Greater China Macro Daily(Beta Mode)

PBOC Sets Weaker Yuan Fix, TAIEX Slides 2.2%

Market Snapshot

| Asset | Level | Change |

|---|---|---|

| Shanghai Composite | 4,110.81 | +0.11% |

| CSI 300 | 4,943.02 | +0.48% |

| Hang Seng | 23,412.18 | +0.33% |

| TAIEX | 46,043.60 | -2.24% |

| USD/CNY | 6.79 | -0.01% |

| USD/HKD | 7.84 | -0.01% |

| Copper | 6.13 | +3.15% |

| Brent Crude | 75.00 | +1.71% |

| Gold | 4,041.60 | +1.29% |

| Bitcoin | 60,031.20 | -1.58% |

| China 2Y Govt Yield | - | - |

| China 10Y Govt Yield | - | - |

Prior Economic Events

| Data | Prior | Cons | Actual |

|---|---|---|---|

| FDI (YTD) Year-over-Year | -10.30 | - | -8.60 |

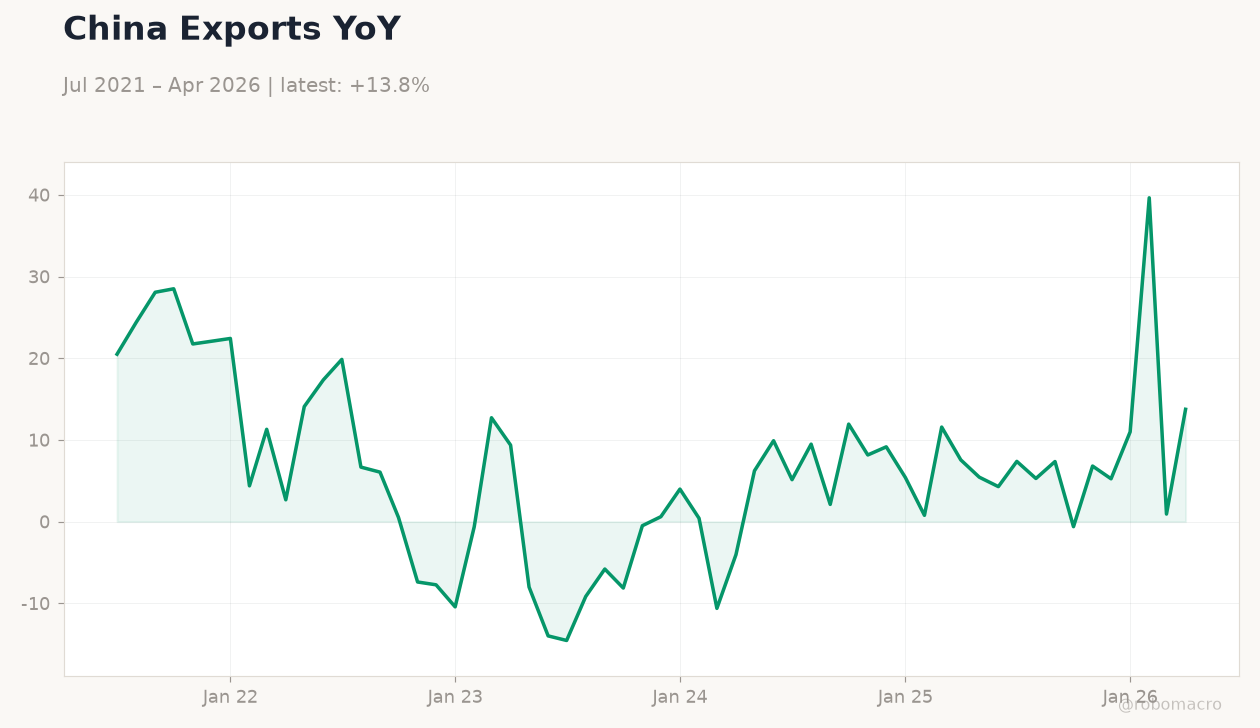

China Imports YoY | Type: macro_line | YoY %: 25.05 (2026-04-01) | Range: -21.28–31.26 | Trend(6pt): 31.26,0.7601,-0.7759,-14.73,25.02,25.05

China Imports YoY | Type: macro_line | YoY %: 25.05 (2026-04-01) | Range: -21.28–31.26 | Trend(6pt): 31.26,0.7601,-0.7759,-14.73,25.02,25.05

Today's Economic Events

| Data | Prior | Cons | Time |

|---|---|---|---|

| No events available | |||

- China FDI YTD YoY improved to -8.6% from -10.3%, signaling modest stabilization in inflows.

- CSI 300 rose 0.48% while TAIEX fell 2.24% amid divergent regional equity moves.

- PBOC guided a weaker USD/CNY fix for the fourth session, prioritizing growth over rapid appreciation.

Yesterday's Recap

China released FDI (YTD) YoY data showing contraction narrowed to 8.6%, an improvement from the prior 10.3% decline and indicating tentative stabilization in foreign investment. Mainland equities posted modest gains as Shanghai Composite advanced 0.11% to 4,110.81 and CSI 300 climbed 0.48% to 4,943.02 on selective buying. Hong Kong's Hang Seng index rose 0.33% to 23,412.18 with USD/HKD steady at 7.84.

Taiwan's TAIEX dropped 2.24% to 46,043.60 as semiconductor names faced pressure despite broader AI demand. USD/CNY held near 6.79 after PBOC set a weaker daily fixing above market estimates. Copper jumped 3.15% to 6.13, reflecting improved China growth sentiment, while Brent crude gained 1.71% to 75.00 and gold rose 1.29% to 4,041.60.

The Day Ahead

No major data releases are scheduled for today or tomorrow across mainland China, Hong Kong or Taiwan. Focus will remain on PBoC daily liquidity operations and any further yuan fixing adjustments that could reinforce depreciation signals. HKMA aggregate balance trends and HKD positioning near the weak band end warrant monitoring for peg stability.

Taiwan semiconductor export momentum and potential CBC FX comments may influence TWD flows. Broader commodity price moves, including copper as a China proxy, could shape regional risk sentiment ahead of the weekend.

Other Economic Notes

Premier Li stressed openness to global trade even as surging Chinese exports draw international criticism and tariff responses. Property developers continue to face muted onshore bond issuance absent fresh stimulus measures from the State Council. Export rerouting after US tariffs produces uneven gains for third countries while Taiwan expands its tech footprint in advanced packaging.

Yuan depreciation expectations have risen as policymakers favor growth support over currency strength.

Global Macro News

Iran and Russia have expanded yuan usage for oil and trade settlements to bypass dollar sanctions, accelerating de-dollarization trends that benefit China's currency internationalization. Brazil has begun preparations for its first yuan-denominated sovereign bonds in China, further widening Beijing's financial reach. <i>↓ p.2</i>