Greater China Macro Daily(Beta Mode)

China FDI Improves, Equities Slide Sharply

Market Snapshot

| Asset | Level | Change |

|---|---|---|

| Shanghai Composite | 4,027.26 | -2.26% |

| CSI 300 | 4,868.22 | -1.51% |

| Hang Seng | 22,671.86 | -1.76% |

| TAIEX | 44,571.76 | -3.64% |

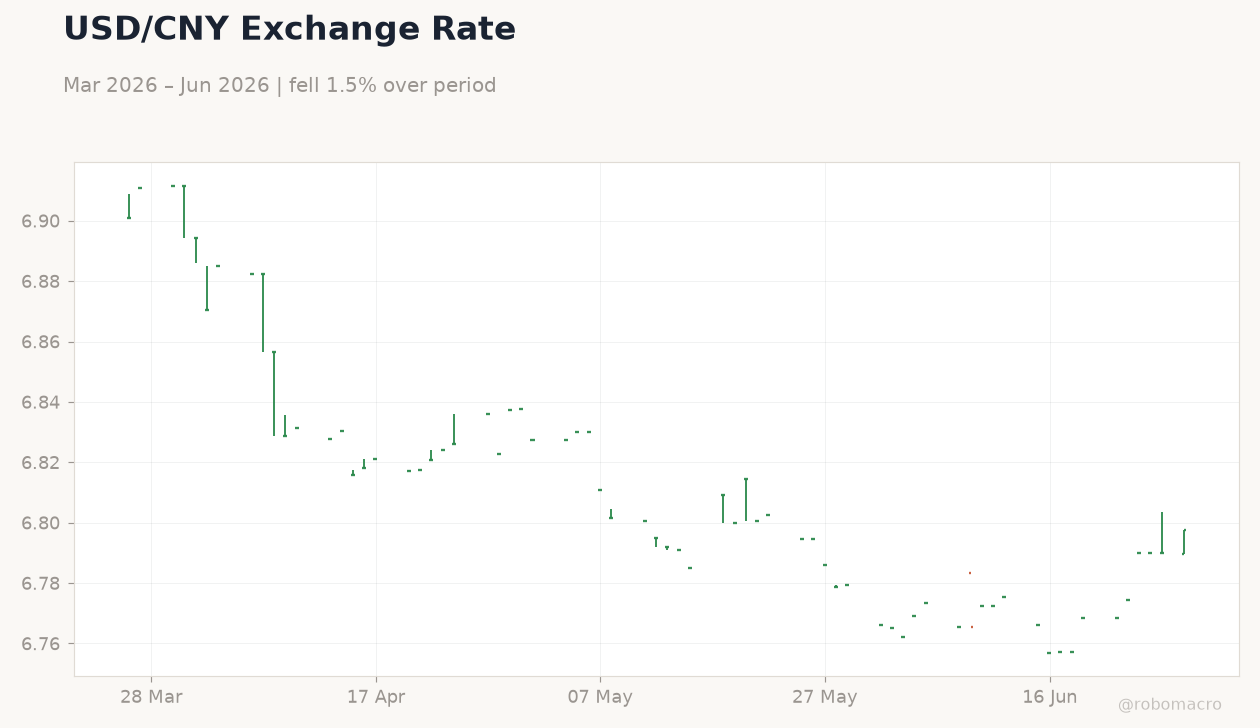

| USD/CNY | 6.79 | -0.00% |

| USD/HKD | 7.84 | +0.02% |

| Copper | 6.21 | +2.25% |

| Brent Crude | 72.60 | -3.53% |

| Gold | 4,096.30 | +1.63% |

| Bitcoin | 59,517.00 | -0.71% |

| China 2Y Govt Yield | - | - |

| China 10Y Govt Yield | - | - |

Prior Economic Events

| Data | Prior | Cons | Actual |

|---|---|---|---|

| FDI (YTD) Year-over-Year | -10.30 | - | -8.60 |

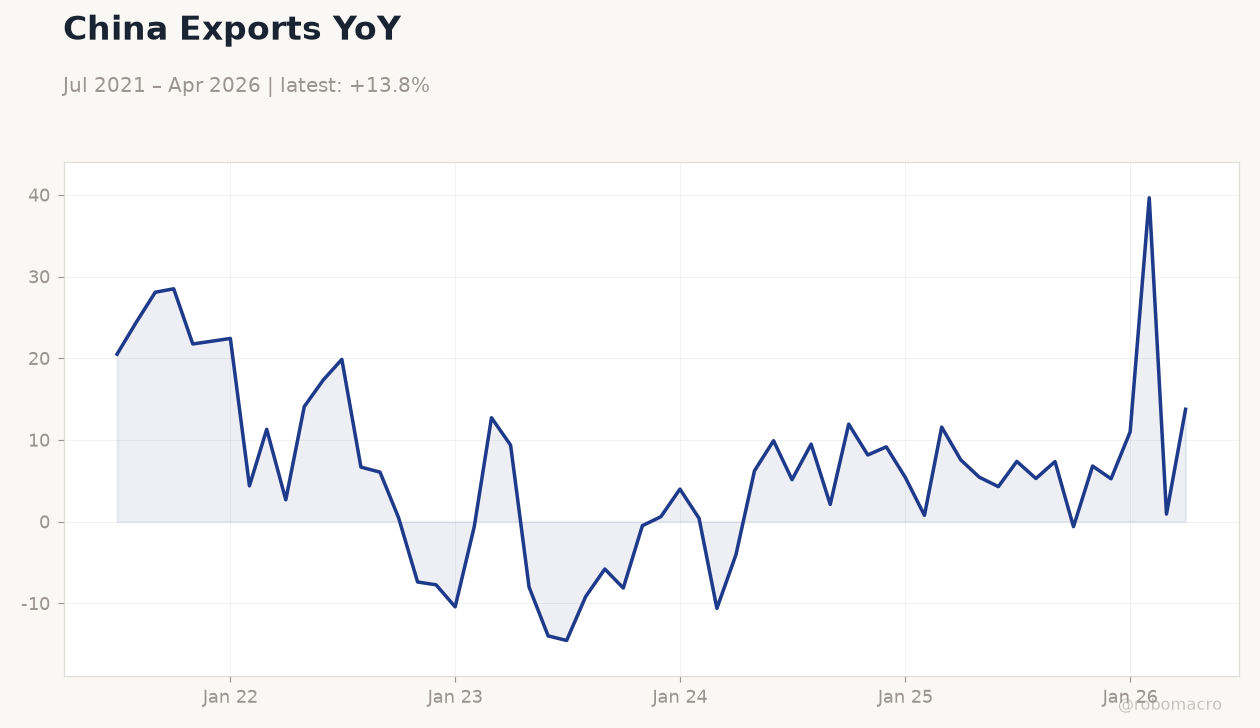

China Exports YoY | Type: macro_line | YoY %: 13.75 (2026-04-01) | Range: -14.55–39.64 | Trend(6pt): 20.5,6.06,-0.4972,5.406,0.9285,13.75

China Exports YoY | Type: macro_line | YoY %: 13.75 (2026-04-01) | Range: -14.55–39.64 | Trend(6pt): 20.5,6.06,-0.4972,5.406,0.9285,13.75

Today's Economic Events

| Data | Prior | Cons | Time |

|---|---|---|---|

| No events available | |||

- China FDI YTD YoY rose to -8.6% from -10.3%, showing modest improvement in mainland inflows.

- Shanghai Composite fell 2.26% to 4,027.26 while TAIEX dropped 3.64% to 44,571.76 amid broad risk-off moves.

- Copper gained 2.25% to 6.21 on China demand signals as Brent Crude declined 3.53% to 72.60.

Yesterday's Recap

Mainland China released FDI data showing the year-to-date decline narrowed to 8.6% from 10.3% previously, pointing to a slower pace of contraction in foreign investment. Shanghai Composite declined 2.26% to close at 4,027.26 while CSI 300 fell 1.51% to 4,868.22 as investors rotated out of growth names. Hong Kong’s Hang Seng Index dropped 1.76% to 22,671.86 with property and tech shares leading losses.

