India Macro Daily(Beta Mode)

Rupee Rally Extends on RBI Signals

Market Snapshot

| Asset | Level | Change |

|---|---|---|

| Nifty 50 | 24,031.70 | +1.32% |

| Sensex | 76,488.96 | +1.42% |

| USD/INR | 95.22 | -0.52% |

| EUR/INR | 110.85 | -0.49% |

| Reliance | 1,354.50 | +0.36% |

| HDFC Bank | 766.80 | +1.01% |

| Brent Crude | 94.99 | -8.26% |

| Gold | 4,546.10 | +0.56% |

| Bitcoin | 77,053.81 | +0.09% |

| India Short-term Rate | 5.50% | +0.00% |

| India Long-term Rate | - | - |

Prior Economic Events

| Data | Prior | Cons | Actual |

|---|---|---|---|

| No events available | |||

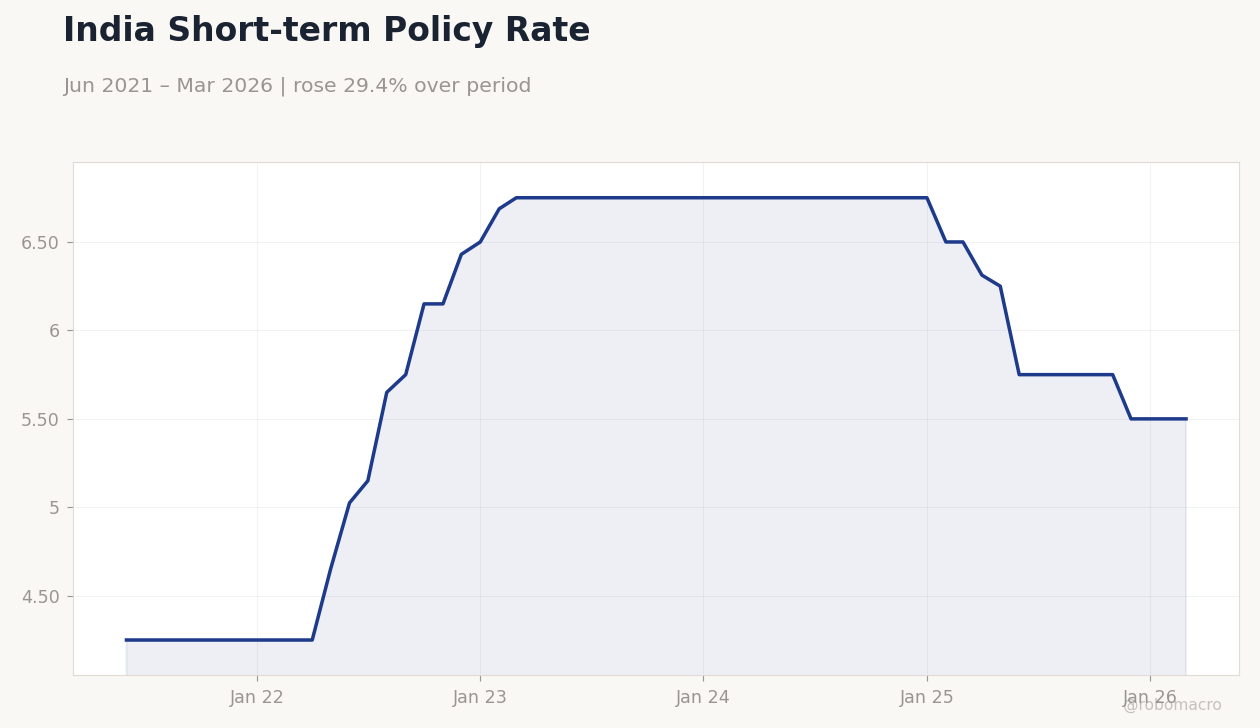

India Short-term Policy Rate | Type: macro_line | Policy Rate %: 5.5 (2026-03-01) | Range: 4.25–6.75 | Trend(5pt): 4.25,5.65,6.75,6.75,5.5

India Short-term Policy Rate | Type: macro_line | Policy Rate %: 5.5 (2026-03-01) | Range: 4.25–6.75 | Trend(5pt): 4.25,5.65,6.75,6.75,5.5

Today's Economic Events

| Data | Prior | Cons | Time |

|---|---|---|---|

| No events available | |||

- Nifty 50 rose 1.32% to 24,031.70 while Sensex gained 1.42% to 76,488.96 as the rupee strengthened.

- USD/INR fell 0.52% to 95.22 after RBI Governor Malhotra signaled further intervention readiness.

- Brent crude dropped 8.26% to 94.99, easing imported inflation pressures for Indian markets.

Yesterday's Recap

Indian equity benchmarks posted solid gains with Nifty 50 closing at 24,031.70 and Sensex at 76,488.96. The rupee extended its rally, with USD/INR settling at 95.22 and EUR/INR at 110.85. Brent crude’s sharp decline to 94.99 supported sentiment by lowering energy import costs.

Reliance and HDFC Bank advanced modestly while gold edged higher to 4,546.10. No major data releases occurred, leaving market moves driven by RBI communications and global oil prices. Short-term rates held steady at 5.50%.

The absence of fresh economic prints kept focus on currency intervention signals.

The Day Ahead

Markets enter a data-light session with no scheduled releases from official sources. Attention will center on any follow-up comments from RBI officials regarding rupee management. Equity traders will monitor Reliance and banking stocks for continuation of recent momentum.

Currency desks expect sustained intervention rhetoric to influence USD/INR flows. Global oil price updates remain the key external variable for Indian inflation expectations. Bond markets are likely to stay range-bound absent new liquidity signals.

Other Economic Notes

India’s fuel retailers raised petrol and diesel prices for the fourth time in ten days amid Middle East supply strains. IT export growth and manufacturing FDI inflows continue to underpin the medium-term growth outlook. Monsoon arrival on schedule supports rural demand and food price moderation.

The repo rate remains at 5.50%, anchoring short-term borrowing costs. Equity positioning reflects modest bullish bias on the rupee and lower crude.

Global Macro News

US Fed minutes showed no shift in the dot plot, limiting external pressure on emerging-market currencies. OPEC+ supply signals contributed to Brent’s steep decline, benefiting India’s terms of trade. Global risk appetite stayed constructive, supporting equity inflows into Indian markets.

<i>↓ p.2</i>