Greater China Macro Daily(Beta Mode)

China Retail Slump Offsets IP Beat, Yuan Push Accelerates

Market Snapshot

| Asset | Level | Change |

|---|---|---|

| Shanghai Composite | 4,108.08 | +0.40% |

| CSI 300 | 4,931.39 | +0.97% |

| Hang Seng | 24,493.95 | -1.40% |

| TAIEX | 45,809.19 | +0.91% |

| USD/CNY | 6.76 | +0.00% |

| USD/HKD | 7.84 | +0.01% |

| Copper | 6.36 | -1.94% |

| Brent Crude | 78.69 | -0.34% |

| Gold | 4,276.30 | -1.26% |

| Bitcoin | 64,128.47 | -2.24% |

| China 2Y Govt Yield | - | - |

| China 10Y Govt Yield | - | - |

Prior Economic Events

| Data | Prior | Cons | Actual |

|---|---|---|---|

| House Price Index Year-over-Year | -3.50 | - | -3.50 |

| Industrial Production Year-over-Year | 4.10 | 4.30 | 4.50 |

| Retail Sales Year-over-Year | 0.20 | 0 | -0.60 |

| Fixed Asset Investment (YTD) Year-over-Year | -1.60 | -2 | -4.10 |

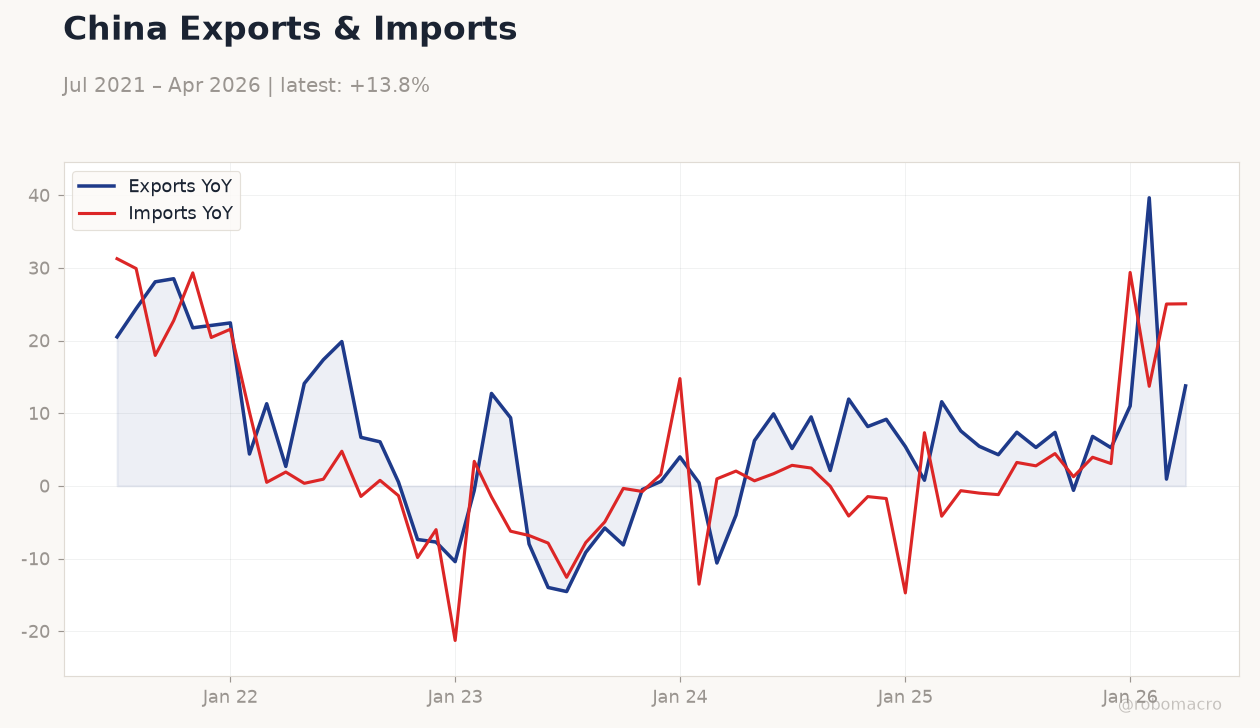

China Exports & Imports | Type: macro_line | Exports YoY: 13.75 (2026-04-01) | Range: -14.55–39.64 | Trend(6pt): 20.5,6.06,-0.4972,5.406,0.9285,13.75 | Imports YoY: 25.05 (2026-04-01) | Range: -21.28–31.26 | Trend(6pt): 31.26,0.7601,-0.7759,-14.73,25.02,25.05

China Exports & Imports | Type: macro_line | Exports YoY: 13.75 (2026-04-01) | Range: -14.55–39.64 | Trend(6pt): 20.5,6.06,-0.4972,5.406,0.9285,13.75 | Imports YoY: 25.05 (2026-04-01) | Range: -21.28–31.26 | Trend(6pt): 31.26,0.7601,-0.7759,-14.73,25.02,25.05

Today's Economic Events

| Data | Prior | Cons | Time |

|---|---|---|---|

| No events available | |||

- China May retail sales fell 0.6% y/y while industrial production beat at 4.5% y/y, deepening growth divergence.

