Greater China Macro Daily(Beta Mode)

China PMI Holds, Equities Slide as Yuan Firms

Market Snapshot

| Asset | Level | Change |

|---|---|---|

| Shanghai Composite | 4,021.16 | -2.22% |

| CSI 300 | 4,812.30 | -2.96% |

| Hang Seng | 22,881.02 | -0.63% |

| TAIEX | 47,018.99 | +1.94% |

| USD/CNY | 6.79 | -0.08% |

| USD/HKD | 7.84 | +0.00% |

| Copper | 6.18 | +0.85% |

| Brent Crude | 71.54 | -0.04% |

| Gold | 4,135.50 | +1.65% |

| Bitcoin | 61,485.48 | +2.47% |

| China 2Y Govt Yield | - | - |

| China 10Y Govt Yield | - | - |

Prior Economic Events

| Data | Prior | Cons | Actual |

|---|---|---|---|

| RatingDog Manufacturing PMI | 51.80 | 51.60 | 51.70 |

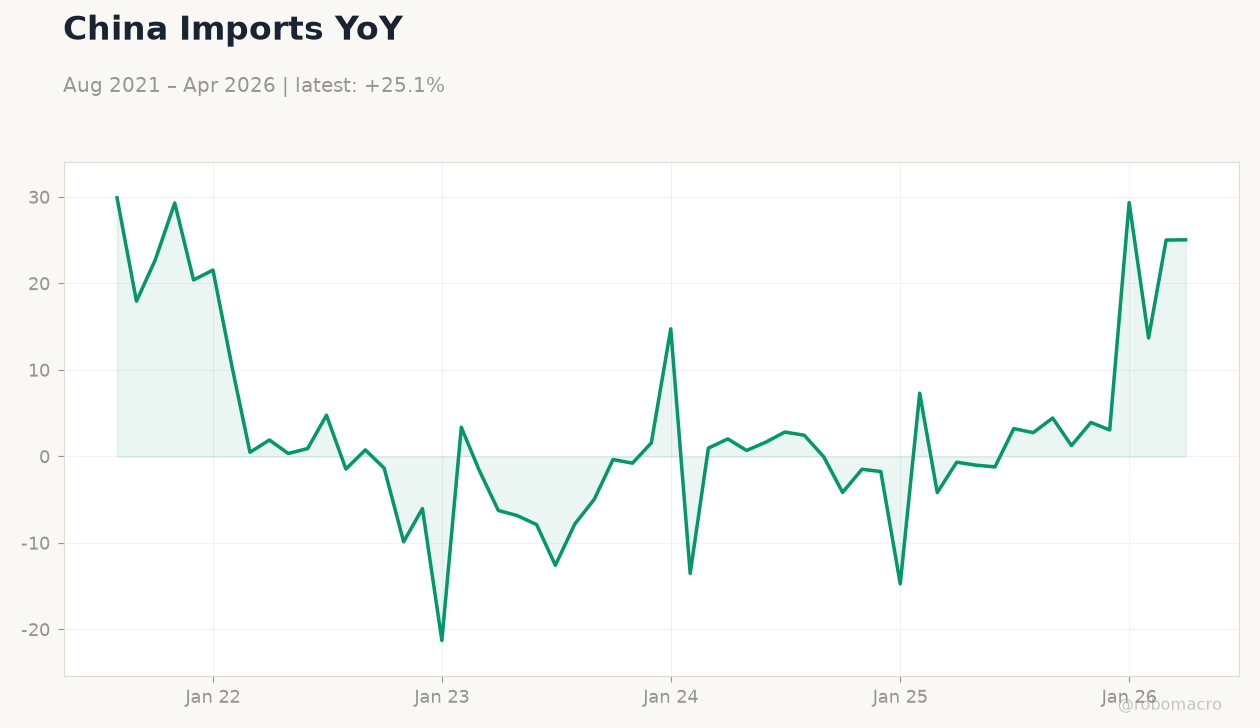

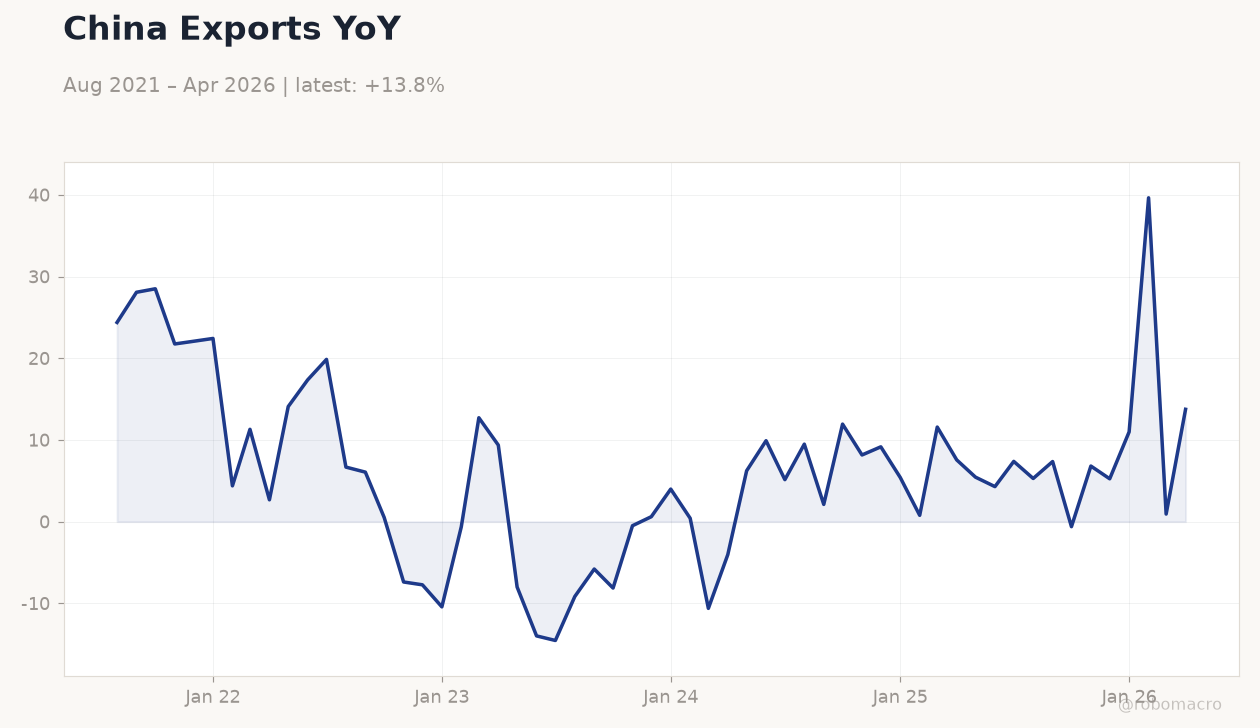

China Exports YoY | Type: macro_line | YoY %: 13.75 (2026-04-01) | Range: -14.55–39.64 | Trend(5pt): 24.38,0.5134,0.6066,0.7746,13.75

China Exports YoY | Type: macro_line | YoY %: 13.75 (2026-04-01) | Range: -14.55–39.64 | Trend(5pt): 24.38,0.5134,0.6066,0.7746,13.75

Today's Economic Events

| Data | Prior | Cons | Time |

|---|---|---|---|

| RatingDog Services PMI | - | 53.60 | 17:45 |

- China RatingDog Manufacturing PMI printed 51.7 in June, beating consensus 51.6 but below prior 51.8, signaling steady mainland expansion.

- Shanghai Composite fell 2.22% to 4,021.16 and CSI 300 dropped 2.96% to 4,812.30, while TAIEX rose 1.94% to 47,018.99.

- HKMA urged banks to expand cross-border yuan usage to support real economy activity amid stable USD/HKD peg at 7.84.

Yesterday's Recap

Mainland China’s RatingDog Manufacturing PMI edged to 51.7, indicating modest expansion in factory activity. Equity markets in mainland China sold off sharply with Shanghai Composite declining 2.22% to close at 4,021.16 and CSI 300 falling 2.96% to 4,812.30. Hong Kong’s Hang Seng Index eased 0.63% to 22,881.02 while Taiwan’s TAIEX advanced 1.94% to 47,018.99 on semiconductor strength.

