India Macro Daily(Beta Mode)

Rupee Weakens on Oil Surge

Market Snapshot

| Asset | Level | Change |

|---|---|---|

| Nifty 50 | 23,151.10 | -2.06% |

| Sensex | 74,563.92 | -1.93% |

| USD/INR | 92.49 | +0.28% |

| EUR/INR | 105.62 | -0.70% |

| Reliance | 1,395.20 | +0.22% |

| HDFC Bank | 819.05 | -1.65% |

| Brent Crude | 103.86 | +3.38% |

| Gold | 5,023.10 | -1.81% |

| Bitcoin | 70,680.31 | +0.27% |

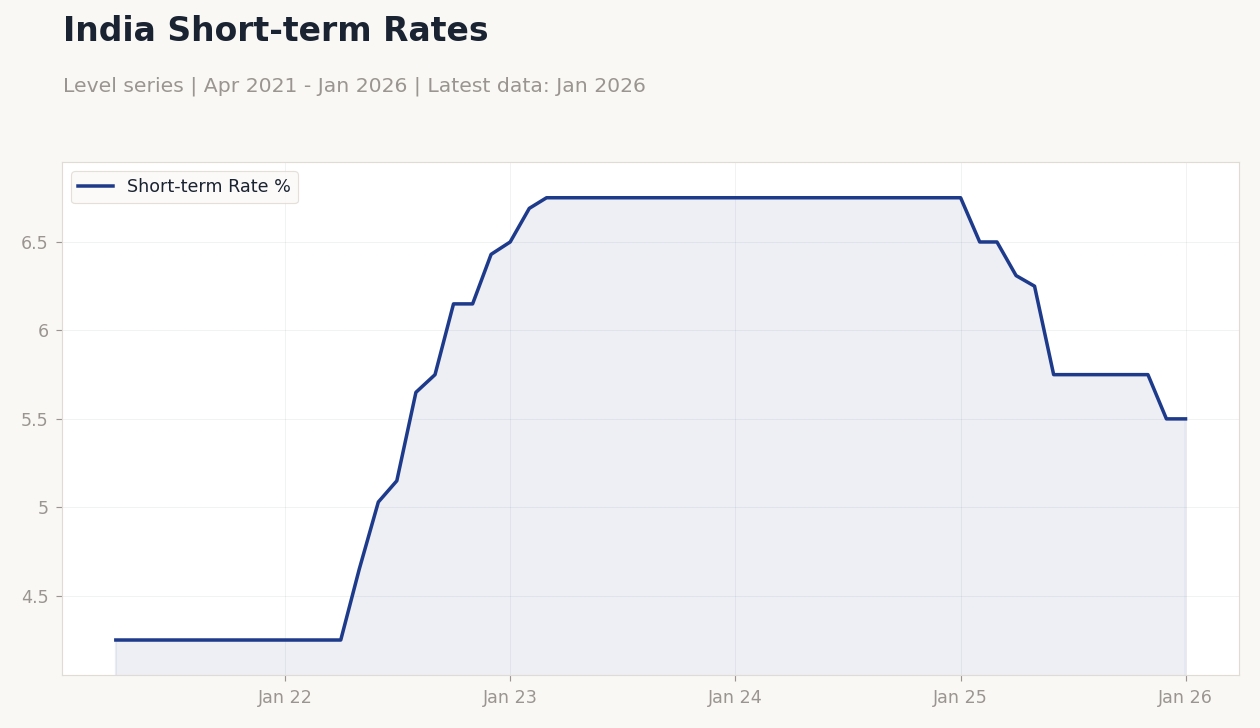

| India Short-term Rate | 5.50% | +0.00% |

| India Long-term Rate | - | - |

Prior Economic Events

| Data | Prior | Cons | Actual |

|---|---|---|---|

| Inflation Rate Year-over-Year | 2.75 | 3.10 | 3.21 |

India Short-term Rates | Type: macro_line | Short-term Rate %: 5.5 (2026-01-01) | Range: 4.25–6.75 | Trend(5pt): 4.25,5.03,6.75,6.75,5.5

India Short-term Rates | Type: macro_line | Short-term Rate %: 5.5 (2026-01-01) | Range: 4.25–6.75 | Trend(5pt): 4.25,5.03,6.75,6.75,5.5

Today's Economic Events

| Data | Prior | Cons | Time |

|---|---|---|---|

| No events available | |||

- India's February inflation rose to 3.21% YoY, slightly above consensus of 3.1%, pressuring the rupee amid elevated oil prices.

- Equity markets tumbled, with Nifty 50 down 2.06% and Sensex down 1.93%, driven by global risk-off sentiment and forex outflows.

- RBI injected ₹50,000 crore in liquidity and intervened to support the rupee, as reserves fell $11.7 billion to $716.8 billion.

Yesterday's Recap

India's February inflation rate climbed to 3.21% year-over-year, exceeding the consensus estimate of 3.1% and higher than the previous 2.75%, fueled by rising food and fuel costs amid geopolitical tensions. This data release coincided with sharp market declines, as the Nifty 50 index closed at 23,151.10 after dropping 2.06%, reflecting investor concerns over imported inflation from surging Brent crude prices at $103.86, up 3.38%. The Sensex fell 1.93% to 74,563.92, with key drags from banking stocks like HDFC Bank, which declined 1.65% to 819.05, amid broader sell-offs tied to rupee depreciation.

USD/INR rose 0.28% to 92.49, marking a fresh low as oil import bills swelled, while EUR/INR eased 0.70% to 105.62 on relative dollar strength. Reliance Industries bucked the trend, gaining 0.22% to 1,395.20, supported by energy sector resilience despite the crude rally. Forex reserves dropped $11.7 billion to $716.8 billion, attributed to RBI interventions to stem rupee losses amid market routs.

Overall, these moves underscored vulnerability in India's growth trajectory, with IT services facing headwinds from global volatility.

The Day Ahead

With no major economic data releases scheduled for today, markets will focus on ongoing geopolitical developments, particularly in the Middle East, which could further influence oil prices and rupee dynamics. Attention turns to potential RBI liquidity operations, as forward premiums signal bets on an impending FX swap to bolster reserves. Broader sentiment may hinge on global cues, including US trade probes targeting India, potentially affecting export-oriented sectors like IT services.

Equity traders will monitor Nifty and Sensex for rebound opportunities, though persistent oil shocks could cap gains. Without events tomorrow, the outlook remains data-light, emphasizing rupee stability and inflation targeting. Investors should watch for any unscheduled RBI announcements on monetary policy.

Other Economic Notes

Broader economic themes highlight India's exposure to global commodity shocks, with $100-plus oil prices straining the current account deficit and challenging the 6-7% GDP growth trajectory. (cont...)