Greater China Macro Daily(Beta Mode)

FDI Improves as PBOC Sets Weaker Yuan Fix

Market Snapshot

| Asset | Level | Change |

|---|---|---|

| Shanghai Composite | nan | +nan% |

| CSI 300 | nan | +nan% |

| Hang Seng | 23,336.28 | -1.82% |

| TAIEX | 47,100.65 | -1.34% |

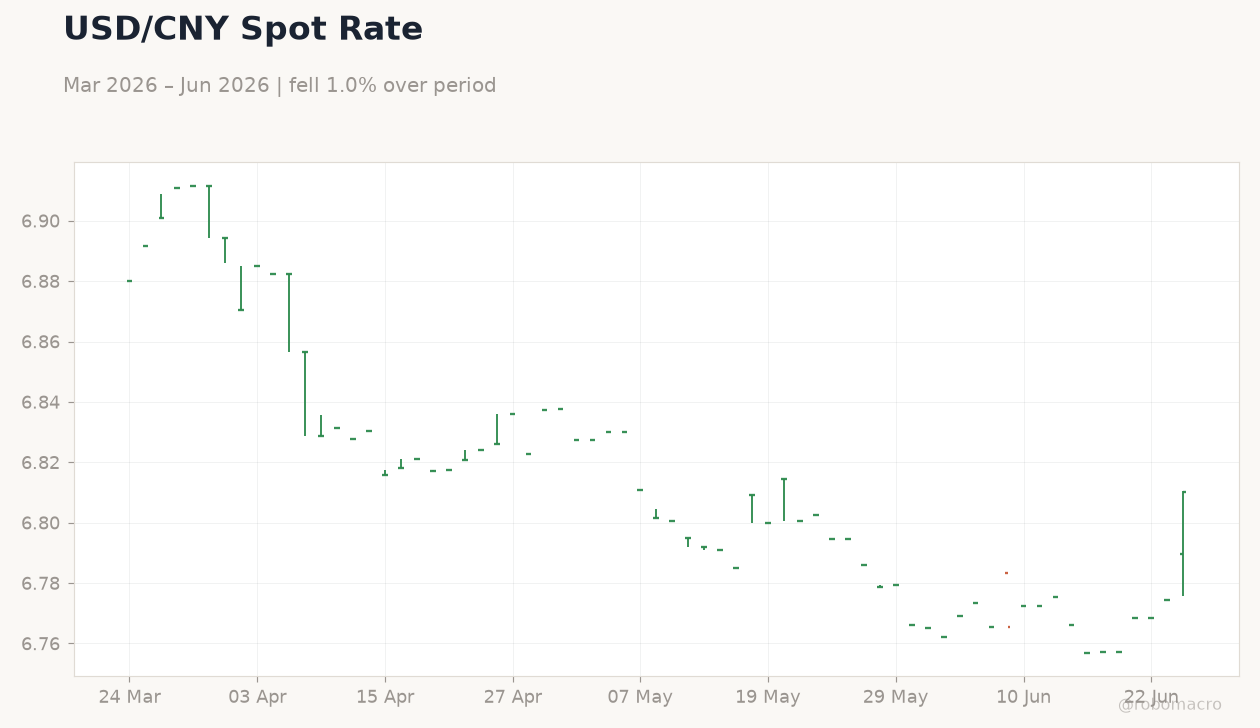

| USD/CNY | 6.81 | +0.53% |

| USD/HKD | 7.84 | -0.00% |

| Copper | 5.99 | -2.54% |

| Brent Crude | 73.18 | -5.06% |

| Gold | 4,016.40 | -2.75% |

| Bitcoin | 60,995.08 | -2.67% |

| China 2Y Govt Yield | - | - |

| China 10Y Govt Yield | - | - |

Prior Economic Events

| Data | Prior | Cons | Actual |

|---|---|---|---|

| FDI (YTD) Year-over-Year | -10.30 | - | -8.60 |

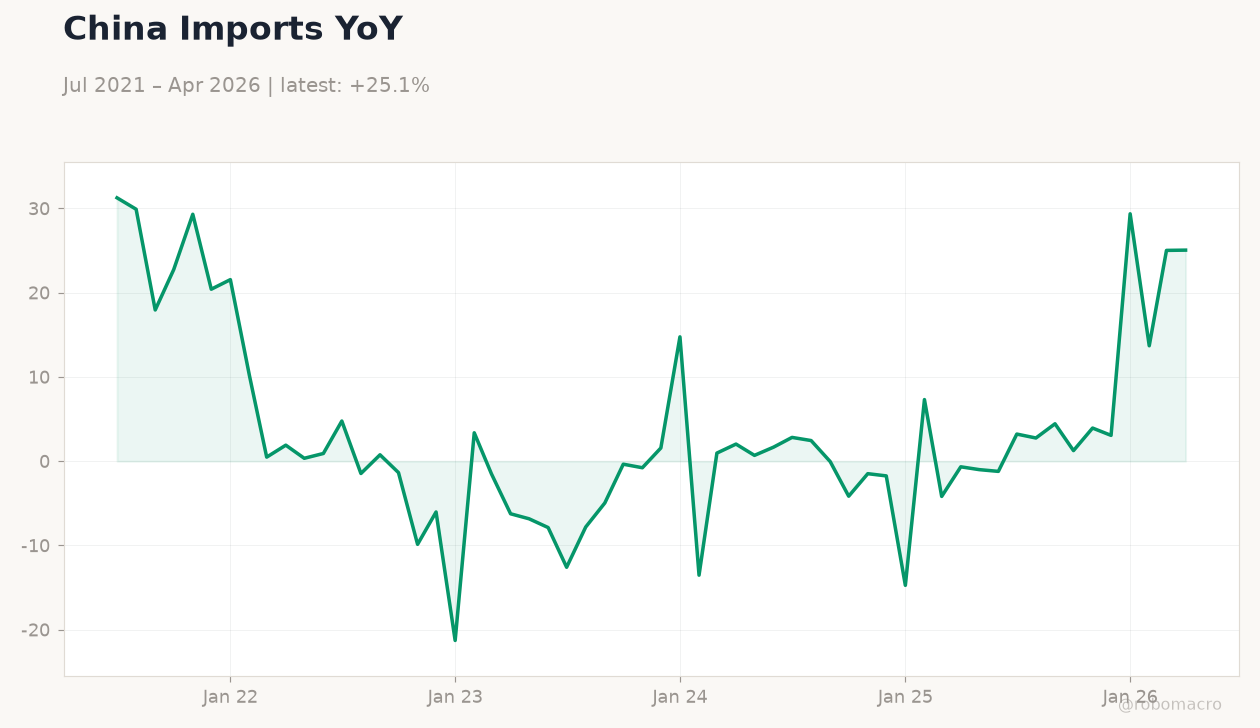

China Exports YoY | Type: macro_line | YoY %: 13.75 (2026-04-01) | Range: -14.55–39.64 | Trend(6pt): 20.5,6.06,-0.4972,5.406,0.9285,13.75

China Exports YoY | Type: macro_line | YoY %: 13.75 (2026-04-01) | Range: -14.55–39.64 | Trend(6pt): 20.5,6.06,-0.4972,5.406,0.9285,13.75

Today's Economic Events

| Data | Prior | Cons | Time |

|---|---|---|---|

| No events available | |||

- China FDI (YTD) YoY rose to -8.6% from -10.3%, signaling modest stabilization in inflows.

- Hang Seng fell 1.82% to 23,336.28 and TAIEX dropped 1.34% to 47,100.65 amid trade concerns.

- USD/CNY climbed 0.53% to 6.81 as PBoC set a weaker fixing for the fourth straight session.

Yesterday's Recap

China released FDI (YTD) YoY data showing an improvement to -8.6% from the prior -10.3%, reflecting slightly better foreign investment momentum on the mainland. Equity markets in Hong Kong and Taiwan declined, with the Hang Seng falling 1.82% to 23,336.28 and the TAIEX slipping 1.34% to 47,100.65. The PBoC fixed USD/CNY at 6.8171, extending its streak of weaker daily settings and allowing the spot rate to rise 0.53% to 6.81.

