Greater China Macro Daily(Beta Mode)

Hang Seng Slides as PBoC Holds Steady

Market Snapshot

| Asset | Level | Change |

|---|---|---|

| Shanghai Composite | 4,090.48 | -0.43% |

| CSI 300 | 4,941.60 | +0.21% |

| Hang Seng | 23,924.81 | -1.59% |

| TAIEX | 46,465.20 | +1.28% |

| USD/CNY | 6.77 | +0.00% |

| USD/HKD | 7.84 | +0.04% |

| Copper | 6.35 | -0.34% |

| Brent Crude | 78.25 | -2.00% |

| Gold | 4,206.60 | -0.41% |

| Bitcoin | 63,852.16 | +0.97% |

| China 2Y Govt Yield | - | - |

| China 10Y Govt Yield | - | - |

Prior Economic Events

| Data | Prior | Cons | Actual |

|---|---|---|---|

| No events available | |||

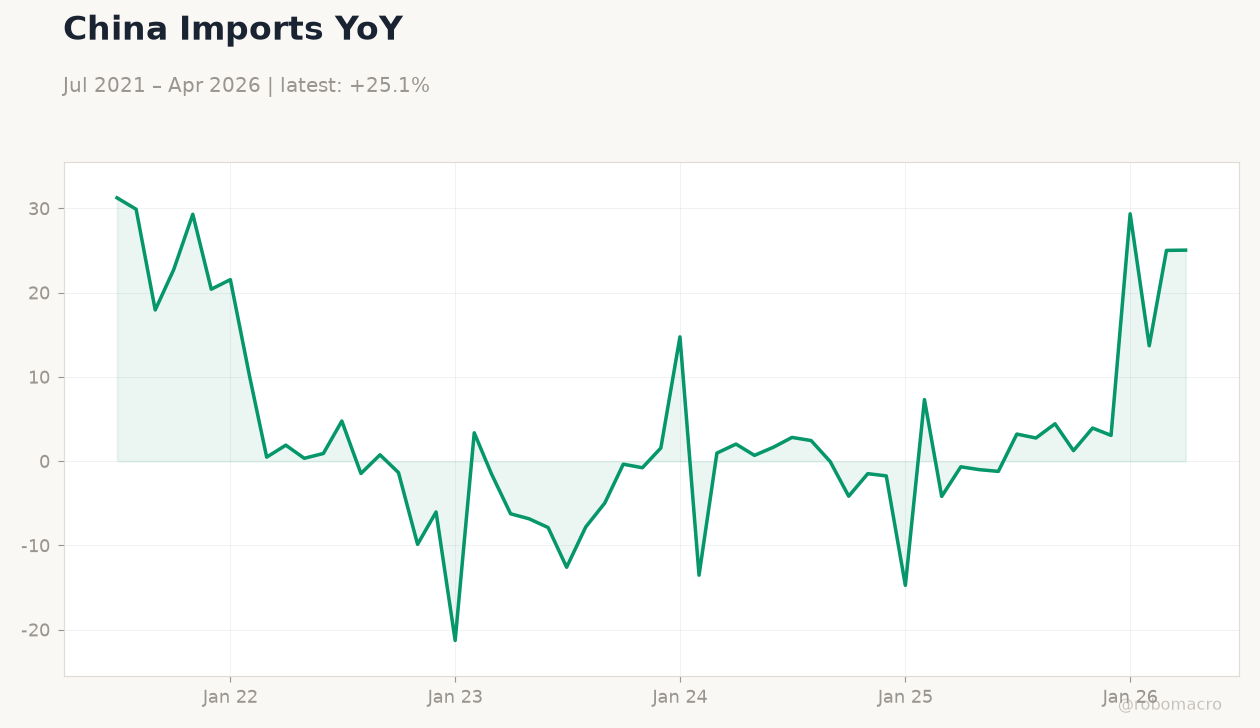

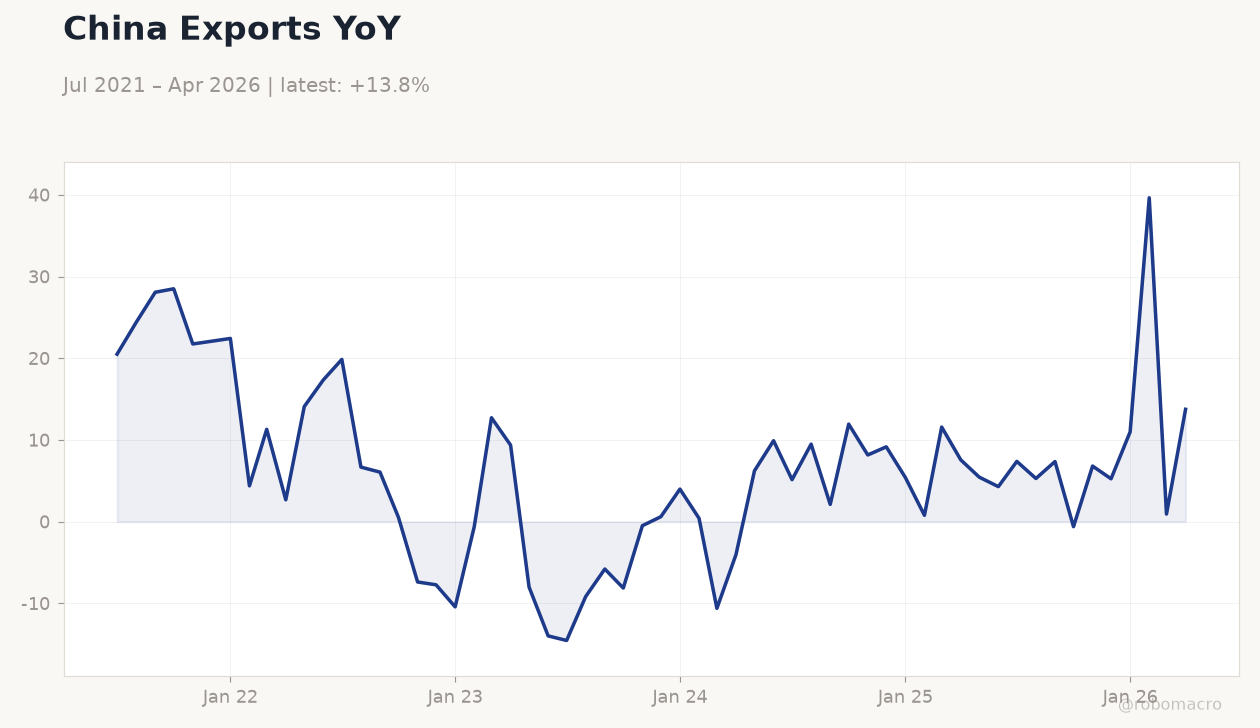

China Exports YoY | Type: macro_line | YoY %: 13.75 (2026-04-01) | Range: -14.55–39.64 | Trend(6pt): 20.5,6.06,-0.4972,5.406,0.9285,13.75

China Exports YoY | Type: macro_line | YoY %: 13.75 (2026-04-01) | Range: -14.55–39.64 | Trend(6pt): 20.5,6.06,-0.4972,5.406,0.9285,13.75

Today's Economic Events

| Data | Prior | Cons | Time |

|---|---|---|---|

| No events available | |||

- Mainland equities mixed with CSI 300 rising 0.21% while Shanghai Composite fell 0.43% to 4,090.48 amid thin data flow.

- Hong Kong shares dropped 1.59% to 23,924.81 as USD/HKD edged higher to 7.84.

- Taiwan’s TAIEX gained 1.28% to 46,465.20 on semiconductor demand resilience.

Yesterday's Recap

Mainland China equity markets showed divergence on June 21 with the CSI 300 advancing 0.21% to 4,941.60 while the Shanghai Composite declined 0.43% to 4,090.48. Hong Kong’s Hang Seng Index fell 1.59% to 23,924.81 as investors reacted to steady USD/HKD at 7.84. Taiwan’s TAIEX rose 1.28% to 46,465.20, supported by continued strength in AI-related exports.

