India Macro Daily(Beta Mode)

Markets Sink on Oil Spike

Market Snapshot

| Asset | Level | Change |

|---|---|---|

| Nifty 50 | 23,866.85 | -1.63% |

| Sensex | 76,863.71 | -1.72% |

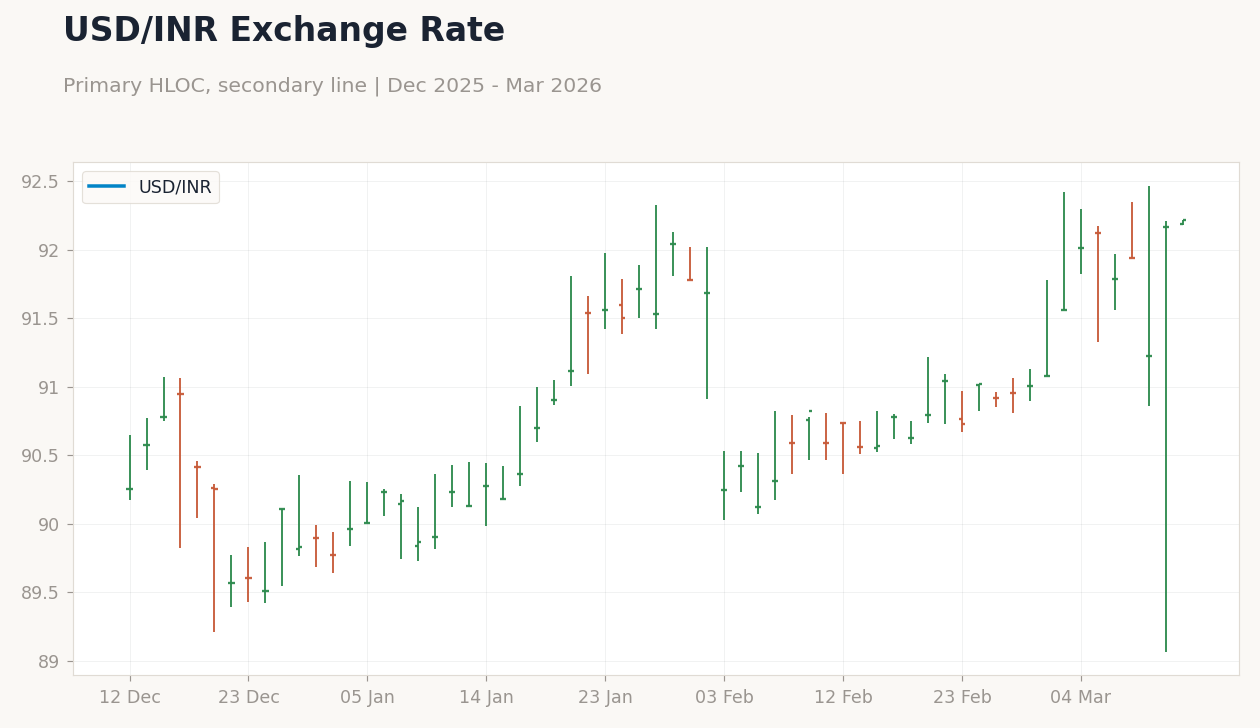

| USD/INR | 92.19 | +0.02% |

| EUR/INR | 106.39 | -0.30% |

| Reliance | 1,406.10 | -0.19% |

| HDFC Bank | 841.45 | -0.94% |

| Brent Crude | 95.31 | +8.55% |

| Gold | 5,146.70 | -1.59% |

| Bitcoin | 70,301.72 | +0.54% |

| India Short-term Rate | 5.50% | +0.00% |

| India Long-term Rate | - | - |

Prior Economic Events

| Data | Prior | Cons | Actual |

|---|---|---|---|

| No events available | |||

Nifty 50 Index | Type: market_hloc | Nifty 50: 2.387e+04 (2026-03-11) | Range: 2.387e+04–2.633e+04 | Trend(5pt): 2.59e+04,2.633e+04,2.518e+04,2.573e+04,2.387e+04

Nifty 50 Index | Type: market_hloc | Nifty 50: 2.387e+04 (2026-03-11) | Range: 2.387e+04–2.633e+04 | Trend(5pt): 2.59e+04,2.633e+04,2.518e+04,2.573e+04,2.387e+04

Today's Economic Events

| Data | Prior | Cons | Time |

|---|---|---|---|

| Thursday (2026-03-12) | |||

| Inflation Rate Year-over-Year | 2.13 | 3.10 | 02:30 |

- Indian equities tumbled amid surging oil prices, with Nifty 50 down 1.63% and Sensex falling 1.72%.

- Brent crude jumped 8.55% to $95.31, pressuring rupee and inflation outlook.

- RBI revises bank dividend norms, tying payouts to CET1 ratios for financial stability.

Yesterday's Recap

Indian markets faced sharp declines yesterday as geopolitical tensions drove oil prices higher, exacerbating concerns over import costs and inflation. The Nifty 50 closed at 23,866.85, down 1.63%, while the Sensex ended at 76,863.71, shedding 1.72%, with heavy selling in banking and energy sectors. USD/INR edged up 0.02% to 92.19, reflecting mild rupee pressure, whereas EUR/INR dipped 0.30% to 106.39 amid global currency shifts.

Key stocks like Reliance fell 0.19% to 1,406.10, and HDFC Bank dropped 0.94% to 841.45, mirroring broader market sentiment. Gold prices declined 1.59% to 5,146.70, losing safe-haven appeal, while Bitcoin rose 0.54% to 70,301.72. India short-term rates held steady at 5.50%, with no change, signaling stable liquidity conditions.

No major data releases occurred, but news of potential oil-driven GDP risks weighed on investor confidence.

The Day Ahead

Investors eye tomorrow's inflation rate year-over-year release at 02:30 ET, with consensus at 3.1% against previous 2.13%, potentially influencing RBI's policy stance. This medium-impact data could signal easing price pressures if it undershoots expectations, supporting rupee stability. No events are scheduled for today, allowing markets to digest recent oil volatility and global cues.

Broader focus remains on West Asia developments, which may indirectly affect India's energy imports and equity flows.

Other Economic Notes

Rising oil prices pose a significant risk to India's growth trajectory, with warnings that a $50 surge could erase 2% of GDP through higher import bills and fiscal strain. Cybersecurity talent shortages highlight vulnerabilities in India Inc., potentially disrupting IT services and financial sectors amid growing digital threats. Government plans for Rs 2.8 lakh crore additional spending aim to bolster infrastructure, but escalating energy costs may offset these stimulus effects on domestic demand.

Global Macro News

Global oil markets remain volatile as West Asia conflicts disrupt shipments, with Brent crude's 8.55% rise amplifying India's energy import challenges and stoking inflation fears. (cont...)