USD/CNY tightened 0.08% to 6.79 after the PBoC fixed the dollar-yuan midpoint at 6.8088. Copper rose 0.85% to 6.18, reflecting mild optimism on China demand. HKMA statements emphasized greater yuan internationalization to underpin trade and investment flows without altering aggregate balance levels.

The Day Ahead

Markets will focus on today’s China RatingDog Services PMI release, with consensus at 53.6. PBoC is scheduled to conduct standard liquidity operations including reverse repos. No policy meetings are set for HKMA or CBC.

Taiwan export order data and any follow-up on cross-strait trade signals could influence sentiment. Regional equity futures point to cautious opening after yesterday’s mixed closes.

Other Economic Notes

Property support measures in mainland China continue to target tier-2 cities but leave tier-3/4 overhang unresolved. EU officials expressed concern over stalled trade reset talks with Beijing, highlighting persistent bilateral imbalances. Semiconductor supply chains remain a Taiwan growth driver, with recent export gains supporting steady CBC policy.

Cross-border yuan initiatives from Hong Kong aim to deepen real-economy linkages without immediate peg implications.

Global Macro News

US June payrolls added only 57,000 jobs, well below forecasts and raising prospects for earlier Fed easing that could ease pressure on USD/CNY. Canada posted its strongest monthly growth since last summer, providing a mild positive backdrop for commodity demand. South Korea inflation reached a two-and-a-half-year high, increasing the chance of a July rate hike that may affect regional capital flows.

<i>↓ p.2</i>