India Macro Daily(Beta Mode)

Rupee Hits Record Low on Oil Surge

Market Snapshot

| Asset | Level | Change |

|---|---|---|

| Nifty 50 | 23,114.50 | +0.49% |

| Sensex | 74,532.96 | +0.44% |

| USD/INR | 93.65 | +0.43% |

| EUR/INR | 108.40 | +1.61% |

| Reliance | 1,414.40 | +2.14% |

| HDFC Bank | 780.45 | -2.22% |

| Brent Crude | 106.41 | -2.06% |

| Gold | 4,574.90 | -0.56% |

| Bitcoin | 70,276.18 | -0.35% |

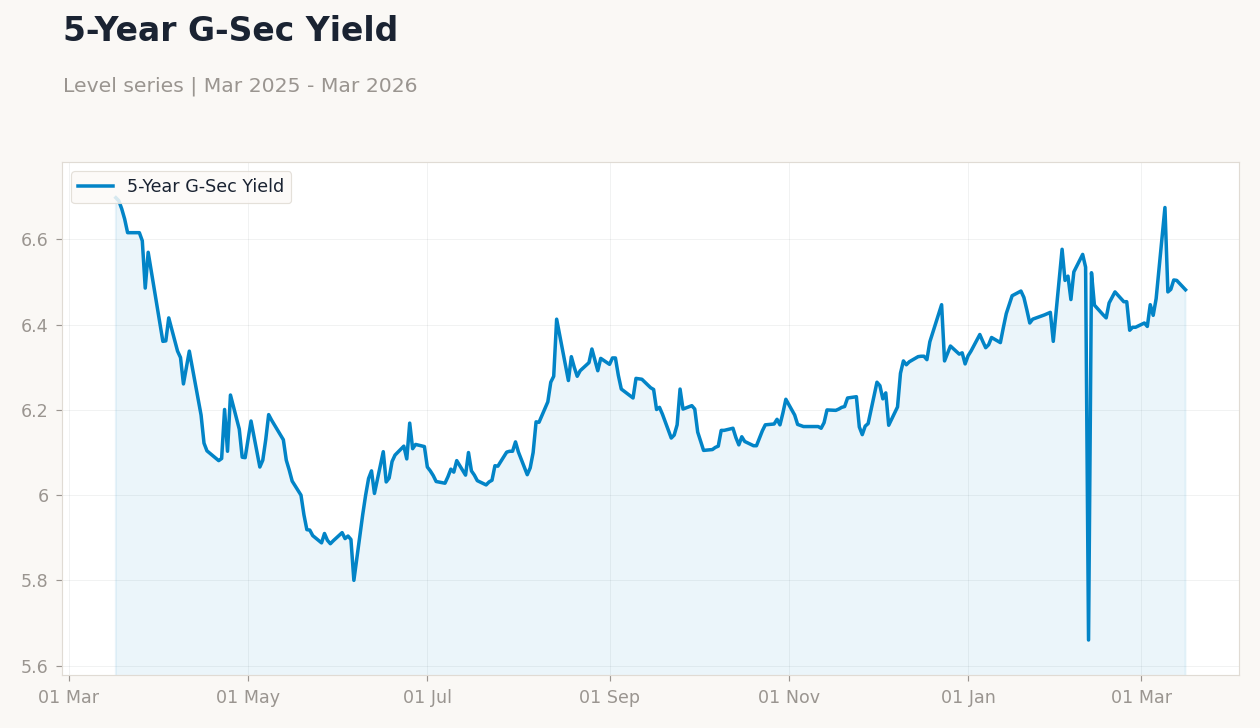

| India Short-term Rate | 5.50% | +0.00% |

| India Long-term Rate | - | - |

Prior Economic Events

| Data | Prior | Cons | Actual |

|---|---|---|---|

| No events available | |||

India Short-Term Policy Rates | Type: macro_line | Short-Term Rate %: 5.5 (2026-02-01) | Range: 4.25–6.75 | Trend(5pt): 4.25,5.025,6.75,6.75,5.5

India Short-Term Policy Rates | Type: macro_line | Short-Term Rate %: 5.5 (2026-02-01) | Range: 4.25–6.75 | Trend(5pt): 4.25,5.025,6.75,6.75,5.5

Today's Economic Events

| Data | Prior | Cons | Time |

|---|---|---|---|

| Tuesday (2026-03-24) | |||

| HSBC Composite PMI Flash | 58.90 | - | 01:00 |

| HSBC Manufacturing PMI Flash | 56.90 | - | 01:00 |

| HSBC Services PMI Flash | 58.10 | - | 01:00 |

- Indian rupee weakened past 93 against USD amid oil price pressures and global uncertainty, with USD/INR closing at 93.65 (+0.43%).

- Equity markets edged higher, Nifty 50 up 0.49% to 23,114.50 and Sensex up 0.44% to 74,532.96, led by gains in Reliance (+2.14%).

- RBI signals vigilance on currency volatility and inflation risks, supported by forex reserves and potential $1 trillion buffer.

Yesterday's Recap

Indian markets showed modest gains on March 20 despite rupee pressures, with the Nifty 50 advancing 0.49% to close at 23,114.50, driven by strength in energy stocks like Reliance Industries, which rose 2.14% to 1,414.40. The Sensex followed suit, climbing 0.44% to 74,532.96, though banking shares weighed in with HDFC Bank dropping 2.22% to 780.45 amid concerns over lending risks. The rupee depreciated sharply, with USD/INR up 0.43% to 93.65 and EUR/INR surging 1.61% to 108.40, attributed to oil surges and dollar strength.

Brent crude fell 2.06% to 106.41, providing some relief, while gold dipped 0.56% to 4,574.90 and Bitcoin eased 0.35% to 70,276.18. No major economic data releases occurred, but forex reserves fluctuated significantly, adding to market caution. India short-term rates held steady at 5.50%, reflecting RBI's unchanged repo rate stance.

The Day Ahead

On March 21, no immediate economic releases are scheduled for India, allowing markets to digest recent rupee volatility and global cues. Attention turns to March 24, when HSBC flash PMI data for composite, manufacturing, and services sectors will be released at 01:00 ET, with prior readings at 58.9, 56.9, and 58.1 respectively. These medium-impact indicators could signal growth momentum in manufacturing and services, influencing RBI's inflation outlook.

Investors will monitor any RBI interventions in forex markets amid ongoing rupee weakness. Broader events include potential updates on US-India trade talks, which could affect tariff pressures on the rupee.

Other Economic Notes

Broader economic themes highlight India's vulnerability to global oil surges and dollar strength, exacerbating rupee depreciation and inflation risks. Forex reserves fluctuations underscore the need for a robust buffer, with suggestions of building to $1 trillion to defend against external shocks. The IT sector views AI as an opportunity for growth rather than disruption, potentially boosting India's services exports and overall GDP trajectory.

Global Macro News

Global uncertainty, including escalating Middle East conflicts like Iran-related risks, has spurred oil price volatility, directly pressuring India's import bill and rupee stability. (cont...)