India Macro Daily(Beta Mode)

RBI Curbs FX, Rupee Stabilizes

Market Snapshot

| Asset | Level | Change |

|---|---|---|

| Nifty 50 | 22,679.40 | +1.56% |

| Sensex | 73,134.32 | +1.65% |

| USD/INR | 92.94 | +0.33% |

| EUR/INR | 107.30 | -0.62% |

| Reliance | 1,369.90 | +1.93% |

| HDFC Bank | 746.90 | +2.10% |

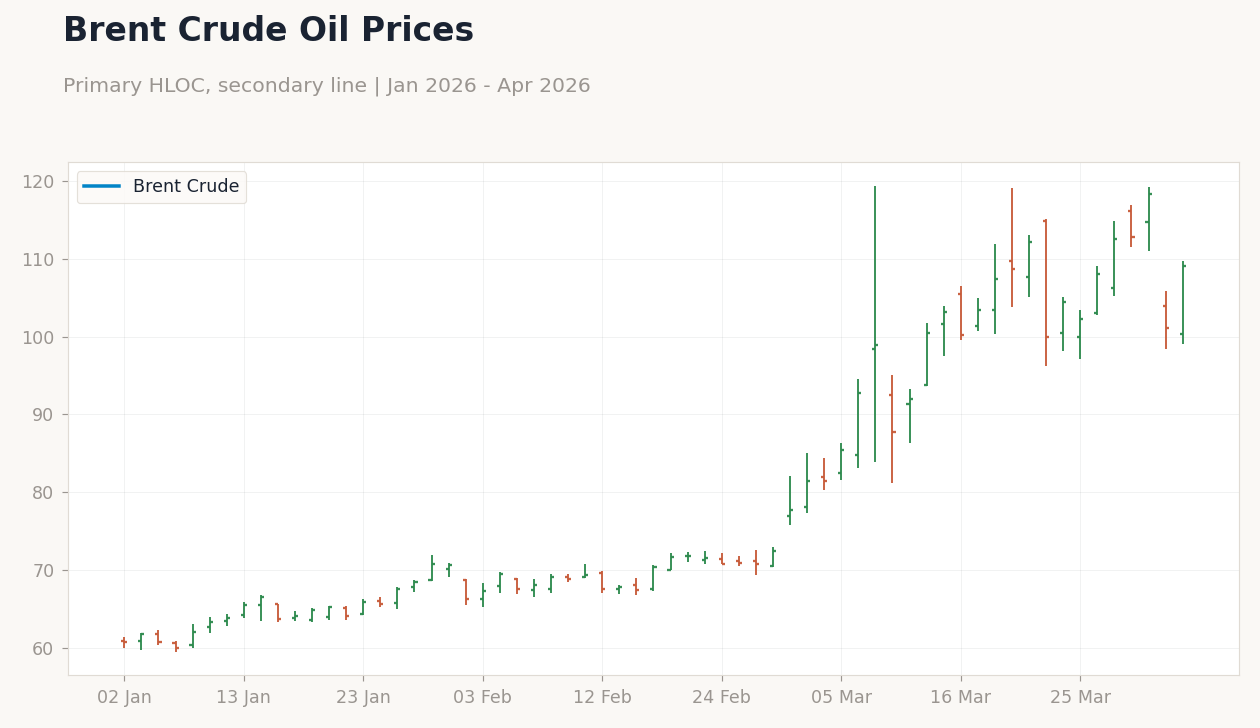

| Brent Crude | 109.05 | +7.80% |

| Gold | 4,702.70 | -1.68% |

| Bitcoin | 66,837.72 | -1.82% |

| India Short-term Rate | 5.50% | +0.00% |

| India Long-term Rate | - | - |

Prior Economic Events

| Data | Prior | Cons | Actual |

|---|---|---|---|

| Industrial Production Year-over-Year | 5.10 | 4.20 | 5.20 |

| Manufacturing Production Year-over-Year | 5.30 | - | 6 |

RBI Policy Rate Context | Type: macro_line | Short-term Rate %: 5.5 (2026-02-01) | Range: 4.25–6.75 | Trend(5pt): 4.25,5.15,6.75,6.75,5.5

RBI Policy Rate Context | Type: macro_line | Short-term Rate %: 5.5 (2026-02-01) | Range: 4.25–6.75 | Trend(5pt): 4.25,5.15,6.75,6.75,5.5

Today's Economic Events

| Data | Prior | Cons | Time |

|---|---|---|---|

| No events available | |||

- RBI tightens non-deliverable FX rules to curb speculation, arresting rupee's fall amid offshore market disruptions.

- Manufacturing PMI slips to 53.9 in March, signaling weakest growth in nearly four years due to cost pressures and global tensions.

- Equities rebound with Nifty up 1.56% and Sensex 1.65%, driven by value buying and rupee recovery.

Yesterday's Recap

India's industrial production grew 5.2% year-over-year in the latest release, beating consensus of 4.2% and edging up from the previous 5.1%, reflecting resilient factory output despite global headwinds. Manufacturing production accelerated to 6% year-over-year, surpassing the prior 5.3% and indicating strength in key sectors like petrochemicals following the government's abolition of import taxes. Equity markets rallied, with the Nifty 50 closing at 22,679.40 after a 1.56% gain, fueled by strong performances in banking and energy stocks such as HDFC Bank (+2.10% to 746.90) and Reliance (+1.93% to 1,369.90).

The Sensex advanced 1.65% to 73,134.32, supported by value buying amid rupee stabilization news. Currency markets saw USD/INR rise 0.33% to 92.94, though intraday reports highlighted a 173-paise rupee rally following RBI's FX curbs. EUR/INR declined 0.62% to 107.30, reflecting euro weakness.

Commodities mixed, with Brent crude surging 7.80% to 109.05 on supply fears, while gold fell 1.68% to 4,702.70 and Bitcoin dropped 1.82% to 66,837.72. India short-term rate held steady at 5.50%.

The Day Ahead

No major economic data releases are scheduled for today, providing markets a breather after yesterday's volatility. Attention turns to potential RBI commentary on recent FX measures, which could influence rupee dynamics. Tomorrow also lacks key events, though broader focus remains on upcoming RBI MPC decisions amid war-rattled markets.

Traders will monitor global cues, including any US data spillover, for directional signals on Indian assets. Equity sentiment may hinge on corporate earnings previews, particularly in IT services. Overall, low event risk suggests consolidation in Nifty and Sensex levels.

Other Economic Notes

India's manufacturing sector faces headwinds from fierce competition and West Asia conflicts, as evidenced by the PMI drop to 53.9, potentially pressuring growth trajectory. The government's move to end import taxes on petrochemicals aims to bolster local industries in plastics and pharmaceuticals, enhancing self-reliance. Emerging market rankings show India climbing to second spot in February on domestic momentum, underscoring resilience despite rupee challenges.

(cont...)