Greater China Macro Daily(Beta Mode)

China PMIs Beat, CSI 300 Surges 2.4%

Market Snapshot

| Asset | Level | Change |

|---|---|---|

| Shanghai Composite | 4,096.67 | +0.56% |

| CSI 300 | 4,984.07 | +2.38% |

| Hang Seng | 22,881.02 | -0.63% |

| TAIEX | 47,221.36 | +2.37% |

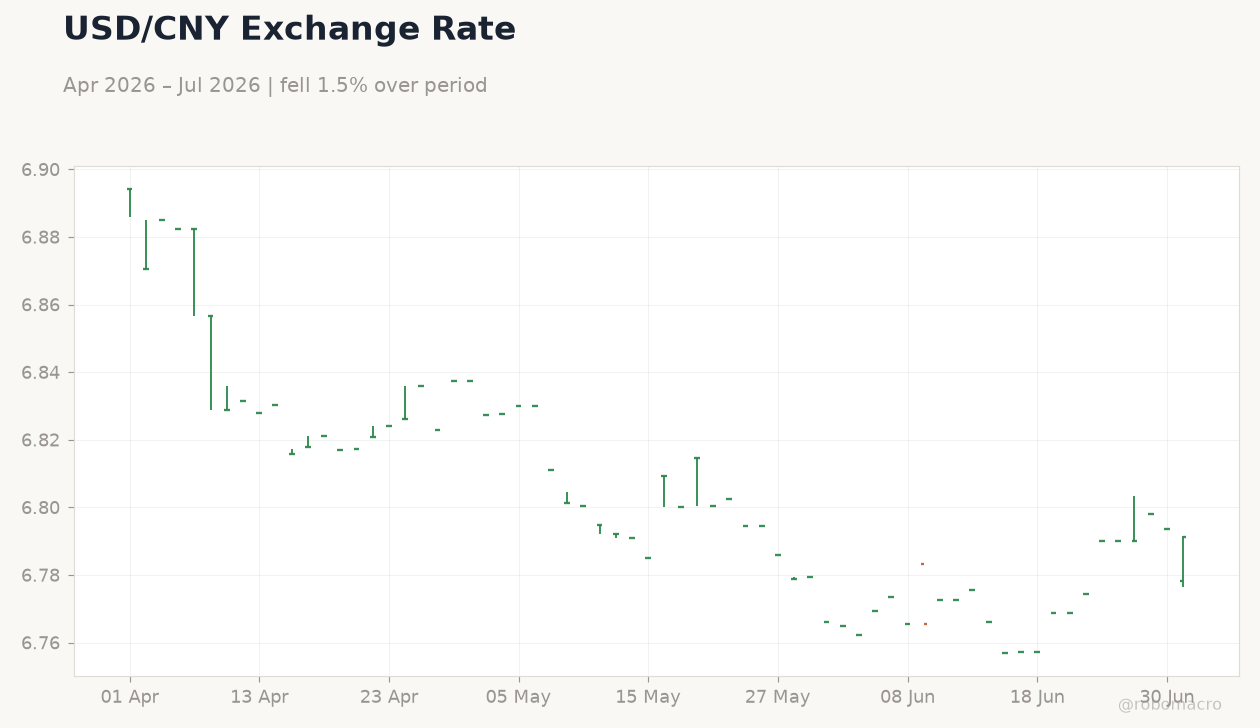

| USD/CNY | 6.79 | -0.05% |

| USD/HKD | 7.84 | +0.03% |

| Copper | 6.19 | +1.50% |

| Brent Crude | 73.21 | +0.08% |

| Gold | 3,990.80 | -0.78% |

| Bitcoin | 58,680.15 | -2.42% |

| China 2Y Govt Yield | - | - |

| China 10Y Govt Yield | - | - |

Prior Economic Events

| Data | Prior | Cons | Actual |

|---|---|---|---|

| NBS Manufacturing PMI | 50 | 50.10 | 50.30 |

| NBS Non-Manufacturing PMI | 50.10 | 49.90 | 50.20 |

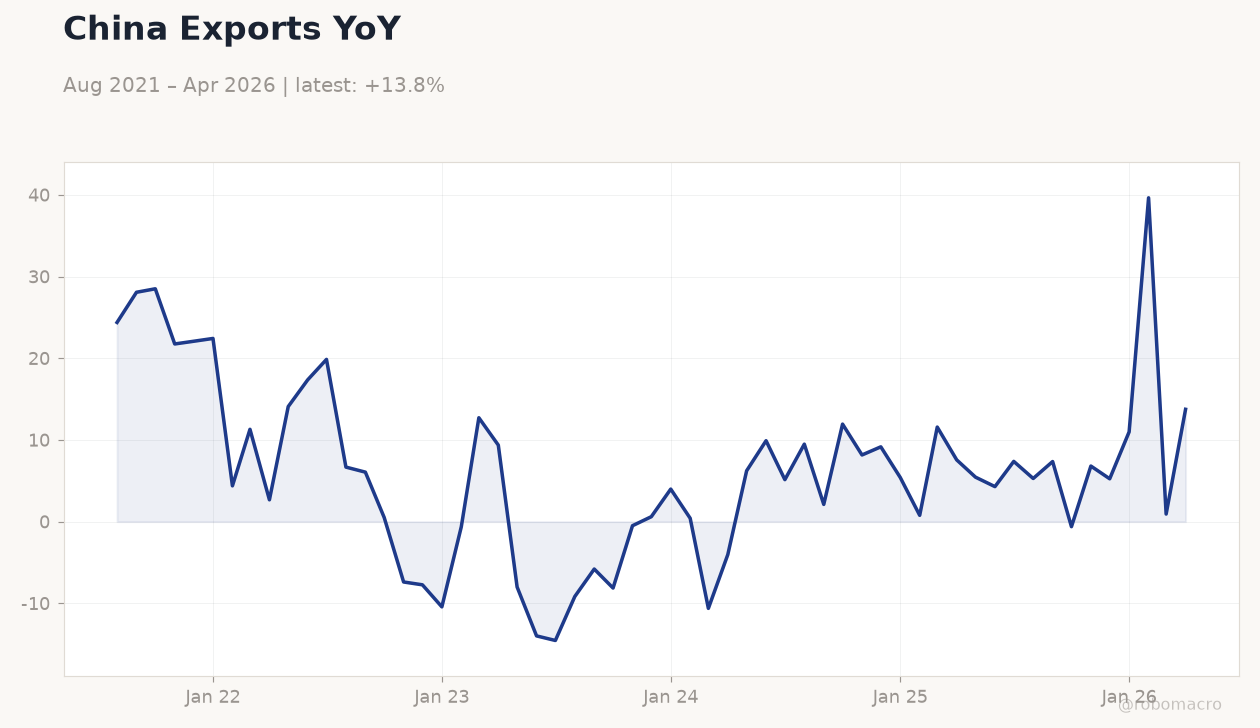

China Exports YoY | Type: macro_line | YoY %: 13.75 (2026-04-01) | Range: -14.55–39.64 | Trend(5pt): 24.38,0.5134,0.6066,0.7746,13.75

China Exports YoY | Type: macro_line | YoY %: 13.75 (2026-04-01) | Range: -14.55–39.64 | Trend(5pt): 24.38,0.5134,0.6066,0.7746,13.75

Today's Economic Events

| Data | Prior | Cons | Time |

|---|---|---|---|

| RatingDog Manufacturing PMI | - | 51.70 | 17:45 |

| RatingDog Services PMI | - | 53.60 | 17:45 |

- China June NBS Manufacturing PMI rose to 50.3 versus 50.1 consensus, with non-manufacturing at 50.2.

- CSI 300 gained 2.38% to 4,984.07 while Shanghai Composite rose 0.56%; Hang Seng fell 0.63%.

- PBoC signaled patient policy stance after data beat, keeping focus on liquidity support.

Yesterday's Recap

China’s June NBS Manufacturing PMI printed at 50.3, above the 50.1 consensus and 50.0 prior, while non-manufacturing PMI reached 50.2 against 49.9 expected. The beat was driven by new orders and production, supporting a soft-landing view for the mainland economy. Shanghai Composite closed at 4,096.67, up 0.56%, and CSI 300 jumped 2.38% to 4,984.07 on stimulus hopes.

