Greater China Macro Daily(Beta Mode)

China IP Beats but Retail Sales Slump

Market Snapshot

| Asset | Level | Change |

|---|---|---|

| Shanghai Composite | 4,090.48 | -0.43% |

| CSI 300 | 4,941.60 | +0.21% |

| Hang Seng | 24,312.16 | -0.74% |

| TAIEX | 45,877.39 | +0.15% |

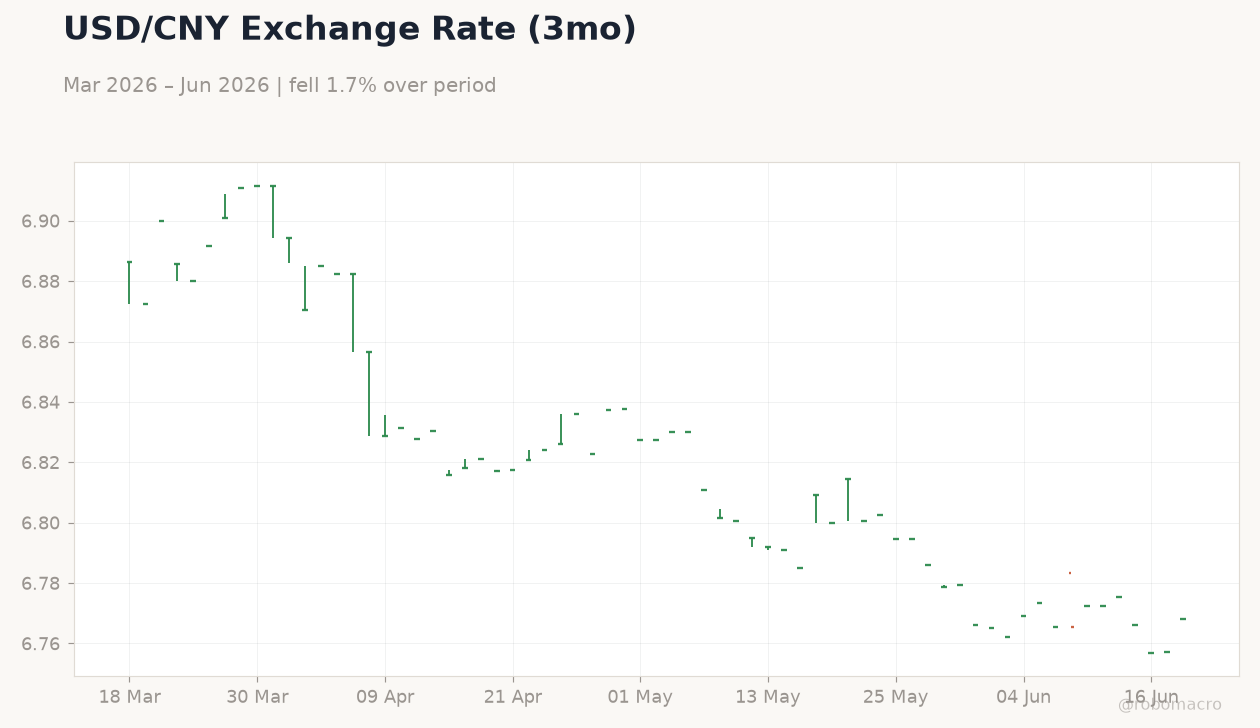

| USD/CNY | 6.77 | +0.16% |

| USD/HKD | 7.84 | +0.05% |

| Copper | 6.38 | -1.59% |

| Brent Crude | 79.44 | -0.14% |

| Gold | 4,227.90 | -3.01% |

| Bitcoin | 62,908.96 | -4.10% |

| China 2Y Govt Yield | - | - |

| China 10Y Govt Yield | - | - |

Prior Economic Events

| Data | Prior | Cons | Actual |

|---|---|---|---|

| House Price Index Year-over-Year | -3.50 | - | -3.50 |

| Industrial Production Year-over-Year | 4.10 | 4.30 | 4.50 |

| Retail Sales Year-over-Year | 0.20 | 0 | -0.60 |

| Fixed Asset Investment (YTD) Year-over-Year | -1.60 | -2 | -4.10 |

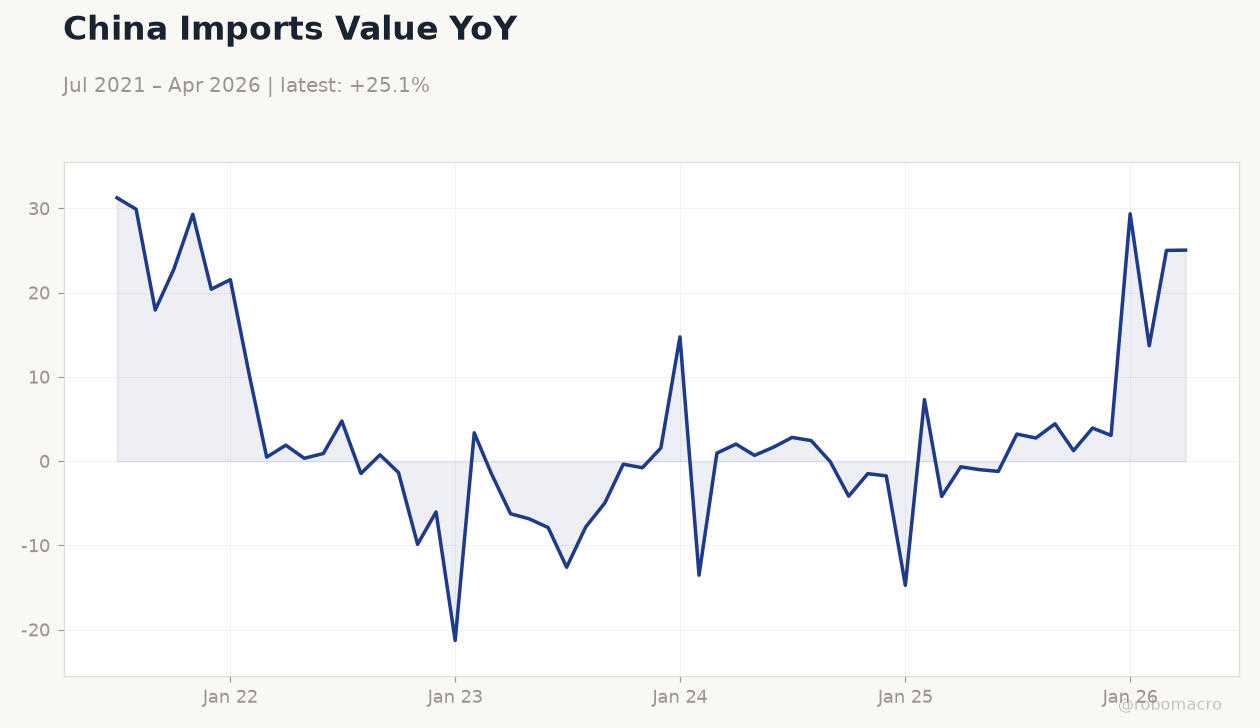

China Imports Value YoY | Type: macro_line | % YoY: 25.05 (2026-04-01) | Range: -21.28–31.26 | Trend(6pt): 31.26,0.7601,-0.7759,-14.73,25.02,25.05

China Imports Value YoY | Type: macro_line | % YoY: 25.05 (2026-04-01) | Range: -21.28–31.26 | Trend(6pt): 31.26,0.7601,-0.7759,-14.73,25.02,25.05

Today's Economic Events

| Data | Prior | Cons | Time |

|---|---|---|---|

| No events available | |||

- Mainland China May industrial production rose 4.5% y/y, beating consensus, while retail sales fell 0.6% and fixed-asset investment contracted 4.1% ytd.

- PBoC signals fresh steps to internationalize the yuan via Africa tariff cuts as trade nears $400 billion; HKMA and CBC both hold policy rates steady.

- Shanghai Composite fell 0.43% to 4,090.48 while CSI 300 gained 0.21%; USD/CNY rose 0.16% to 6.77 amid mixed equity moves.

Yesterday's Recap

