India Macro Daily(Beta Mode)

Rupee Firms on RBI Swap Amid Equity Slide

Market Snapshot

| Asset | Level | Change |

|---|---|---|

| Nifty 50 | 23,913.70 | -0.49% |

| Sensex | 76,009.70 | -0.63% |

| USD/INR | 95.25 | -0.49% |

| EUR/INR | 110.75 | -0.58% |

| Reliance | 1,356.30 | -0.78% |

| HDFC Bank | 778.90 | -1.01% |

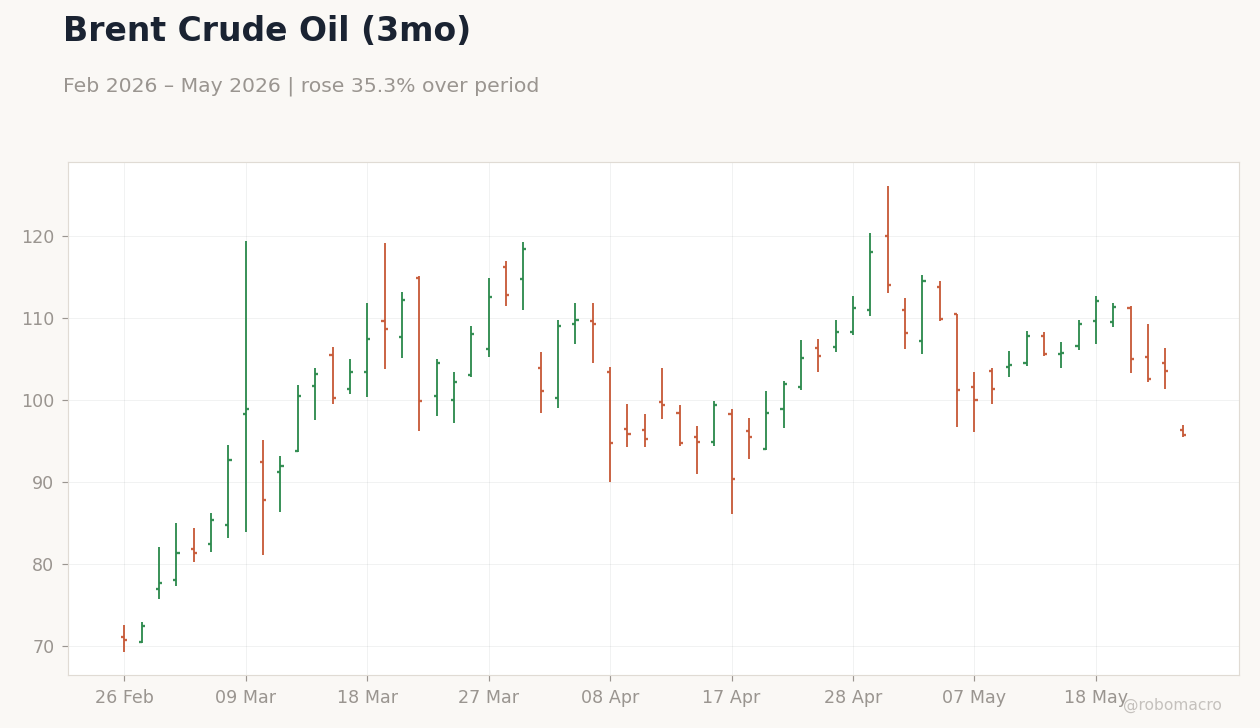

| Brent Crude | 95.86 | -7.42% |

| Gold | 4,509.10 | -0.26% |

| Bitcoin | 75,763.42 | -1.96% |

| India Short-term Rate | 5.50% | +0.00% |

| India Long-term Rate | - | - |

Prior Economic Events

| Data | Prior | Cons | Actual |

|---|---|---|---|

| No events available | |||

India Short-term Policy Rate | Type: macro_line | Policy Rate %: 5.5 (2026-03-01) | Range: 4.25–6.75 | Trend(5pt): 4.25,5.65,6.75,6.75,5.5

India Short-term Policy Rate | Type: macro_line | Policy Rate %: 5.5 (2026-03-01) | Range: 4.25–6.75 | Trend(5pt): 4.25,5.65,6.75,6.75,5.5

Today's Economic Events

| Data | Prior | Cons | Time |

|---|---|---|---|

| No events available | |||

- Nifty 50 slips 0.49% to 23,913.70 while Sensex falls 0.63% to 76,009.70 amid broad equity weakness.

- USD/INR drops to 95.25 as rupee strengthens for a second session on RBI dollar-rupee swap operations.

- Brent crude plunges 7.42% to $95.86, easing imported inflation pressures even as fuel retailers raise petrol and diesel prices for the fourth time in ten days.

Yesterday's Recap

Indian equities closed lower with Nifty and Sensex declining on profit-taking in banking and energy names after Reliance and HDFC Bank posted losses of 0.78% and 1.01%. The rupee firmed to 95.25 against the dollar as the RBI’s dollar-rupee swap attracted nearly double the usual bids, signaling official comfort with gradual appreciation. State-run oil companies raised retail fuel prices again, passing on part of the recent Middle East supply strain despite the sharp drop in global crude.

Market participants also digested the earlier transfer of ₹2.87 lakh crore in RBI surplus to the government, which is expected to support fiscal spending without immediate liquidity injection. Short-term rates remained anchored at 5.50% with no change in the policy corridor.

The Day Ahead

With the economic calendar empty, markets will focus on follow-through in the rupee after the successful RBI swap. Traders will monitor oil marketing company announcements for any further retail price adjustments. Global cues from US Treasury yields and Asian equity opens will set the tone for Nifty and Sensex.

Corporate results from the IT sector may provide incremental color on export demand. Liquidity conditions will be watched for any RBI fine-tuning operations ahead of month-end.

Other Economic Notes

Persistent rupee volatility continues to highlight India’s structural dependence on imported energy, with recent price hikes underscoring the pass-through to domestic inflation. Economists note that reviving private corporate investment remains essential to sustain growth momentum above 6.5%. The RBI’s willingness to allow two-way rupee movement, as endorsed by former CEA Montek Singh Ahluwalia, reduces the risk of one-sided reserve depletion.

Heatwave-related disruptions in northern states may weigh on Q1 industrial output, though services activity shows resilience.