USD/CNY remained unchanged at 6.77. Copper prices slipped 0.34% to 6.35 while Brent crude dropped 2.00% to 78.25. No major macroeconomic data releases occurred across mainland China, Hong Kong or Taiwan.

News flow centered on China’s reduction of US Treasury holdings to an 18-year low and ongoing discussions about yuan valuation. European Central Bank President Lagarde urged global talks on yuan undervaluation, adding external pressure on Chinese exchange-rate policy. Surging Chinese exports drew fresh G7 concern over renewed competitive pressure in European manufacturing.

The State Council approved further property transaction tax cuts in tier-2 cities to support domestic demand without aggressive monetary easing. Taiwan semiconductor exports rose 27.4% year-on-year in May, confirming resilient AI-driven demand.

The Day Ahead

The PBoC is scheduled to conduct reverse-repo operations on June 23 with an expected net liquidity injection of RMB 200 billion. No significant data releases are due in mainland China or Hong Kong on June 22-23. Taiwan will publish June export orders on June 25.

The HKMA plans to tender RMB 1.25 billion of 7-year bonds on June 25. Market participants will monitor any further signals from the State Council on property sector measures. Cross-strait trade tensions remain in focus following China’s atemoya purchase offer to Taiwan farmers, which has ignited domestic debate over agricultural trade dependence.

Other Economic Notes

China’s ongoing reduction in US Treasury holdings reflects both reserve management and geopolitical hedging. European Central Bank President Lagarde called for international talks on yuan undervaluation, highlighting external pressure on Chinese exchange-rate policy. Surging Chinese exports continue to draw concern at the G7, with Europe citing renewed competitive pressure in manufacturing sectors.

<i>↓ p.2</i>