Greater China Macro Daily(Beta Mode)

LPR Hold Looms as China Demand Weakens

Market Snapshot

| Asset | Level | Change |

|---|---|---|

| Shanghai Composite | 4,090.48 | -0.43% |

| CSI 300 | 4,941.60 | +0.21% |

| Hang Seng | 23,924.81 | -1.59% |

| TAIEX | 46,465.20 | +1.28% |

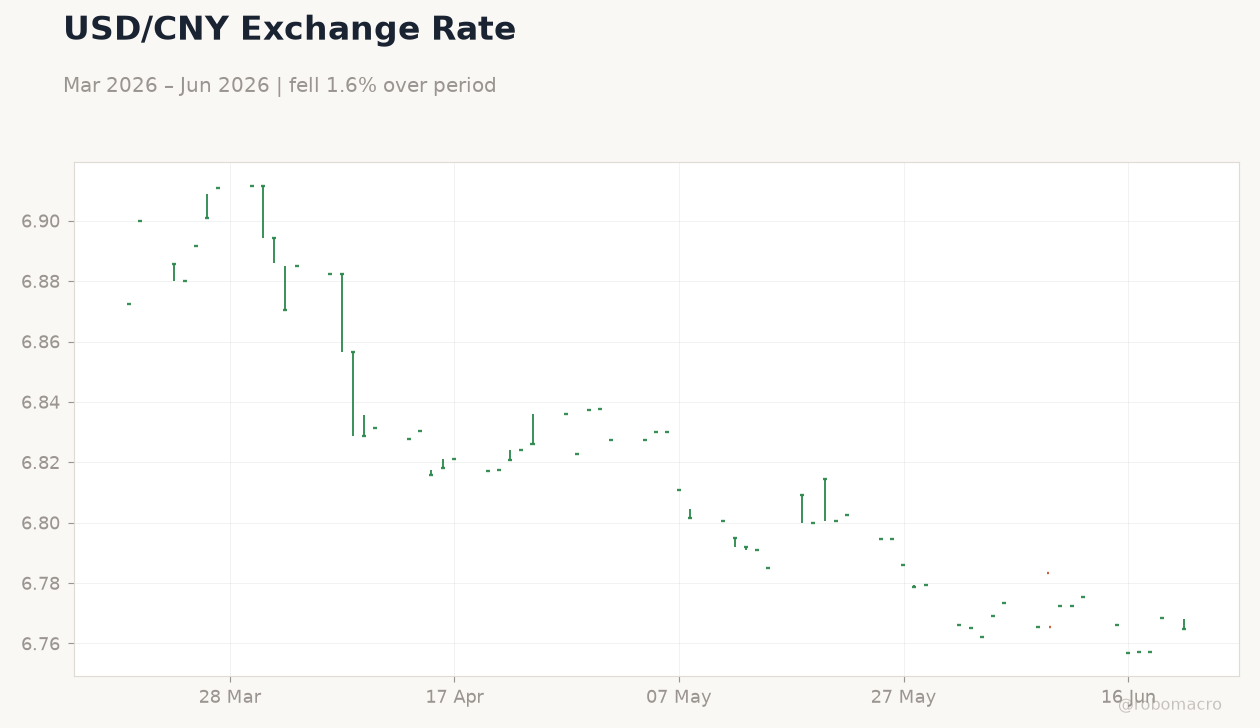

| USD/CNY | 6.76 | -0.06% |

| USD/HKD | 7.84 | -0.00% |

| Copper | 6.34 | -0.59% |

| Brent Crude | 80.59 | +0.93% |

| Gold | 4,172.90 | -1.21% |

| Bitcoin | 63,584.71 | -1.02% |

| China 2Y Govt Yield | - | - |

| China 10Y Govt Yield | - | - |

Prior Economic Events

| Data | Prior | Cons | Actual |

|---|---|---|---|

| No events available | |||

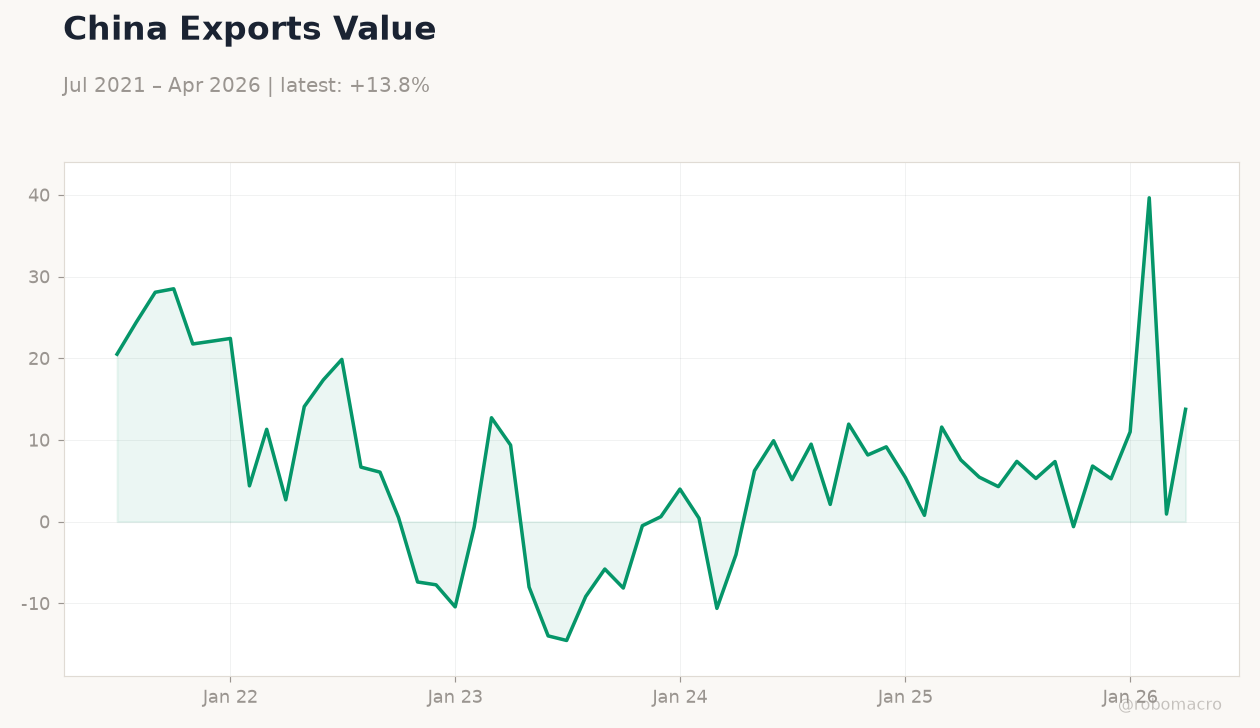

China Imports Value | Type: macro_line | USD bn: 25.05 (2026-04-01) | Range: -21.28–31.26 | Trend(6pt): 31.26,0.7601,-0.7759,-14.73,25.02,25.05

China Imports Value | Type: macro_line | USD bn: 25.05 (2026-04-01) | Range: -21.28–31.26 | Trend(6pt): 31.26,0.7601,-0.7759,-14.73,25.02,25.05

Today's Economic Events

| Data | Prior | Cons | Time |

|---|---|---|---|

| Loan Prime Rate 1Y | 3 | 3 | 21:15 |

| Loan Prime Rate 5Y | 3.50 | 3.50 | 21:15 |

| Monday (2026-06-22) | |||

| Loan Prime Rate 1Y | 3 | 3 | 21:15 |

| Loan Prime Rate 5Y | 3.50 | 3.50 | 21:15 |

- China’s Loan Prime Rates expected to hold at 3.00% (1Y) and 3.50% (5Y) with no change signaled by PBoC liquidity data.

- Mainland equities mixed while Hong Kong fell 1.59% and Taiwan rose 1.28% on semiconductor order strength.

- Yuan steady at 6.76 against USD as Beijing trims US Treasury holdings to 18-year low amid export surge concerns.

Yesterday's Recap

