India Macro Daily(Beta Mode)

Industrial Output Misses, Stocks Fall

Market Snapshot

| Asset | Level | Change |

|---|---|---|

| Nifty 50 | 24,865.70 | -1.24% |

| Sensex | 80,238.85 | -1.29% |

| USD/INR | 92.00 | +0.48% |

| EUR/INR | 106.55 | -0.43% |

| Reliance | 1,358.00 | -2.58% |

| HDFC Bank | 879.40 | -0.94% |

| Brent Crude | 82.64 | +6.30% |

| Gold | 5,171.60 | -2.32% |

| Bitcoin | 68,161.97 | -0.89% |

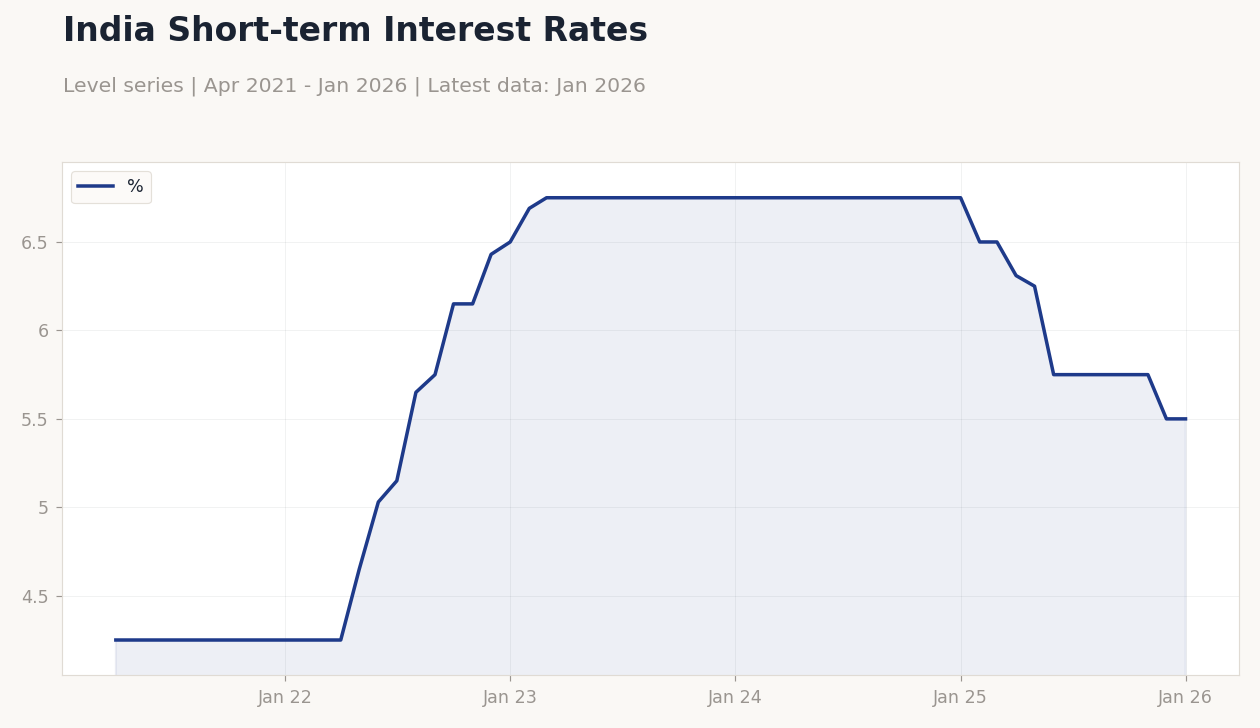

| India Short-term Rate | 5.50% | +0.00% |

| India Long-term Rate | - | - |

Prior Economic Events

| Data | Prior | Cons | Actual |

|---|---|---|---|

| Industrial Production Year-over-Year | 8 | 6.50 | 4.80 |

| Manufacturing Production Year-over-Year | 8.40 | - | 4.80 |

| Current Account Balance | -14,100m | - | -13,200m |

Today's Economic Events

| Data | Prior | Cons | Time |

|---|---|---|---|

| No events available | |||

- Industrial production slowed to 4.8% YoY, missing consensus of 6.5%, signaling manufacturing weakness amid global headwinds.

- Current account deficit narrowed to -$13.2 billion, better than previous -$14.1 billion, supporting rupee stability.

- Equities declined with Nifty 50 down 1.24% and Sensex off 1.29%, pressured by geopolitical risks and FII outflows.

Yesterday's Recap

India's industrial production grew 4.8% year-over-year in January, falling short of the 6.5% consensus and previous 8%, reflecting slowdowns in manufacturing and export demand. Manufacturing production also eased to 4.8% YoY from 8.4%, highlighting vulnerabilities in key sectors like autos and textiles amid rising input costs. The current account balance improved to a deficit of $13.2 billion from $14.1 billion prior, aided by lower oil imports and resilient services exports.

Equity markets reacted negatively, with the Nifty 50 closing at 24,865.70 after a 1.24% drop, driven by losses in heavyweights like Reliance (-2.58%). The Sensex fell 1.29% to 80,238.85, as banking stocks such as HDFC Bank (-0.94%) weighed on sentiment. Rupee weakened 0.48% to 92.00 against the USD, influenced by FII selling amid Middle East tensions.

Bond yields held steady, with short-term rates at 5.50% unchanged, as markets digested the softer data without immediate RBI signals.

The Day Ahead

Indian stock exchanges BSE and NSE will remain closed today for the Holi holiday, halting trading in equities, derivatives, and currency segments. No major economic data releases are scheduled for March 3, providing a brief pause amid recent volatility. Attention turns to potential global spillovers, including oil price movements from Middle East conflicts.

Tomorrow, March 4, also lacks key India-specific events, though markets may reopen with focus on rupee dynamics and FII flows. Investors should monitor any RBI liquidity operations if needed to stabilize short-term rates. Overall, the quiet calendar allows digestion of yesterday's data misses.

Other Economic Notes

India's growth trajectory faces risks from stretched valuations and geopolitical uncertainties, with analysts noting potential for lackluster equity performance this year. Recent sell-offs amid Iran-Israel tensions could pressure the rupee. Infrastructure spending aims to bolster long-term growth in sectors like transportation and power.

India Inc raised $4.435 billion via ECBs in December 2025, led by NBFCs and airlines, amid US Fed rate cuts. Analysts suggest betting on certain stocks amid US-Iran conflict to hedge volatility.