Mainland China May data showed industrial production at 4.5% y/y versus 4.3% expected, confirming a modest manufacturing rebound, while retail sales contracted 0.6% against a flat consensus and fixed-asset investment plunged to -4.1% ytd. House prices held at -3.5% y/y. Shanghai Composite closed at 4,090.48 (-0.43%) and Hang Seng fell 0.74% to 24,312.16, but CSI 300 edged up 0.21% to 4,941.60 on property support hopes.

TAIEX rose 0.15% to 45,877.39. USD/CNY climbed 0.16% to 6.77 and USD/HKD ticked 0.05% higher to 7.84. Copper dropped 1.59% to 6.38 while Brent eased 0.14% to 79.44.

PBoC governor highlighted new yuan internationalization measures at the Lujiazui Forum.

The Day Ahead

No major data releases are scheduled for mainland China, Hong Kong or Taiwan today. Markets will focus on ongoing Lujiazui Forum speeches from PBoC and financial regulators for fresh policy signals. HKMA aggregate balance and peg stability remain in focus after the base-rate hold.

Taiwan semiconductor supply-chain updates may surface ahead of next week’s export figures. Investors will also monitor any State Council comments on targeted credit support for developers.

Other Economic Notes

Property-sector weakness persisted as fixed-asset investment contracted sharply, keeping pressure on local-government financing vehicles. China’s tariff removals on African imports are accelerating yuan settlement in bilateral trade, supporting de-dollarization efforts. Hong Kong credit-card usage surged in Q1, reflecting resilient consumer spending despite the record-low birth rate.

Cross-strait trade flows remain stable but face monitoring amid geopolitical tensions.

Global Macro News

The Federal Reserve left rates unchanged, aligning with HKMA and CBC decisions and limiting immediate pressure on Asian currencies. Fed patience on further hikes supports a narrow trading range for USD/CNY near 6.77. <i>↓ p.2</i>