Mainland China markets showed modest divergence with Shanghai Composite falling 0.43% to 4,090.48 while CSI 300 edged up 0.21% to 4,941.60. Property and bank shares provided support after reports of expanded white-list financing. Hong Kong’s Hang Seng dropped 1.59% to 23,924.81 as investors remained cautious ahead of the LPR announcement.

Taiwan’s TAIEX gained 1.28% to 46,465.20, lifted by continued AI-driven semiconductor demand. USD/CNY eased 0.06% to 6.76 while USD/HKD stayed pinned at 7.84. Copper declined 0.59% to 6.34 on softer China growth signals, while Brent crude rose 0.93% to 80.59.

No major data releases occurred on 20 June across Greater China.

The Day Ahead

Markets focus on the 21:15 LPR fixing where both the 1-year and 5-year rates are expected to remain unchanged at 3.00% and 3.50%. Analysts watch for any accompanying PBoC statement on liquidity operations or targeted RRR relief. Hong Kong reports no major releases but follows HKMA aggregate balance updates.

Taiwan tracks any comments from the CBC on export orders. Cross-strait trade tensions may surface with ongoing atemoya purchase discussions between Beijing and Taipei.

Other Economic Notes

Activity remains soft midway through 2026 despite Beijing’s repeated calls to boost domestic demand. Property transaction volumes in tier-1 cities rose 12% m/m in early June after the white list expanded to 6,800 projects. Export momentum continues to draw international scrutiny as surging shipments raise G7 concerns over Europe’s industrial base.

China’s CPI printed -0.10% YoY in the latest reading, underscoring persistent price weakness.

Global Macro News

The Fed’s hawkish tilt has tightened global financial conditions and weighed on emerging-market sentiment. China’s demand slowdown is cited as a key drag on global commodity prices and growth forecasts. Beijing trimmed US Treasury holdings to an 18-year low, reflecting both reserve management and geopolitical caution.

<i>↓ p.2</i>