Greater China Macro Daily(Beta Mode)

China Data Due Amid Equity Rally, Yuan MoU

Market Snapshot

| Asset | Level | Change |

|---|---|---|

| Shanghai Composite | 4,031.51 | +1.12% |

| CSI 300 | 4,777.32 | +1.16% |

| Hang Seng | 24,718.10 | +1.93% |

| TAIEX | 44,169.04 | +2.36% |

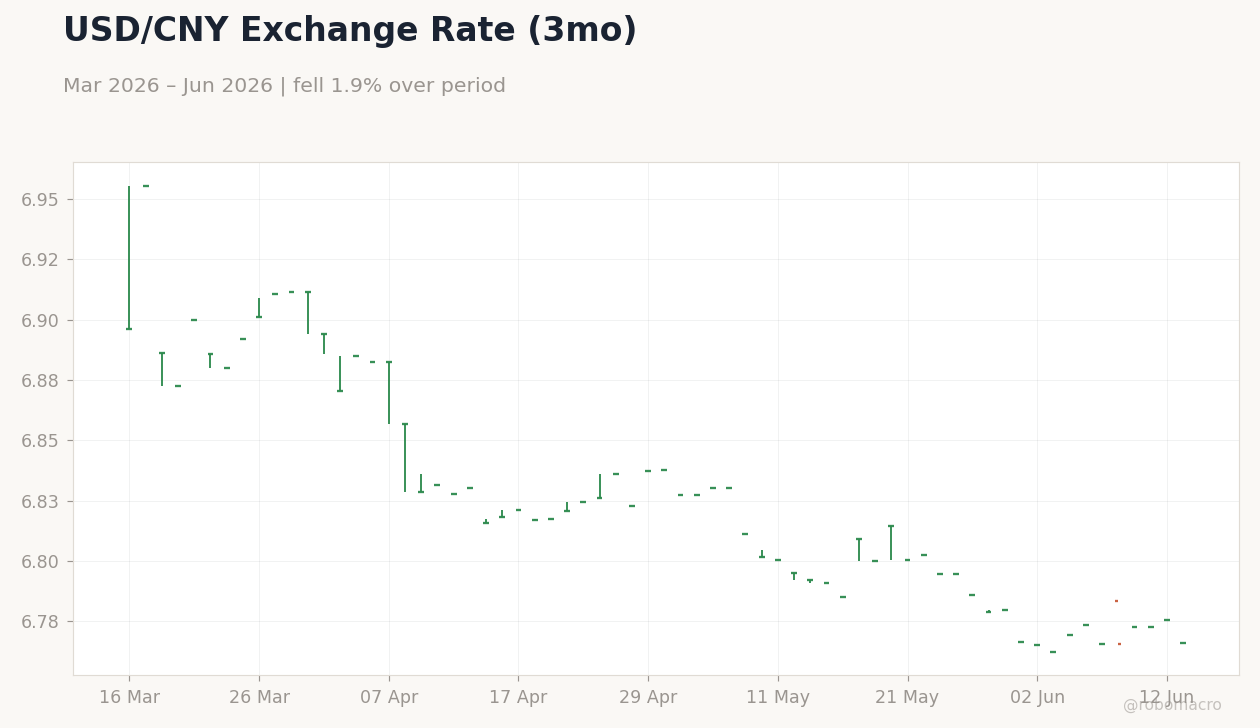

| USD/CNY | 6.77 | -0.14% |

| USD/HKD | 7.83 | -0.01% |

| Copper | 6.48 | +0.78% |

| Brent Crude | 83.64 | -4.23% |

| Gold | 4,332.10 | +2.78% |

| Bitcoin | 66,166.27 | +0.69% |

| China 2Y Govt Yield | - | - |

| China 10Y Govt Yield | - | - |

Prior Economic Events

| Data | Prior | Cons | Actual |

|---|---|---|---|

| No events available | |||

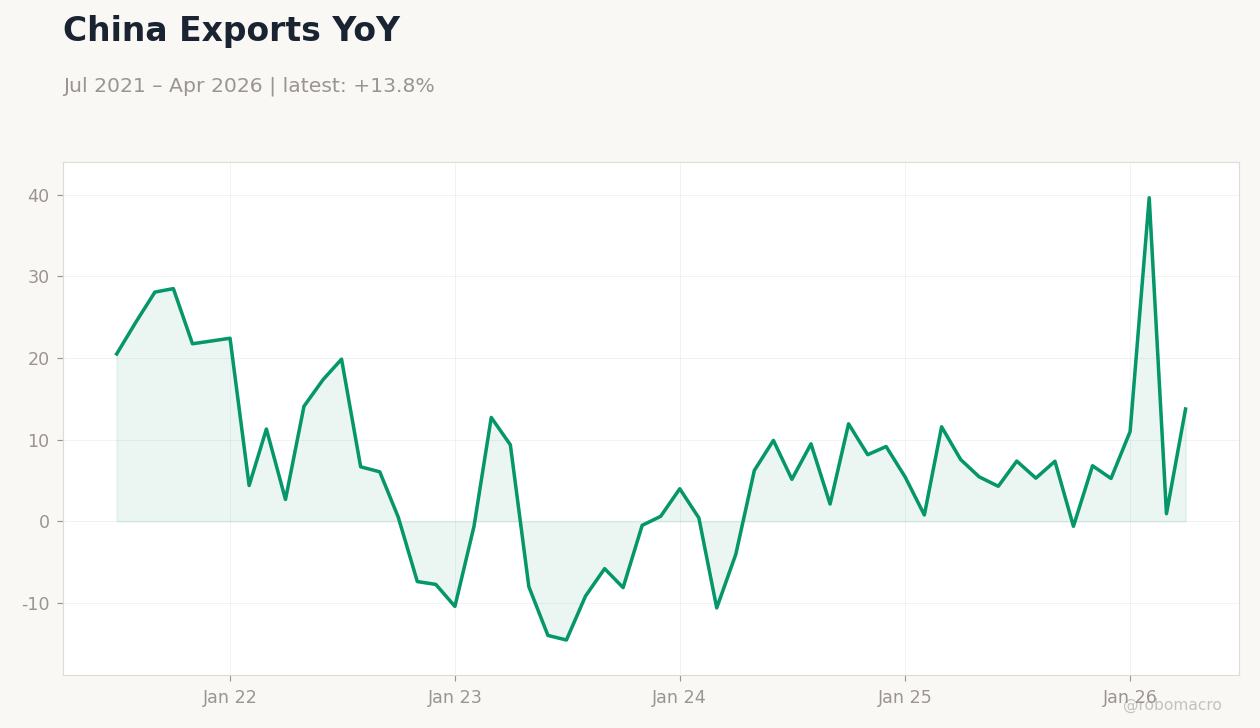

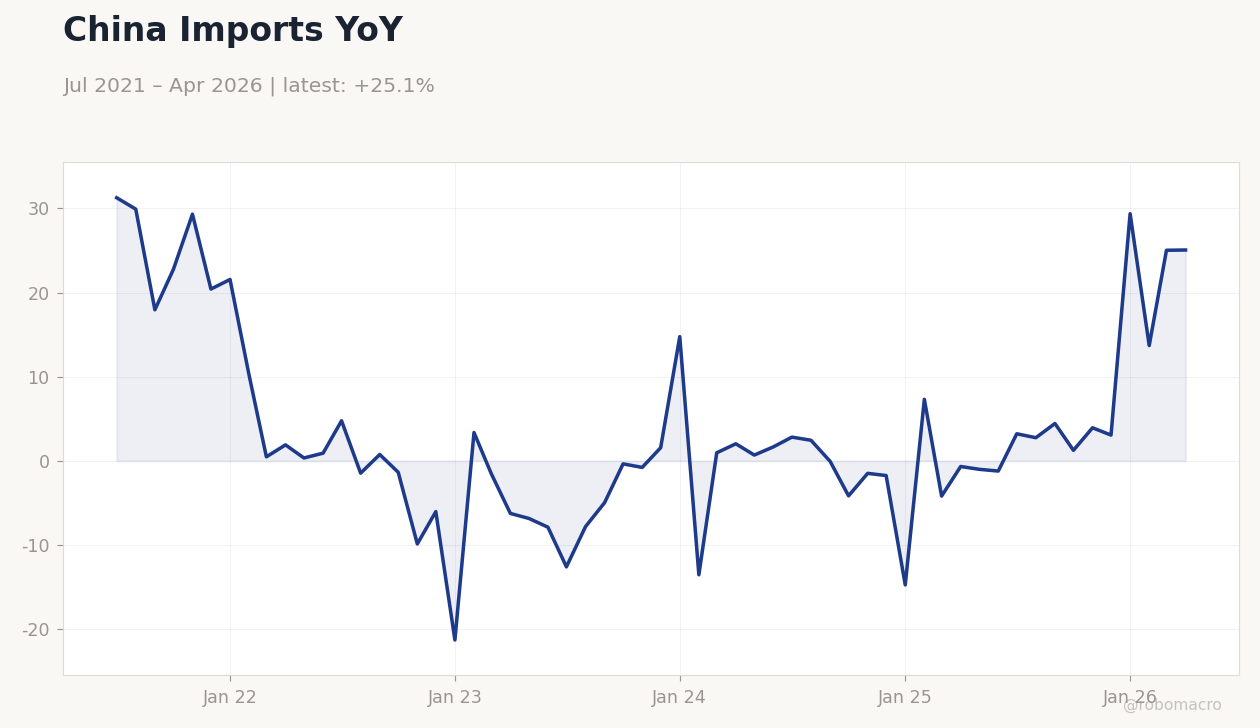

China Imports YoY | Type: macro_line | YoY %: 25.05 (2026-04-01) | Range: -21.28–31.26 | Trend(6pt): 31.26,0.7601,-0.7759,-14.73,25.02,25.05

China Imports YoY | Type: macro_line | YoY %: 25.05 (2026-04-01) | Range: -21.28–31.26 | Trend(6pt): 31.26,0.7601,-0.7759,-14.73,25.02,25.05

Today's Economic Events

| Data | Prior | Cons | Time |

|---|---|---|---|

| House Price Index Year-over-Year | -3.50 | - | 17:30 |

| Industrial Production Year-over-Year | 4.10 | 4.20 | 18:00 |

