Greater China Macro Daily(Beta Mode)

China Retail Slump Offsets IP Beat

Market Snapshot

| Asset | Level | Change |

|---|---|---|

| Shanghai Composite | 4,091.89 | +1.50% |

| CSI 300 | 4,884.23 | +2.24% |

| Hang Seng | 24,842.67 | +0.50% |

| TAIEX | 45,396.99 | +2.78% |

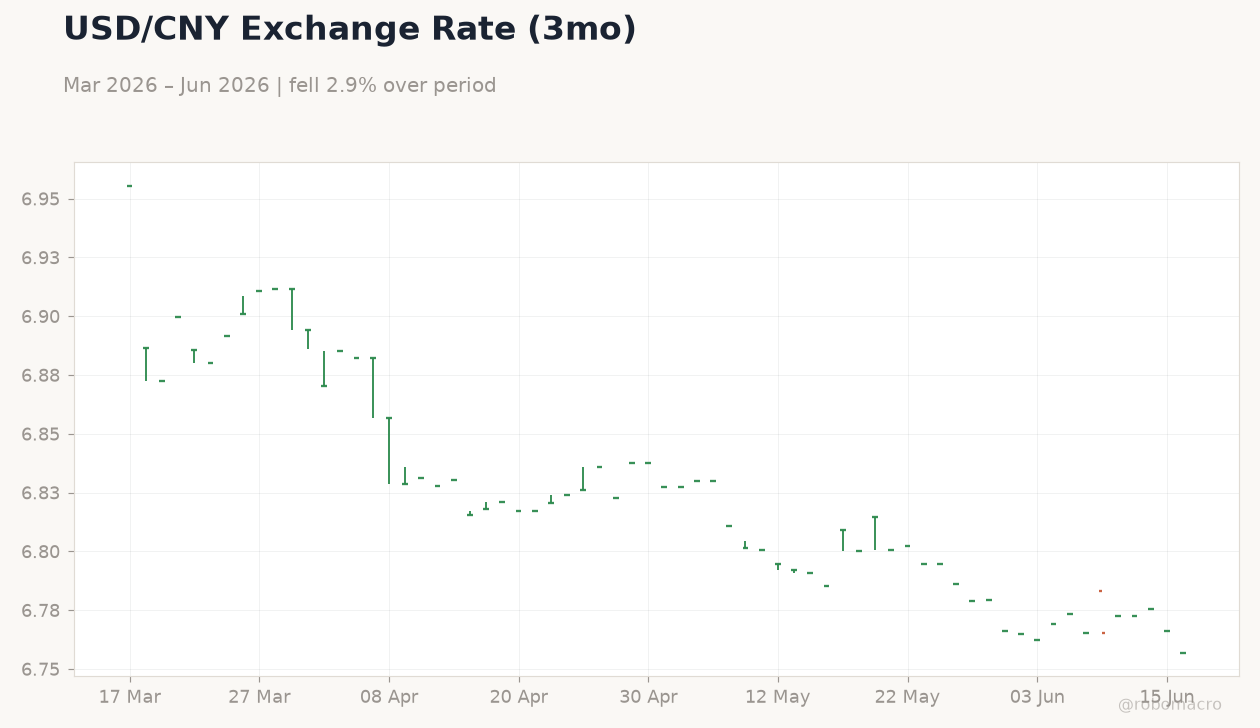

| USD/CNY | 6.76 | -0.13% |

| USD/HKD | 7.83 | -0.02% |

| Copper | 6.49 | +0.17% |

| Brent Crude | 79.49 | -4.42% |

| Gold | 4,353.20 | +0.58% |

| Bitcoin | 65,727.94 | -0.85% |

| China 2Y Govt Yield | - | - |

| China 10Y Govt Yield | - | - |

Prior Economic Events

| Data | Prior | Cons | Actual |

|---|---|---|---|

| House Price Index Year-over-Year | -3.50 | - | -3.50 |

| Industrial Production Year-over-Year | 4.10 | 4.30 | 4.50 |

| Retail Sales Year-over-Year | 0.20 | 0 | -0.60 |

| Fixed Asset Investment (YTD) Year-over-Year | -1.60 | -2 | -4.10 |

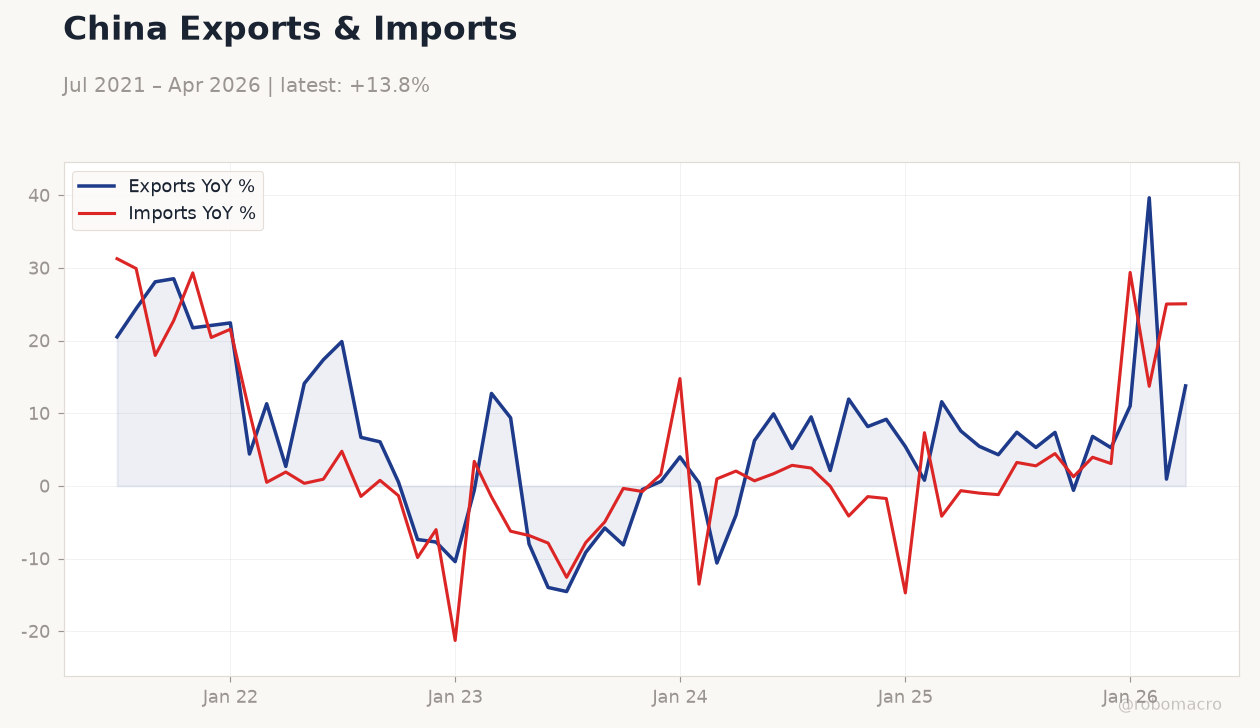

China Exports & Imports | Type: macro_line | Exports YoY %: 13.75 (2026-04-01) | Range: -14.55–39.64 | Trend(6pt): 20.5,6.06,-0.4972,5.406,0.9285,13.75 | Imports YoY %: 25.05 (2026-04-01) | Range: -21.28–31.26 | Trend(6pt): 31.26,0.7601,-0.7759,-14.73,25.02,25.05

China Exports & Imports | Type: macro_line | Exports YoY %: 13.75 (2026-04-01) | Range: -14.55–39.64 | Trend(6pt): 20.5,6.06,-0.4972,5.406,0.9285,13.75 | Imports YoY %: 25.05 (2026-04-01) | Range: -21.28–31.26 | Trend(6pt): 31.26,0.7601,-0.7759,-14.73,25.02,25.05

Today's Economic Events

| Data | Prior | Cons | Time |

|---|---|---|---|

| No events available | |||

- China retail sales contracted 0.6% YoY in May, missing consensus and marking the first decline since Covid

- Industrial production rose 4.5% YoY, beating expectations, while fixed-asset investment fell 4.1% YTD

- Equities rallied sharply with CSI 300 gaining 2.24% and TAIEX advancing 2.78%

Yesterday's Recap

