Greater China Macro Daily(Beta Mode)

PBoC Signals Yuan Strength; HKMA Boosts RMB Use

Market Snapshot

| Asset | Level | Change |

|---|---|---|

| Shanghai Composite | 4,043.64 | +0.37% |

| CSI 300 | 4,842.17 | +0.62% |

| Hang Seng | 23,350.03 | +1.28% |

| TAIEX | 46,780.62 | +0.08% |

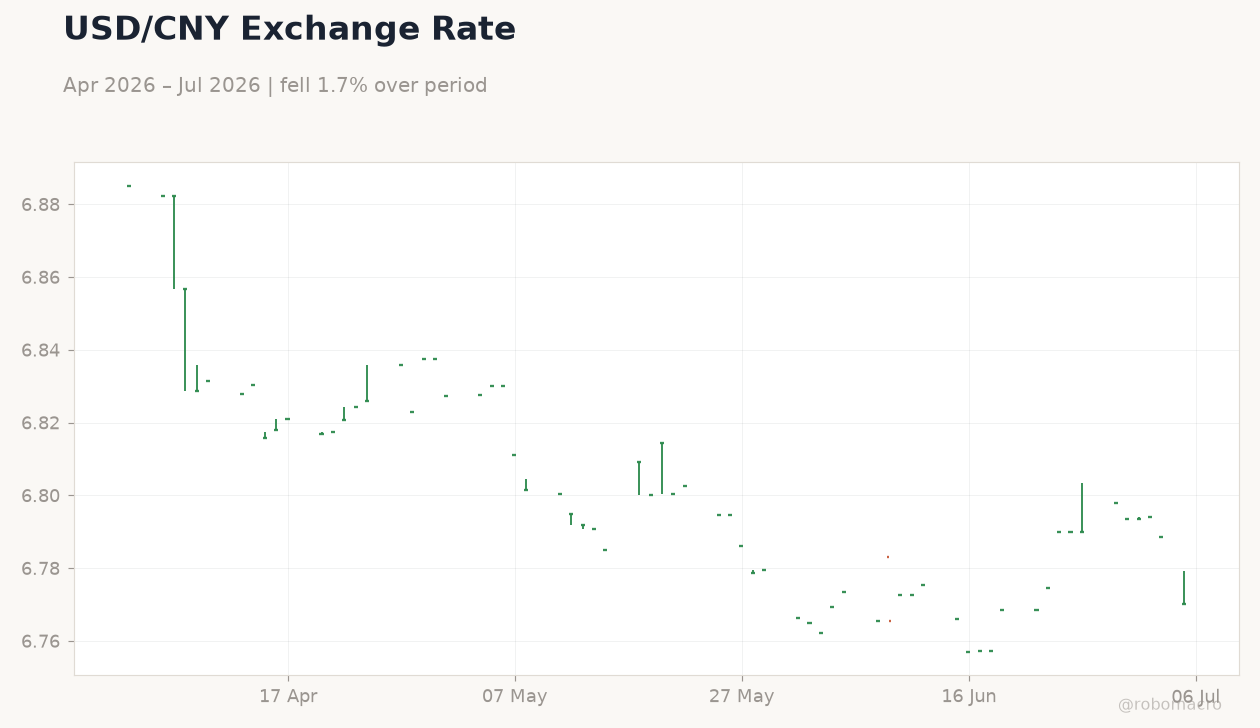

| USD/CNY | 6.77 | -0.27% |

| USD/HKD | 7.84 | -0.01% |

| Copper | 6.22 | +1.79% |

| Brent Crude | 72.13 | +0.46% |

| Gold | 4,187.30 | +1.81% |

| Bitcoin | 63,006.41 | -0.13% |

| China 2Y Govt Yield | - | - |

| China 10Y Govt Yield | - | - |

Prior Economic Events

| Data | Prior | Cons | Actual |

|---|---|---|---|

| No events available | |||

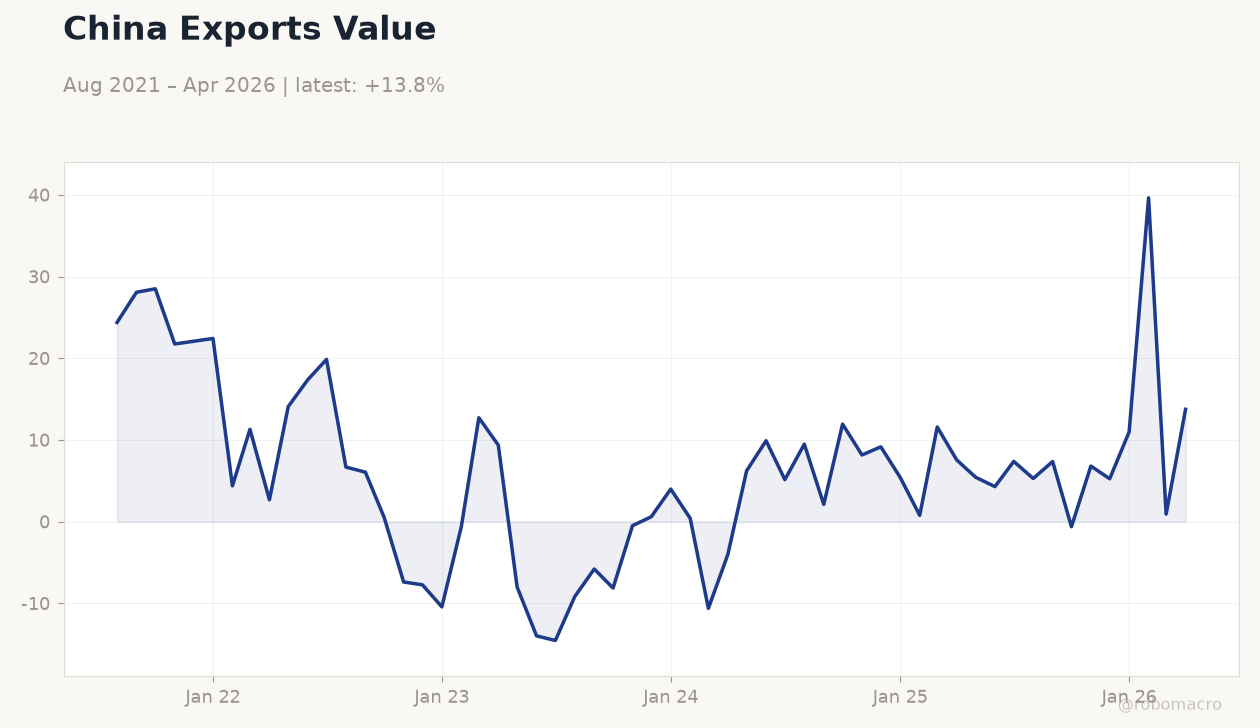

China Exports Value | Type: macro_line | USD bn: 13.75 (2026-04-01) | Range: -14.55–39.64 | Trend(5pt): 24.38,0.5134,0.6066,0.7746,13.75

China Exports Value | Type: macro_line | USD bn: 13.75 (2026-04-01) | Range: -14.55–39.64 | Trend(5pt): 24.38,0.5134,0.6066,0.7746,13.75

Today's Economic Events

| Data | Prior | Cons | Time |

|---|---|---|---|

| Inflation Rate Year-over-Year | 1.20 | 1.20 | 21:30 |

| Inflation Rate Month-over-Month | -0.10 | - | 21:30 |

| Producer Price Index Year-over-Year | 3.90 | 4.10 | 21:30 |

- PBoC set firmer USD/CNY fix, guiding managed yuan strength amid soft growth signals.

- HKMA urged banks to broaden yuan products and will launch new internationalization measures in coming weeks.

- Equities rose across Greater China with Shanghai Composite +0.37% and Hang Seng +1.28% on thin holiday volume.

Yesterday's Recap

Mainland China markets closed higher on July 4 despite thin holiday-adjusted volumes. Shanghai Composite rose 0.37% to 4,043.64 while CSI 300 gained 0.62% to 4,842.17, supported by selective buying in banks and renewables. Hong Kong equities outperformed as Hang Seng advanced 1.28% to 23,350.03, led by tech and property names.

