India Macro Daily(Beta Mode)

Rupee Hits Record Low on Oil Shock

Market Snapshot

| Asset | Level | Change |

|---|---|---|

| Nifty 50 | 23,618.00 | -0.14% |

| Sensex | 75,200.85 | -0.15% |

| USD/INR | 96.27 | +0.31% |

| EUR/INR | 112.23 | +0.78% |

| Reliance | 1,338.00 | +0.16% |

| HDFC Bank | 767.80 | -0.11% |

| Brent Crude | 110.89 | -1.08% |

| Gold | 4,507.90 | -0.98% |

| Bitcoin | 76,682.40 | -0.35% |

| India Short-term Rate | 5.50% | +0.00% |

| India Long-term Rate | - | - |

Prior Economic Events

| Data | Prior | Cons | Actual |

|---|---|---|---|

| No events available | |||

USD/INR Exchange Rate | Type: macro_line | INR per USD: 95.97 (2026-05-15) | Range: 72.42–95.97 | Trend(6pt): 72.82,79.66,83.22,86.82,95.69,95.97

USD/INR Exchange Rate | Type: macro_line | INR per USD: 95.97 (2026-05-15) | Range: 72.42–95.97 | Trend(6pt): 72.82,79.66,83.22,86.82,95.69,95.97

Today's Economic Events

| Data | Prior | Cons | Time |

|---|---|---|---|

| Thursday (2026-05-21) | |||

| HSBC Composite PMI Flash | 58.20 | - | 21:00 |

| HSBC Manufacturing PMI Flash | 54.70 | - | 21:00 |

| HSBC Services PMI Flash | 58.80 | - | 21:00 |

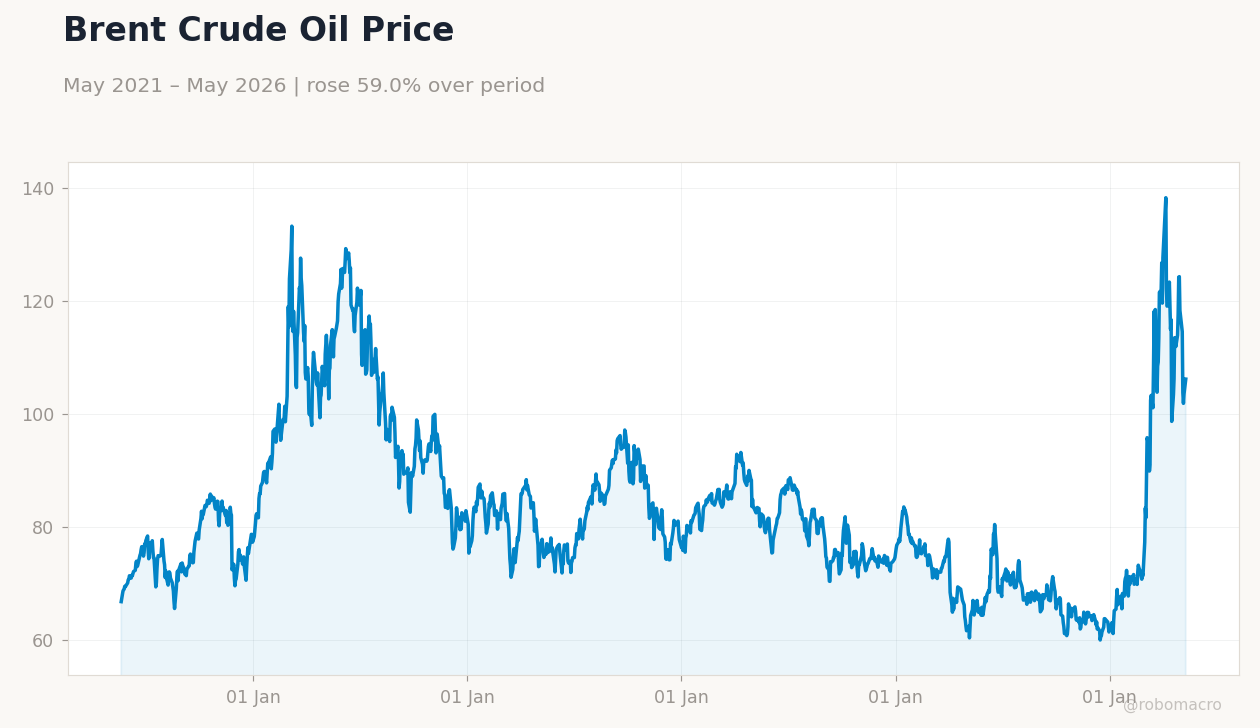

- Rupee falls to record 96.27 against USD as Brent crude holds near $111 amid Iran-related supply risks.

- Nifty 50 and Sensex close 0.14-0.15% lower while short-term rates stay anchored at 5.50%.

- HSBC flash PMI prints due tonight; markets watch for signs of sustained services momentum above 58.

Yesterday's Recap

Equity benchmarks ended modestly lower with Nifty at 23,618 and Sensex at 75,200.85 after profit-taking in banking and IT names. The rupee touched a fresh all-time low of 96.27, pressured by elevated Brent crude at 110.89 and widening current-account concerns. Reliance Industries gained 0.16% on resilient refining margins while HDFC Bank slipped 0.11%.

Gold fell 0.98% to 4,507.90 as risk appetite improved slightly. No major data releases occurred yesterday, leaving market focus on geopolitical oil headlines and RBI liquidity operations. India’s continued purchase of Russian crude irrespective of US sanctions provided some offset to price pressures.

The Day Ahead

Tonight’s HSBC Composite, Manufacturing and Services PMI flashes at 21:00 IST will set the tone for growth expectations. A print near prior levels of 58.2, 54.7 and 58.8 respectively would reinforce resilience in services. Traders will also monitor any RBI liquidity injection signals ahead of month-end.

Oil price volatility remains the dominant risk factor for both the rupee and inflation trajectory. No MPC speakers are scheduled.

Other Economic Notes

Government sources ruled out near-term capital-gains tax relief for FPIs, signalling continued focus on forex conservation. Rising biodiesel mandates in Indonesia and Malaysia are tightening palm-oil supplies and could lift India’s import bill. State fuel retailers have passed on modest price hikes twice in a week to offset crude costs.

Dividend windfalls and strong tax collections continue to buffer the fiscal position against external shocks.

Global Macro News

Surging oil prices linked to Iran conflict dominate global sentiment and directly widen India’s trade deficit. Brent’s move above 110 has pushed the rupee to successive record lows and raised imported inflation risks. Central banks elsewhere face similar energy-driven price pressures, limiting coordinated policy support.

Safe-haven flows into gold have eased while Bitcoin trades softer near 76,682. <i>↓ p.2</i>