India Macro Daily(Beta Mode)

Rupee Hits Record Low as RBI Unveils $5bn Swap

Market Snapshot

| Asset | Level | Change |

|---|---|---|

| Nifty 50 | 23,618.00 | -0.14% |

| Sensex | 75,200.85 | -0.15% |

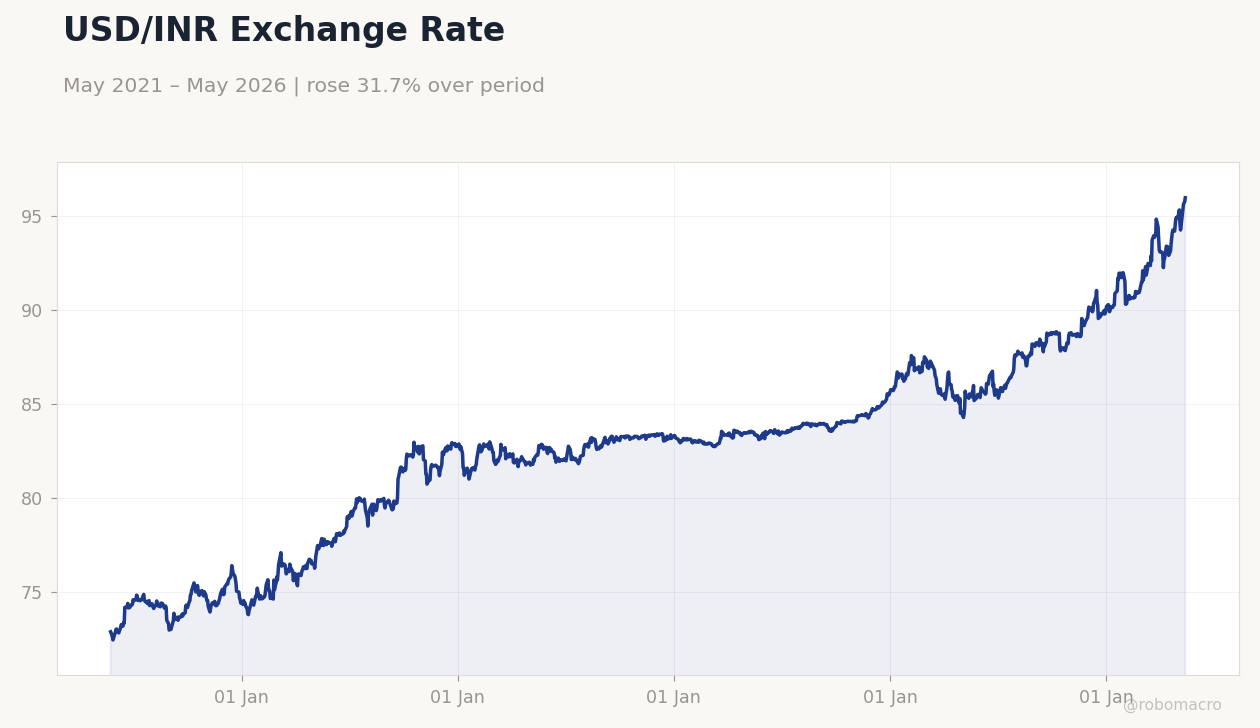

| USD/INR | 96.57 | +0.31% |

| EUR/INR | 111.99 | -0.21% |

| Reliance | 1,359.70 | +2.80% |

| HDFC Bank | 759.50 | -0.39% |

| Brent Crude | 106.26 | -4.51% |

| Gold | 4,546.30 | +0.89% |

| Bitcoin | 77,654.98 | +1.18% |

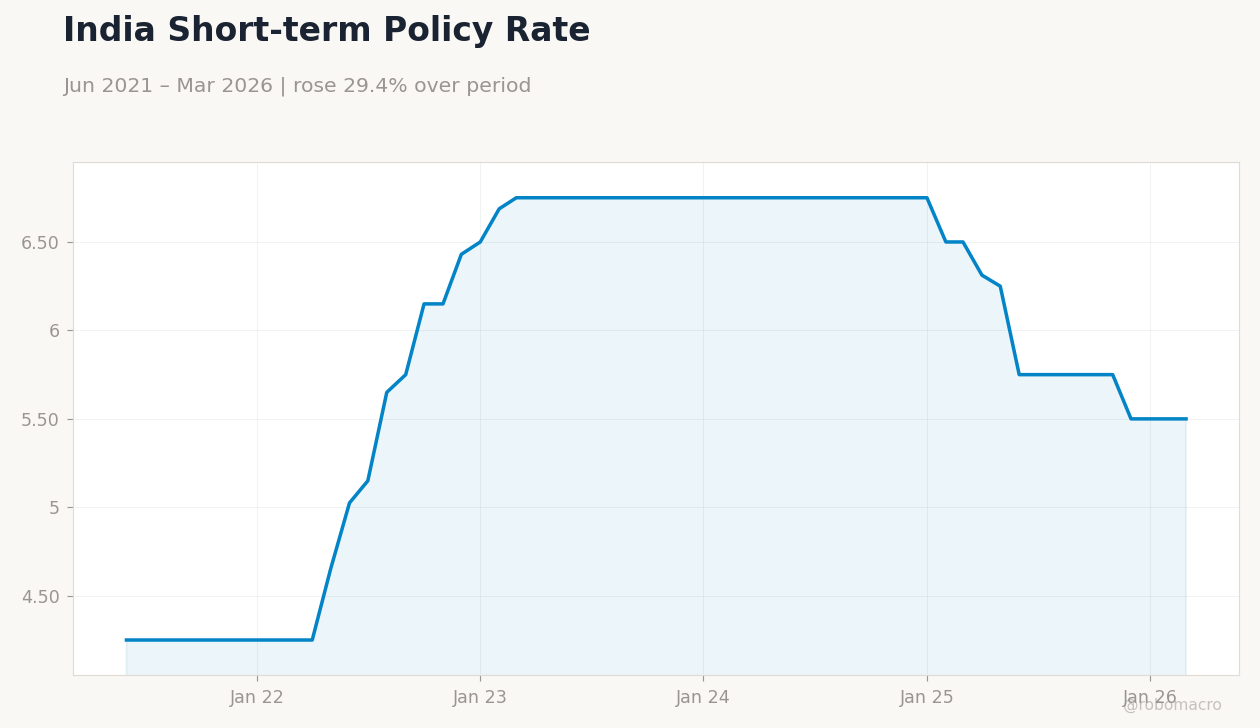

| India Short-term Rate | 5.50% | +0.00% |

| India Long-term Rate | - | - |

Prior Economic Events

| Data | Prior | Cons | Actual |

|---|---|---|---|

| No events available | |||

USD/INR Exchange Rate | Type: macro_line | USD/INR: 95.97 (2026-05-15) | Range: 72.42–95.97 | Trend(6pt): 72.86,79.89,83.25,86.96,95.76,95.97

USD/INR Exchange Rate | Type: macro_line | USD/INR: 95.97 (2026-05-15) | Range: 72.42–95.97 | Trend(6pt): 72.86,79.89,83.25,86.96,95.76,95.97

Today's Economic Events

| Data | Prior | Cons | Time |

|---|---|---|---|

| Thursday (2026-05-21) | |||

| HSBC Composite PMI Flash | 58.20 | - | 21:00 |

| HSBC Manufacturing PMI Flash | 54.70 | - | 21:00 |

| HSBC Services PMI Flash | 58.80 | - | 21:00 |

- Rupee weakens to record low near 97 amid elevated oil prices and global pressures

- Nifty 50 falls 0.14% to 23,618 while Sensex declines 0.15% to 75,200.85

- RBI announces $5 billion dollar-rupee swap to inject liquidity and support FX stability

Yesterday's Recap

Indian equity markets closed modestly lower with Nifty 50 at 23,618.00, down 0.14%, and Sensex at 75,200.85, off 0.15%. The rupee depreciated 0.31% to 96.57 against the dollar, extending its slide toward record lows near 97. Brent crude dropped 4.51% to 106.26 per barrel, easing some imported inflation risks despite ongoing geopolitical strains.