Taiwan’s TAIEX edged up 0.08% to 46,780.62 with semiconductor names mixed. USD/CNY fell 0.27% to 6.77 after the PBoC’s firmer fix, while USD/HKD stayed inside the peg at 7.84. Copper rose 1.79% to 6.22 as a China growth proxy, and Brent crude gained 0.46% to 72.13.

The Day Ahead

China will release June CPI YoY, CPI MoM and PPI YoY on July 8 at 21:30 ET, with consensus at 1.2% YoY and 4.1% for PPI. Markets will watch for any signs of persistent deflationary pressure that could reinforce calls for further PBoC easing. No major data releases are scheduled for Hong Kong or Taiwan on July 6.

HKMA is expected to announce additional yuan internationalization steps in the coming weeks. Traders will also monitor aggregate balance levels for any signs of intervention.

Other Economic Notes

June credit data released earlier this week showed total social financing below expectations, keeping alive the case for a possible MLF or LPR cut later in July. Property sector restructuring continues with recent court approval for Country Garden’s onshore bonds, though broad re-rating still requires demand-side stimulus. Semiconductor export growth in Taiwan slowed to 18.4% y/y in May, the weakest reading since February, highlighting downside risks to the island’s trade balance.

Global Macro News

European policymakers expressed concern over Chinese industrial competition and called for yuan adjustments to protect German manufacturers. The Federal Reserve continues to assess AI-driven productivity effects on the US economy, with indirect implications for Taiwan’s chip supply chain. Chile’s finance minister signaled a turning point in June activity and expects a second-half rebound that could support copper prices.

Global commodity markets remained supported by China demand signals, with gold rising 1.81% to 4,187.30. Cross-border yuan usage is expanding in Africa as Beijing builds financial infrastructure to reduce dollar dependence.