Copper prices dropped 2.54% to 5.99 while Brent crude fell 5.06% to 73.18, weighing on growth-sensitive assets. Hong Kong equities faced additional pressure from global risk-off flows, while Taiwan shares reflected semiconductor inventory digestion. No major data emerged from Hong Kong or Taiwan.

The Day Ahead

No data releases are scheduled for mainland China, Hong Kong, or Taiwan today. PBoC will conduct routine 7-day reverse repo operations to manage liquidity. HKMA is set to publish May foreign reserve figures, which should confirm ample reserves supporting the USD/HKD peg.

Markets will monitor any State Council comments on export policy amid ongoing trade tensions. CBC has no policy meeting planned.

Other Economic Notes

Beijing continues to prioritize growth over currency stability, as evidenced by successive weaker yuan fixings that support exporters. Property sector sentiment remains soft, with developers offering discounts in tier-2 cities without fresh policy support. Cross-strait trade flows show Taiwan gaining from rerouted supply chains even as mainland export surges draw EU and US scrutiny.

Semiconductor demand in Taiwan faces near-term inventory headwinds despite longer-term AI tailwinds.

Global Macro News

Rising US dollar strength to 13-month highs pressures Asian currencies and complicates PBoC efforts to manage yuan volatility. Escalating US-China and EU-China tariff disputes threaten to further fragment trade routes, with third-country gains proving uneven. Iran and Russia continue shifting oil settlements into yuan, underscoring Beijing's push to expand the currency's international role.

<i>↓ p.2</i>