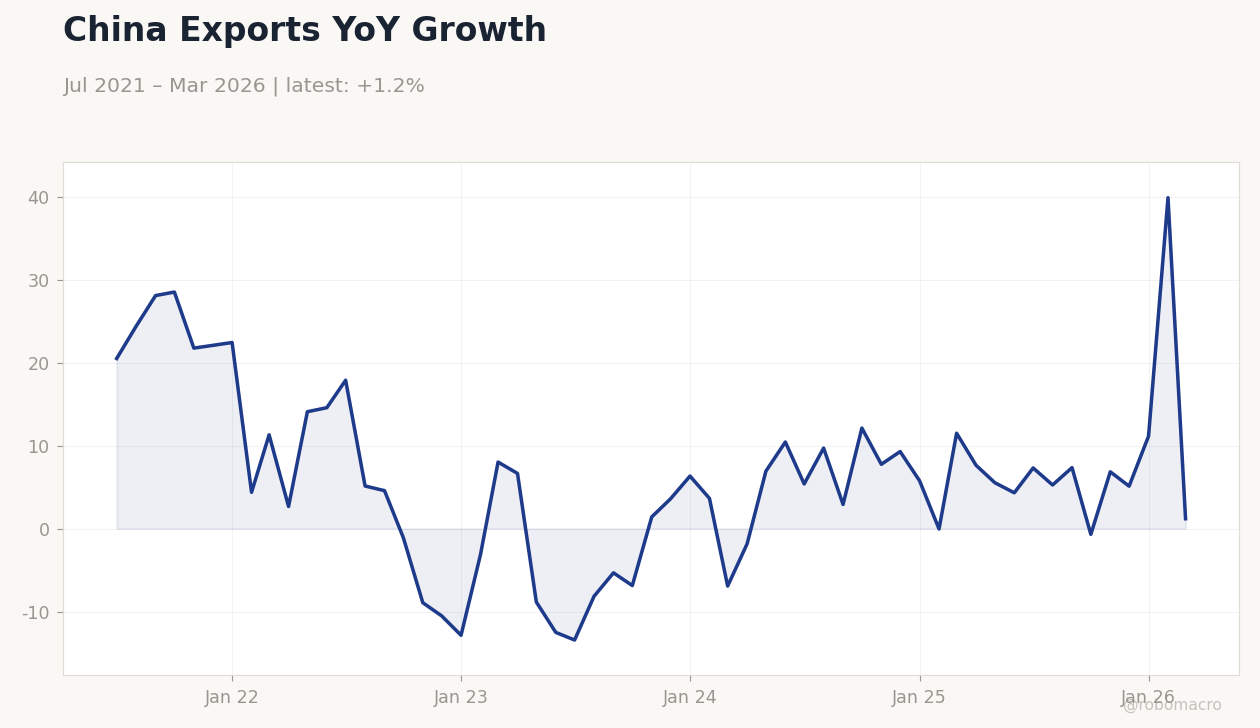

| Exports Year-over-Year | 14.10 | 15 | 19.40 |

| Imports Year-over-Year | 25.30 | 25 | 27.40 |

| Trade Balance | 84,800m | 92,100m | 105,430m |

| Inflation Rate Year-over-Year | 1.20 | 1.30 | 1.20 |

| Inflation Rate Month-over-Month | 0.30 | -0.20 | -0.10 |

| Producer Price Index Year-over-Year | 2.80 | 3.90 | 3.90 |

China Exports YoY Growth | Type: macro_line | Exports YoY %: 1.195 (2026-03-01) | Range: -13.41–39.86 | Trend(5pt): 20.5,4.577,1.416,5.768,1.195

China Exports YoY Growth | Type: macro_line | Exports YoY %: 1.195 (2026-03-01) | Range: -13.41–39.86 | Trend(5pt): 20.5,4.577,1.416,5.768,1.195

Today's Economic Events

| Data | Prior | Cons | Time |

|---|---|---|---|

| No events available | |||

- China exports jumped 19.4% YoY in May while imports rose 27.4% YoY, lifting the trade surplus to $105.4 billion.

- CPI held at 1.2% YoY but PPI accelerated to 3.9% YoY, widening the gap between consumer and factory prices.

- Equities fell across Greater China with TAIEX down 3.31% and CSI 300 off 0.55% amid Middle East tensions.

Yesterday's Recap

Mainland China released May trade figures showing exports rising 19.4% YoY against a 15% consensus and imports climbing 27.4% YoY, pushing the trade balance to $105.4 billion. CPI remained unchanged at 1.2% YoY while the monthly reading printed -0.1%, missing expectations. Producer prices accelerated to 3.9% YoY, the fastest pace in nearly four years.

Equity markets closed lower, led by a 3.31% drop in the TAIEX and a 0.64% decline in the Hang Seng. The Shanghai Composite eased 0.16% and the CSI 300 fell 0.55%. USD/CNY edged 0.04% higher to 6.78 while USD/HKD stayed near the peg at 7.84.

Copper rose 2.28% as a China demand proxy while Brent crude fell 4.31%.

The Day Ahead

The calendar is empty of major data releases for mainland China, Hong Kong and Taiwan. Markets will monitor follow-through from the PBOC-HKMA-Bank Indonesia MoU on direct yuan-rupiah settlement. Traders will also watch oil inventory draws after China began tapping commercial crude reserves.

Equity sentiment hinges on any escalation in Middle East tensions and their impact on Taiwan semiconductor supply chains. Hong Kong tokenisation initiatives and corporate treasury seminars may draw incremental attention.

Other Economic Notes

The divergence between flat consumer prices and surging factory prices highlights uneven cost pressures across the mainland economy. Strong trade data suggest resilient external demand despite global uncertainty, supporting near-term industrial output. Property sector weakness remains unaddressed by the latest releases and continues to weigh on domestic confidence.

Taiwan’s semiconductor exports face added volatility from geopolitical risks and rare-earth supply chain diversification efforts.

Global Macro News

China-linked accounts were banned from ChatGPT after using the tool to influence U.S. tariff and AI data-center debates. Beijing cancelled two high-level EU meetings as trade tensions between the blocs intensified.

<i>↓ p.2</i>