| Retail Sales Year-over-Year | 0.20 | 0 | 18:00 |

| Fixed Asset Investment (YTD) Year-over-Year | -1.60 | -2 | 18:00 |

- Equities across Greater China surged on improved risk sentiment, with TAIEX leading gains at +2.36%.

- PBOC, HKMA and Bank Indonesia signed direct yuan-rupiah MoU, reducing dollar reliance in bilateral trade.

- China May forex purchases reached 93 billion yuan as authorities managed elevated foreign currency demand.

Yesterday's Recap

Mainland China equities posted solid gains with Shanghai Composite rising 1.12% to 4,031.51 and CSI 300 advancing 1.16% to 4,777.32. Hong Kong’s Hang Seng climbed 1.93% to 24,718.10 while Taiwan’s TAIEX jumped 2.36% to 44,169.04, supported by semiconductor demand. USD/CNY fell 0.14% to 6.77, reflecting stronger yuan flows, and USD/HKD held steady near the peg at 7.83.

Copper rose 0.78% to 6.48 as a China growth proxy while Brent crude dropped 4.23%. PBOC and HKMA joined Bank Indonesia in signing an MoU to settle trade directly in yuan and rupiah, bypassing the dollar. China recorded a net forex purchase of 93 billion yuan in May amid sustained foreign currency demand.

No major data releases occurred on June 14.

The Day Ahead

China will release May House Price Index at 17:30 ET followed by Industrial Production, Retail Sales and Fixed Asset Investment at 18:00 ET. Markets expect Industrial Production to edge up to 4.2% y/y from 4.1% while Retail Sales are seen flat after April’s 0.2% print. Fixed Asset Investment is forecast to contract further to -2.0% y/y.

The data will shape expectations for near-term PBoC liquidity support. No policy meetings or Taiwan or Hong Kong releases are scheduled.

Other Economic Notes

Property-sector stress persists with developers facing liquidity shortfalls and local-government financing vehicle spreads widening. Beijing’s expanded “white list” of projects has yet to deliver measurable credit easing. Consumer spending shows signs of renewed weakness, extending the post-pandemic slowdown.

Cross-strait semiconductor flows remain central to Taiwan’s export outlook and CBC policy stance. New yuan loans rebounded in May to 520 billion yuan after an April drop, while total social financing also increased. China’s net forex purchases of 93 billion yuan in May highlight ongoing efforts to manage foreign-currency demand.

Broader economic indicators point to subdued momentum, with consumption remaining a key drag.