- Shanghai Composite rose 0.40% and CSI 300 gained 0.97% as PBoC signaled further yuan internationalization steps.

- HKMA announced June 24 bond tenders and advanced tokenization initiatives while Hang Seng fell 1.40%.

Yesterday's Recap

Mainland China data released on June 16 showed industrial production rising 4.5% y/y, above the 4.3% consensus, while retail sales contracted 0.6% y/y against a flat consensus. Fixed-asset investment (YTD) slumped to -4.1% y/y and house prices held at -3.5% y/y. Equities diverged with Shanghai Composite and CSI 300 advancing while the Hang Seng declined 1.40% and TAIEX rose 0.91%.

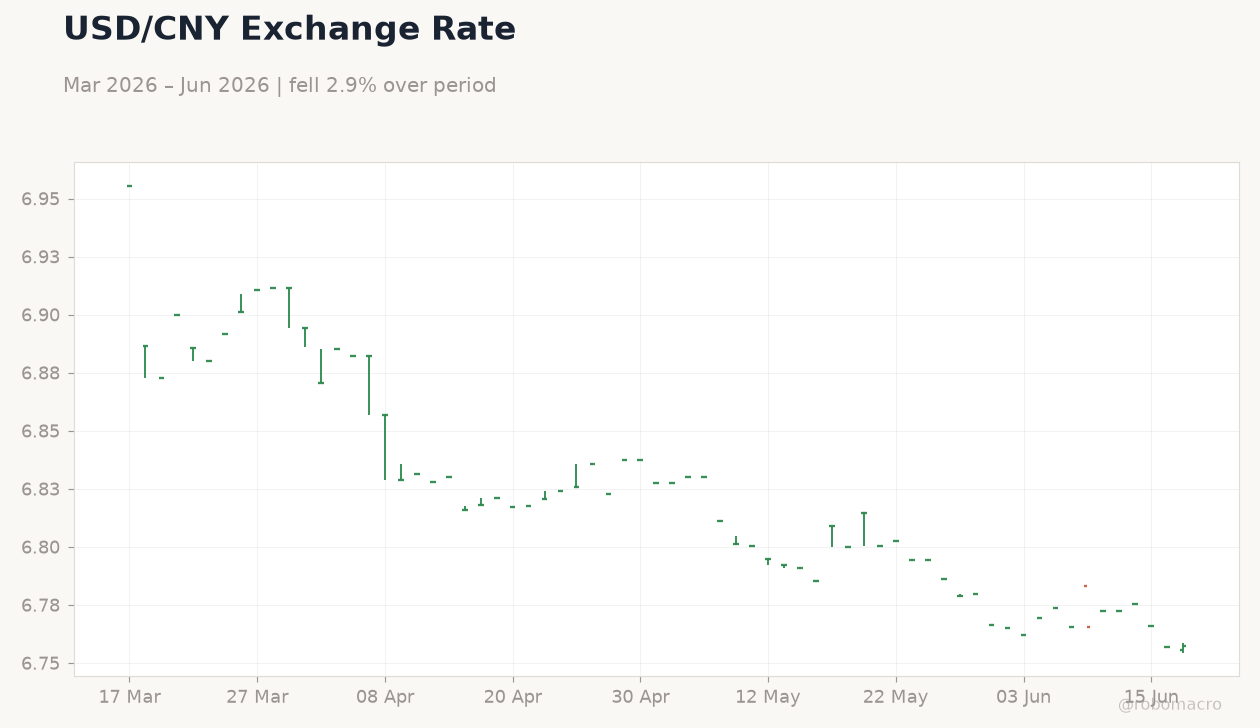

USD/CNY stayed at 6.76 and USD/HKD at 7.84 inside the peg band. Copper fell 1.94% on softer China demand signals. PBoC Governor announcements at the Lujiazui Forum emphasized new measures to expand yuan use in cross-border payments and integrate 26 institutions into the digital yuan platform.

The Day Ahead

No major data releases are scheduled for Greater China on June 17. Attention centers on ongoing Lujiazui Forum speeches by PBoC and financial regulators expected to outline further yuan internationalization steps. HKMA will proceed with preparations for the June 24 tender of HK$1.75 billion 5-year and HK$1.25 billion 10-year government bonds.

Market participants will monitor any PBoC liquidity operations or State Council signals on property support. Taiwan export and semiconductor supply-chain updates remain on watch for June.

Other Economic Notes

China’s retail sales contraction marks the first decline since Covid and widens the gap between external demand strength and domestic weakness. Exports continue to surge, raising EU concerns over subsidized shipments ahead of the G7 summit and prompting fresh trade-deficit scrutiny in Brussels. Property sector data remain soft with house prices unchanged at -3.5% y/y, keeping pressure on local-government financing and urban redevelopment quotas.

Broader stimulus remains measured, with the latest special-bond tranche smaller than prior rounds.

Global Macro News

Surging Chinese exports are flagged as “China Shock 2.0” at the G7, with Europe weighing new protective measures on EVs and other goods. Eurozone growth resilience contrasts with China’s domestic softness, supporting a firmer euro versus yuan. Brent crude eased 0.34% and gold declined 1.26% amid mixed risk sentiment.

<i>↓ p.2</i>