India Macro Daily(Beta Mode)

RBI Eases Rupee Curbs

Market Snapshot

| Asset | Level | Change |

|---|---|---|

| Nifty 50 | 24,374.55 | +0.04% |

| Sensex | 78,520.30 | +0.03% |

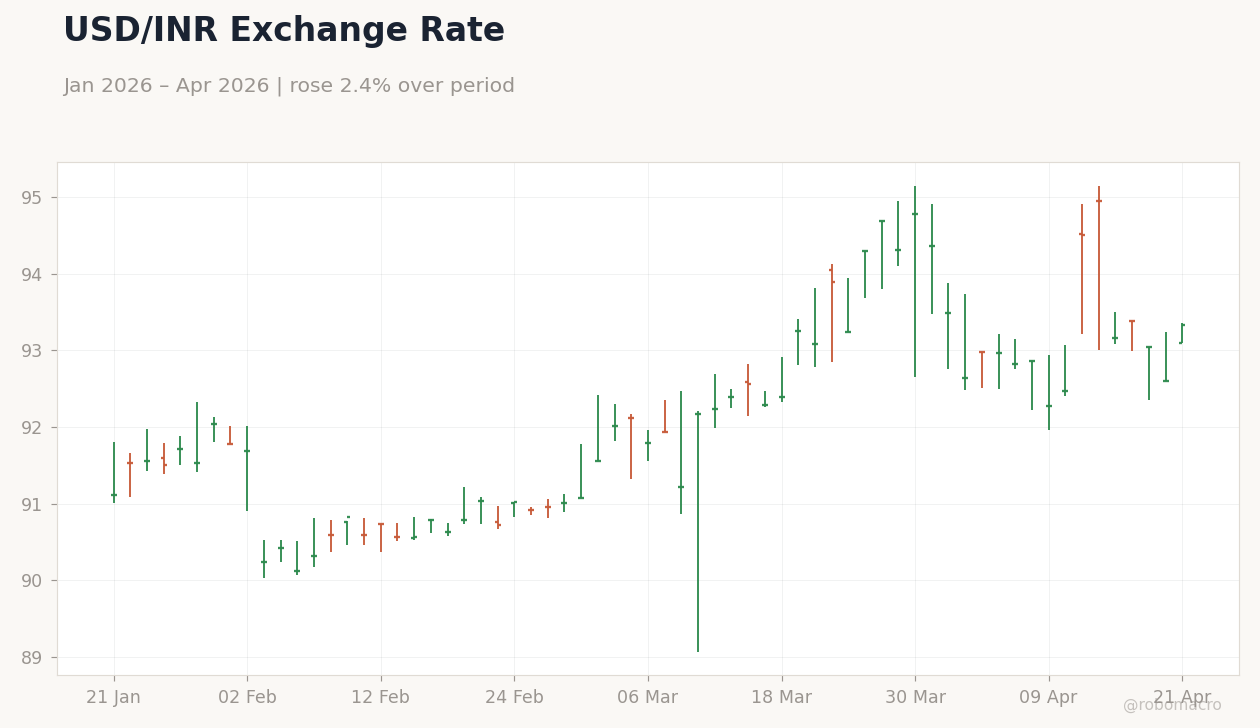

| USD/INR | 93.34 | +0.80% |

| EUR/INR | 109.89 | +0.55% |

| Reliance | 1,365.00 | +1.62% |

| HDFC Bank | 799.90 | +0.56% |

| Brent Crude | 94.94 | +5.05% |

| Gold | 4,817.30 | -0.83% |

| Bitcoin | 75,576.27 | +2.33% |

| India Short-term Rate | 5.50% | +0.00% |

| India Long-term Rate | - | - |

Prior Economic Events

| Data | Prior | Cons | Actual |

|---|---|---|---|

| No events available | |||

India Short-Term Interest Rates | Type: macro_line | Short-Term Rate (%): 5.5 (2026-02-01) | Range: 4.25–6.75 | Trend(5pt): 4.25,5.15,6.75,6.75,5.5

India Short-Term Interest Rates | Type: macro_line | Short-Term Rate (%): 5.5 (2026-02-01) | Range: 4.25–6.75 | Trend(5pt): 4.25,5.15,6.75,6.75,5.5

Today's Economic Events

| Data | Prior | Cons | Time |

|---|---|---|---|

| Wednesday (2026-04-22) | |||

| Monetary Policy Meeting Minutes | - | - | 03:30 |

| Thursday (2026-04-23) | |||

| HSBC Composite PMI Flash | 57 | - | 21:00 |

| HSBC Manufacturing PMI Flash | 53.90 | - | 21:00 |

| HSBC Services PMI Flash | 57.50 | - | 21:00 |

- RBI partially rolls back restrictions on rupee derivative trades, allowing non-deliverable derivatives with related-party limits to curb speculation.

- India's forex reserves climb $3.82 billion to $700.9 billion, bolstered by RBI interventions amid rupee pressures.

- Equity markets edge higher with Nifty 50 up 0.04% and Sensex up 0.03%, while USD/INR rises 0.80% on global dollar strength.

Yesterday's Recap

Indian markets showed modest gains yesterday amid limited data releases, with the Nifty 50 closing at 24,374.55 after a 0.04% increase, driven by selective buying in key stocks like Reliance Industries, which rose 1.62% to 1,365.00. The Sensex advanced 0.03% to 78,520.30, supported by banking shares such as HDFC Bank, up 0.56% to 799.90, though broader sentiment remained cautious due to rupee volatility. USD/INR strengthened 0.80% to 93.34, reflecting RBI's recent interventions to stabilize the currency following forex reserve builds.

EUR/INR gained 0.55% to 109.89, tracking euro resilience against the dollar. Commodity influences were mixed, with Brent Crude surging 5.05% to 94.94 amid West Asia tensions, while Gold dipped 0.83% to 4,817.30 as safe-haven demand eased slightly. Bitcoin climbed 2.33% to 75,576.27, buoyed by global crypto optimism.

India's short-term rate held steady at 5.50%, aligning with the RBI repo rate, signaling no immediate liquidity shifts.

The Day Ahead

Upcoming events focus on key monetary and activity indicators, with the RBI's Monetary Policy Meeting Minutes scheduled for release on April 22 at 03:30 ET, providing insights into the committee's rationale for holding the repo rate at 5.50%. Later that day, HSBC Flash PMIs for Composite, Manufacturing, and Services will be out at 21:00 ET, with prior readings at 57.0, 53.9, and 57.5 respectively, offering early signals on Q2 economic momentum. These releases could influence market expectations for RBI's inflation targeting and growth outlook, particularly if PMI data indicates softening in services amid global headwinds.

No major events are slated for April 21, allowing markets to digest recent RBI measures on rupee trades. Investors will watch for any unscheduled RBI statements on liquidity management.

Other Economic Notes

Broader economic themes highlight India's push for regional integration, with officials advocating a swift energy hub in Sri Lanka to enhance bilateral ties and energy security. (cont...)