Taiwan’s TAIEX posted the steepest decline, falling 3.64% to 44,571.76 as semiconductor names faced selling pressure. USD/CNY held steady at 6.79 while USD/HKD edged 0.02% higher to 7.84, remaining well inside the peg band. Copper rose 2.25% to 6.21, reflecting optimism around mainland industrial demand, whereas Brent Crude fell 3.53% to 72.60 and gold advanced 1.63% to 4,096.30.

The Day Ahead

No major data releases are scheduled across mainland China, Hong Kong or Taiwan. Markets will focus on PBoC liquidity operations and any follow-through commentary on industrial profit trends. Hong Kong investors may watch USD/HKD aggregate balance movements for peg signals.

Taiwan semiconductor supply-chain updates could influence TAIEX sentiment given ongoing export-order strength. Overall trading volumes are expected to remain moderate ahead of the weekend.

Other Economic Notes

China’s January-May industrial profits rose 18.8% year-over-year, though the pace moderated from earlier months, indicating export gains have not fully offset domestic weakness. Beijing is weighing revisions to gold import and export rules, which could affect physical flows and vaulting activity in Hong Kong. The new five-year energy plan leaves room for further coal consumption growth, underscoring the priority given to energy security over rapid decarbonization.

Hong Kong recorded the fastest ultra-high-net-worth population growth among major wealth centers, supporting local asset-management inflows.

Global Macro News

US-China tariff tensions continue to produce uneven gains for third countries, with some ASEAN economies capturing more redirected trade than others. China stated it can withstand a full freeze in EU trade ties, reducing immediate downside risks to export forecasts. Wall Street semiconductor stocks weakened again, pressuring Taiwan-linked names through global supply-chain linkages.

<i>↓ p.2</i>