India Macro Daily(Beta Mode)

PMI Rebounds, Rupee Weakens

Market Snapshot

| Asset | Level | Change |

|---|---|---|

| Nifty 50 | 24,173.05 | -0.84% |

| Sensex | 77,664.00 | -1.09% |

| USD/INR | 93.80 | +0.19% |

| EUR/INR | 109.72 | +0.01% |

| Reliance | 1,353.20 | -0.65% |

| HDFC Bank | 793.50 | -0.80% |

| Brent Crude | 106.24 | +4.25% |

| Gold | 4,713.90 | -0.39% |

| Bitcoin | 78,473.39 | +0.35% |

| India Short-term Rate | 5.50% | +0.00% |

| India Long-term Rate | - | - |

Prior Economic Events

| Data | Prior | Cons | Actual |

|---|---|---|---|

| Monetary Policy Meeting Minutes | - | - | - |

| HSBC Composite PMI Flash | 57 | - | 58.30 |

| HSBC Manufacturing PMI Flash | 53.90 | - | 55.90 |

| HSBC Services PMI Flash | 57.50 | - | 57.90 |

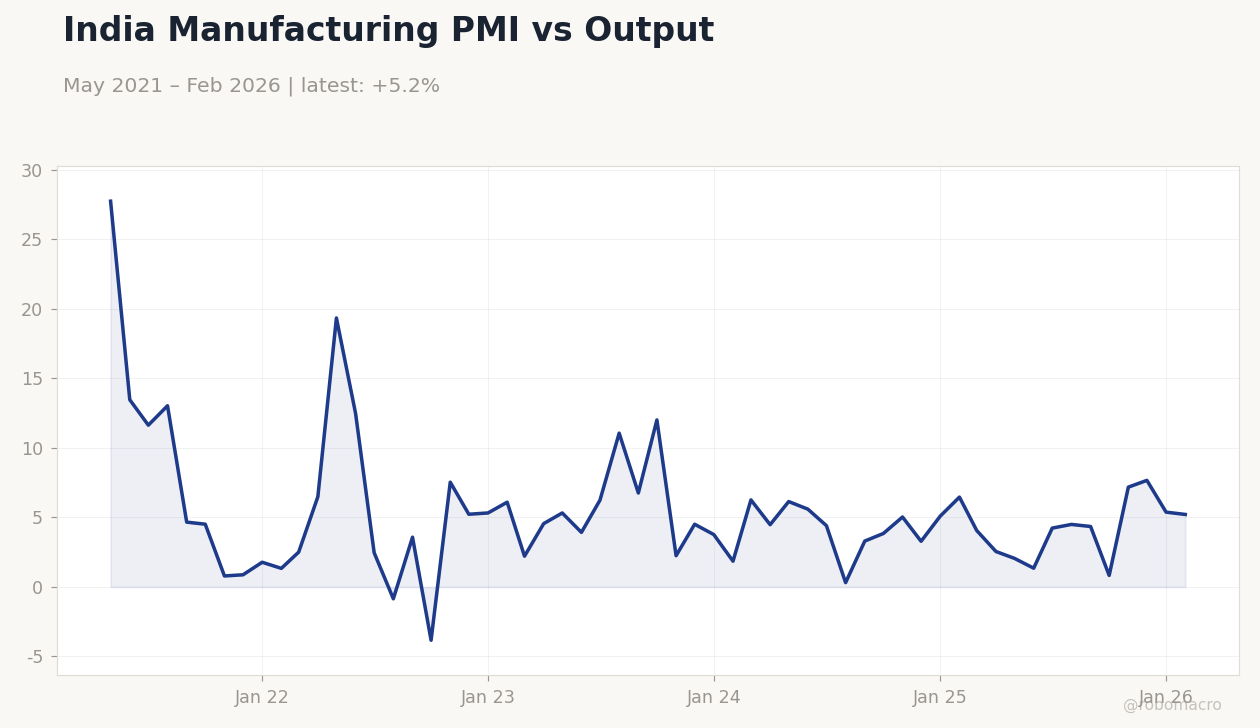

India Manufacturing PMI vs Output | Type: macro_line | Industrial Production YoY %: 5.21 (2026-02-01) | Range: -3.835–27.73 | Trend(6pt): 27.73,2.457,6.752,5.026,5.376,5.21

India Manufacturing PMI vs Output | Type: macro_line | Industrial Production YoY %: 5.21 (2026-02-01) | Range: -3.835–27.73 | Trend(6pt): 27.73,2.457,6.752,5.026,5.376,5.21

Today's Economic Events

| Data | Prior | Cons | Time |

|---|---|---|---|

| No events available | |||

- HSBC Flash PMIs showed accelerated private sector growth in April, with manufacturing and services beating expectations amid stronger output and job creation.

- Rupee depreciated to 93.80 against USD, pressured by oil price surges and West Asia tensions, while equities fell with Nifty 50 down 0.84%.

- RBI MPC minutes highlighted inflation risks from supply disruptions, Iran war impacts, and El Nino, maintaining repo rate at 5.50%.

Yesterday's Recap

India's HSBC Flash Composite PMI rose to 58.30 in April, surpassing the previous 57.0, driven by robust new orders and employment gains. Manufacturing PMI climbed to 55.9 from 53.9, reflecting faster output expansion, while Services PMI edged up to 57.9 from 57.5, indicating sustained momentum despite inflationary pressures. The RBI released Monetary Policy Meeting Minutes, emphasizing vigilance on supply-side disruptions and geopolitical risks without altering the repo rate stance.

Equity markets declined, with Nifty 50 closing at 24,173.05 after a 0.84% drop, led by losses in financials and energy stocks. Sensex fell 1.09% to 77,664.00, as Reliance Industries dropped 0.65% to 1,353.20 and HDFC Bank slid 0.80% to 793.50. USD/INR strengthened to 93.80 with a 0.19% gain, fueled by Brent Crude's 4.25% surge to 106.24 amid oil supply concerns.

Gold dipped 0.39% to 4,713.90, while Bitcoin rose 0.35% to 78,473.39, showing mixed safe-haven flows.

The Day Ahead

Today features no major economic releases or events in India, providing a breather after yesterday's PMI data and RBI minutes. Markets may focus on digesting global cues, including any spillover from West Asia tensions affecting oil prices and rupee stability. Attention could shift to corporate earnings, with potential volatility in banking and IT sectors amid ongoing deposit and growth concerns.

Tomorrow also lacks scheduled data, likely keeping trading volumes subdued unless unexpected news emerges. Investors should monitor forex interventions by RBI to curb rupee depreciation. Overall, the quiet calendar underscores a consolidation phase for Indian assets.

Other Economic Notes

IMF upgraded India's GDP forecast to 7.6% for the year, citing resilience despite global risks, though a weaker rupee has positioned India as the 6th largest economy in nominal terms. Wheat export resumption aims to manage surplus stocks and support farmer incomes, potentially easing domestic price pressures. Broader growth faces tests from supply disruptions and currency volatility, with economists warning of risks to food and fuel affordability if rupee hits 95 against USD.