Hong Kong’s Hang Seng Index declined 0.63% to 22,881.02 amid thin volume in developers. Taiwan’s TAIEX rose 2.37% to 47,221.36, supported by AI-related semiconductor demand. USD/CNY fixed stronger at 6.8109 and closed near 6.79, while USD/HKD held at 7.84.

Copper rose 1.50% to 6.19 on China demand optimism. Export strength lifted the official PMI readings, with analysts noting the surprise upside reflected resilient overseas orders despite ongoing trade tensions with the EU. Property names led mainland gains as investors positioned ahead of the Politburo meeting.

In Hong Kong, developers remained under pressure from weak transaction data and elevated borrowing costs. Taiwan’s advance was concentrated in AI supply-chain names, offsetting broader regional caution. The stronger yuan fix helped anchor sentiment and limited USD/CNY volatility near month-end.

The Day Ahead

RatingDog Manufacturing PMI is scheduled for release at 17:45 ET today, with consensus at 51.7. RatingDog Services PMI follows at the same time, expected at 53.6. Markets will watch for confirmation of the official PMI momentum in mainland China.

No major data releases are listed for Hong Kong or Taiwan. Traders will also monitor any PBoC liquidity operations ahead of month-end. The private survey is expected to corroborate the export-driven improvement seen in the NBS figures.

Any material divergence could shift expectations around near-term policy easing. Month-end funding conditions remain the key focus for money-market desks, with the PBoC likely to conduct fine-tuning operations to keep interbank rates stable.

Other Economic Notes

Mainland property sector saw continued restructuring efforts, with creditor support for onshore bond frameworks reducing contagion risks. <i>↓ p.2</i>