Gold rose 0.89% to 4,546.30 per ounce as investors sought safe havens. Reliance gained 2.80% to 1,359.70 on stronger margins while HDFC Bank slipped 0.39%. Short-term rates held steady at 5.50%.

No major data releases occurred yesterday, leaving market focus on RBI liquidity measures and external volatility.

The Day Ahead

HSBC Composite PMI Flash, Manufacturing PMI Flash and Services PMI Flash are scheduled for release at 21:00 today, with prior prints at 58.2, 54.7 and 58.8 respectively. Traders will assess whether momentum in services and manufacturing remains intact amid global headwinds. April merchandise trade data and weekly forex reserves will also be monitored for signs of external sector stress.

The RBI’s quarterly State of the Economy bulletin is expected to reinforce resilience narratives. No MPC member speeches are listed, keeping attention on the newly announced swap operation.

Other Economic Notes

The RBI bulletin highlighted India’s economic resilience despite global volatility, citing steady domestic demand and contained inflation risks. Oxford Economics flagged a worsening inflation outlook driven by persistent oil shocks. State-owned fuel retailers raised petrol and diesel prices for the second time in a week to offset higher crude costs.

FDI equity inflows reached solid levels in recent months, supporting manufacturing and renewables. Monsoon progress remains on track, limiting near-term food price upside.

Global Macro News

Elevated oil prices stemming from Iran-related tensions continue to pressure India’s current account and currency. Global risk sentiment improved modestly, aiding equity recovery even as the rupee tumbled. <i>↓ p.2</i>