Greater China Macro Daily(Beta Mode)

Equities Surge as PBOC Curbs Interbank Lending

Market Snapshot

| Asset | Level | Change |

|---|---|---|

| Shanghai Composite | 4,031.51 | +1.12% |

| CSI 300 | 4,777.32 | +1.16% |

| Hang Seng | 24,718.10 | +1.93% |

| TAIEX | 44,169.04 | +2.36% |

| USD/CNY | 6.76 | -0.20% |

| USD/HKD | 7.83 | -0.01% |

| Copper | 6.45 | +2.97% |

| Brent Crude | 87.33 | -3.37% |

| Gold | 4,238.80 | +3.63% |

| Bitcoin | 65,329.99 | +1.41% |

| China 2Y Govt Yield | - | - |

| China 10Y Govt Yield | - | - |

Prior Economic Events

| Data | Prior | Cons | Actual |

|---|---|---|---|

| No events available | |||

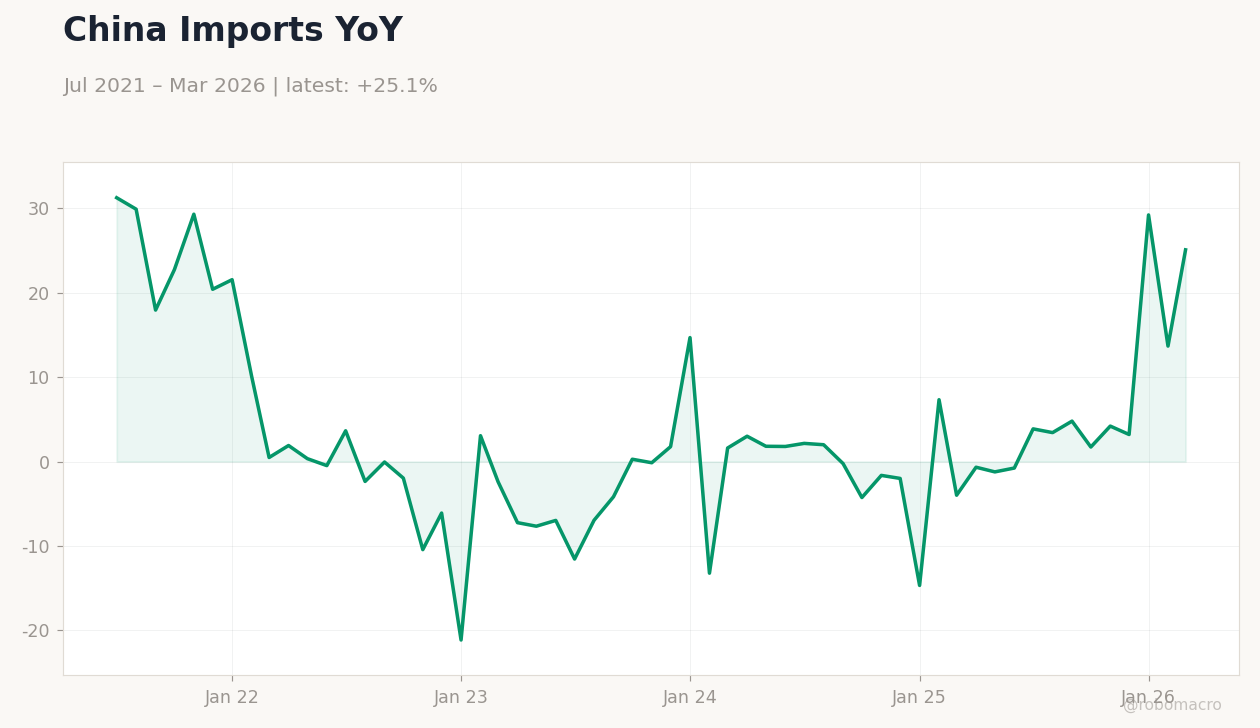

China Exports YoY | Type: macro_line | YoY %: 1.195 (2026-03-01) | Range: -13.41–39.86 | Trend(5pt): 20.5,4.577,1.416,5.768,1.195

China Exports YoY | Type: macro_line | YoY %: 1.195 (2026-03-01) | Range: -13.41–39.86 | Trend(5pt): 20.5,4.577,1.416,5.768,1.195

Today's Economic Events

| Data | Prior | Cons | Time |

|---|---|---|---|

| House Price Index Year-over-Year | -3.50 | - | 21:30 |

| Industrial Production Year-over-Year | 4.10 | 4.20 | 22:00 |

| Retail Sales Year-over-Year | 0.20 | 0 | 22:00 |

| Fixed Asset Investment (YTD) Year-over-Year | -1.60 | -2 | 22:00 |

- Mainland China equities rallied with Shanghai Composite up 1.12% and CSI 300 gaining 1.16% on PBoC liquidity signals.

- Hong Kong and Taiwan markets outperformed, with Hang Seng rising 1.93% and TAIEX climbing 2.36% amid semiconductor strength.

- PBoC signed yuan-rupiah MoU with Indonesia and Bank Indonesia while directing banks to reduce interbank lending to ease cash glut.

Yesterday's Recap

Mainland China markets advanced as the Shanghai Composite closed at 4,031.51 and CSI 300 reached 4,777.32. Hong Kong’s Hang Seng Index climbed to 24,718.10 while Taiwan’s TAIEX jumped to 44,169.04 on robust AI chip demand. USD/CNY eased 0.20% to 6.76 and USD/HKD held steady near 7.83.

No macro data releases occurred across Greater China on June 13. Copper rose 2.97% to 6.45 as a China growth proxy while Brent Crude fell 3.37%. PBoC instructed major banks to curb interbank lending to address excess liquidity.

HKMA reported a HK$26.8 billion rise in foreign assets within the Exchange Fund.

The Day Ahead

China will release May House Price Index at 21:30 ET followed by Industrial Production, Retail Sales and Fixed Asset Investment data at 22:00 ET. Markets will watch whether industrial output beats the 4.2% consensus and whether retail sales avoid contraction. Fixed asset investment is expected near -2.0% year-over-year.

No policy announcements are scheduled from PBoC, HKMA or CBC. Traders will monitor any follow-through from the PBoC-Bank Indonesia currency MoU.

Other Economic Notes

China’s consumer spending faces renewed pressure after earlier contraction signals, extending the slowdown in domestic demand. Property easing measures in tier-2 cities lifted sentiment but failed to reverse broader investment weakness. Taiwan maintained curbs on advanced AI chip exports to China, highlighting supply-chain tensions.

Cross-strait trade flows remained stable despite the licensing rules. HKMA aggregate balance stayed elevated above HK$500 billion, supporting peg stability.

Global Macro News

Iran conflict pushed global prices higher and dented growth forecasts, indirectly supporting China’s commodity imports. UK GDP contracted 0.1% in April, underscoring external demand risks for Chinese exporters. Bank of Japan signaled a potential rate hike to a 31-year high, which could strengthen yen and pressure regional currencies.

<i>↓ p.2</i>