China’s May data showed clear divergence between factory output and domestic demand. Industrial production exceeded forecasts at 4.5% YoY while retail sales printed at -0.6% YoY, confirming the slump reported across multiple outlets. Fixed-asset investment weakened further to -4.1% YTD and the house price index held at -3.5% YoY.

Mainland equities responded positively to the IP beat and property-support signals, lifting the Shanghai Composite 1.50% to 4,091.89 and CSI 300 2.24% to 4,884.23. Hong Kong’s Hang Seng rose 0.50% to 24,842.67 and Taiwan’s TAIEX jumped 2.78% to 45,396.99 on semiconductor resilience. USD/CNY eased 0.13% to 6.76 while USD/HKD stayed stable at 7.83 inside the peg band.

Copper gained 0.17% as a China demand proxy and Brent crude fell 4.42%.

The Day Ahead

No high-impact releases are scheduled for Greater China today or tomorrow. Markets will monitor PBoC liquidity operations and any State Council comments on property easing. Taiwan’s next market-moving print is semiconductor export data due later this week.

HKMA aggregate balance and USD/HKD peg dynamics remain in focus amid ongoing tokenization initiatives. Cross-strait trade flows and G7 discussions on Chinese exports may also influence sentiment.

Other Economic Notes

China’s economy is showing widening divergence between resilient exports and weakening domestic demand. Retail sales and investment have slumped to levels last seen during the pandemic, increasing reliance on external demand. Property-sector support measures in tier-1 cities have lifted transaction volumes modestly but have yet to reverse the broader investment decline.

Digital-yuan integration with 26 financial institutions is expanding cross-border payment channels. Household deleveraging continues to weigh on credit demand according to the latest bank lending figures.

Global Macro News

Surging Chinese exports are raising concerns at the G7 summit about renewed pressure on European manufacturers. The stronger yuan narrative gained traction after reports that USD/CNY could test 6.5 by year-end if the dollar stays range-bound. <i>↓ p.2</i>