India Macro Daily(Beta Mode)

Rupee Slides on Iran Oil Tensions

Market Snapshot

| Asset | Level | Change |

|---|---|---|

| Nifty 50 | 23,114.50 | +0.49% |

| Sensex | 74,532.96 | +0.44% |

| USD/INR | 93.65 | +0.61% |

| EUR/INR | 108.29 | +0.75% |

| Reliance | 1,414.40 | +2.14% |

| HDFC Bank | 780.45 | -2.22% |

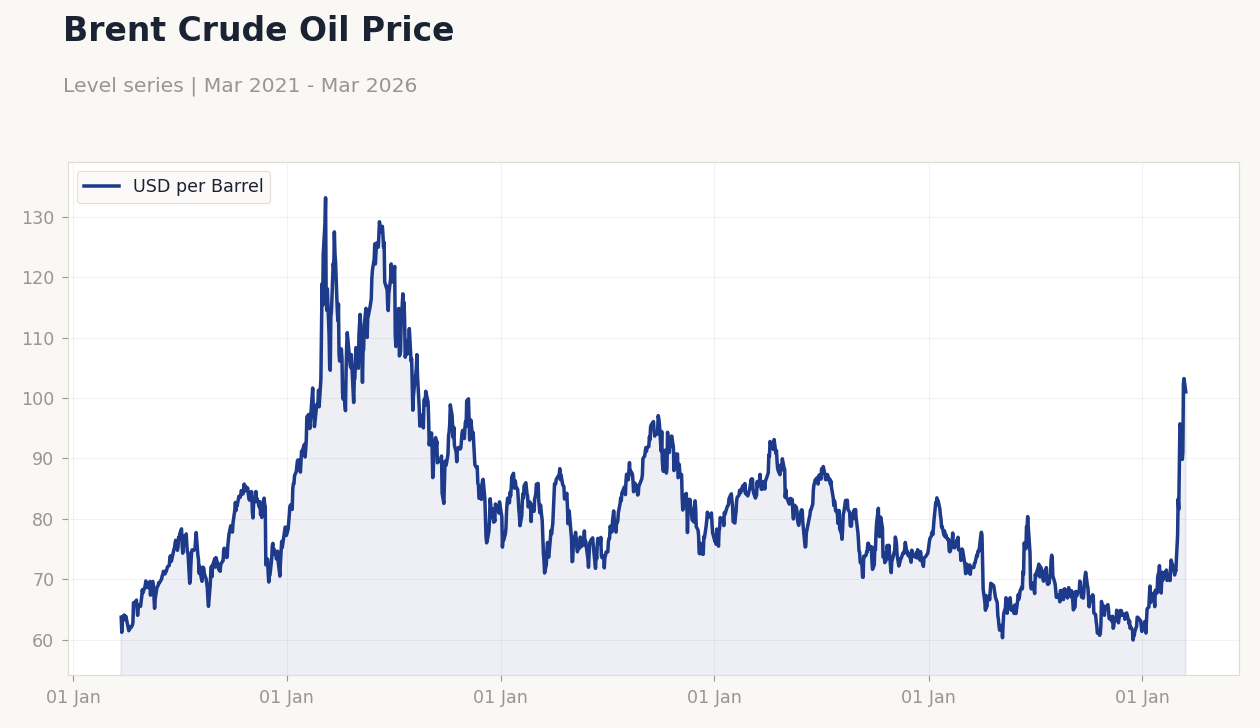

| Brent Crude | 106.73 | -4.87% |

| Gold | 4,429.80 | -3.08% |

| Bitcoin | 67,988.62 | -1.05% |

| India Short-term Rate | 5.50% | +0.00% |

| India Long-term Rate | - | - |

Prior Economic Events

| Data | Prior | Cons | Actual |

|---|---|---|---|

| No events available | |||

Brent Crude Oil Price | Type: macro_line | USD per Barrel: 101 (2026-03-16) | Range: 59.93–133.2 | Trend(6pt): 63.7,115.5,94.56,74.89,103.2,101

Brent Crude Oil Price | Type: macro_line | USD per Barrel: 101 (2026-03-16) | Range: 59.93–133.2 | Trend(6pt): 63.7,115.5,94.56,74.89,103.2,101

Today's Economic Events

| Data | Prior | Cons | Time |

|---|---|---|---|

| Tuesday (2026-03-24) | |||

| HSBC Composite PMI Flash | 58.90 | - | 01:00 |

| HSBC Manufacturing PMI Flash | 56.90 | - | 01:00 |

| HSBC Services PMI Flash | 58.10 | - | 01:00 |

- Rupee weakens amid Iran conflict, RBI intervenes to curb slide.

- Equities edge up despite FPI outflows; bonds firm on oil dip.

- Geopolitical risks spotlight India's oil imports, gold reserves.

Yesterday's Recap

Indian markets showed mixed performance amid geopolitical tensions, with the Nifty 50 closing at 23,114.50 after a 0.49% gain, driven by select large-caps like Reliance Industries, which rose 2.14% to 1,414.40. The Sensex advanced 0.44% to 74,532.96, though banking stocks weighed in, with HDFC Bank dropping 2.22% to 780.45 on broader sector concerns. The rupee depreciated sharply, with USD/INR climbing 0.61% to 93.65 and EUR/INR up 0.75% to 108.29, pressured by safe-haven dollar demand from the Iran war.

Brent Crude fell 4.87% to 106.73, providing some relief to import-dependent India, while Gold declined 3.08% to 4,429.80 amid reduced haven buying. Bitcoin slipped 1.05% to 67,988.62, tracking global risk aversion. India's short-term rate held steady at 5.50%, with no change, reflecting RBI's liquidity stance.

No major data releases occurred, but markets reacted to news of FPIs fleeing Indian debt due to global turmoil.

The Day Ahead

No significant economic releases are scheduled for tomorrow, March 23, leaving markets to digest ongoing geopolitical developments. Attention turns to Tuesday, March 24, with HSBC Flash PMIs at 01:00 ET, including Composite (previous 58.9), Manufacturing (previous 56.9), and Services (previous 58.1), which could signal early Q1 momentum. These PMI figures, all medium impact, may influence RBI rate cut expectations if they indicate softening growth.

Broader events include monitoring state bond auctions, as highlighted in recent news, potentially affecting yields. Investors will watch for any RBI interventions in forex markets amid rupee volatility. Global cues, such as Bank of Japan rate decisions, could indirectly impact Indian equities.

Other Economic Notes

India's push for critical mineral auctions, with 19 blocks up for bid, aims to mitigate supply chain risks from geopolitical uncertainties like China's export halts. The country's estimated $5 trillion gold hoard is under scrutiny as both an economic asset for reserves and a potential drag on productive investments. Energy transition discussions at the India-Africa meet underscore efforts to diversify away from oil dependency amid war-driven price spikes.

Alkem's launch of a ₹450 weight-loss drug highlights pharmaceutical sector innovation, potentially boosting exports.