India Macro Daily(Beta Mode)

Rupee Firms as RBI Intervenes, Oil Drops

Market Snapshot

| Asset | Level | Change |

|---|---|---|

| Nifty 50 | 23,907.15 | -0.03% |

| Sensex | 75,867.80 | -0.19% |

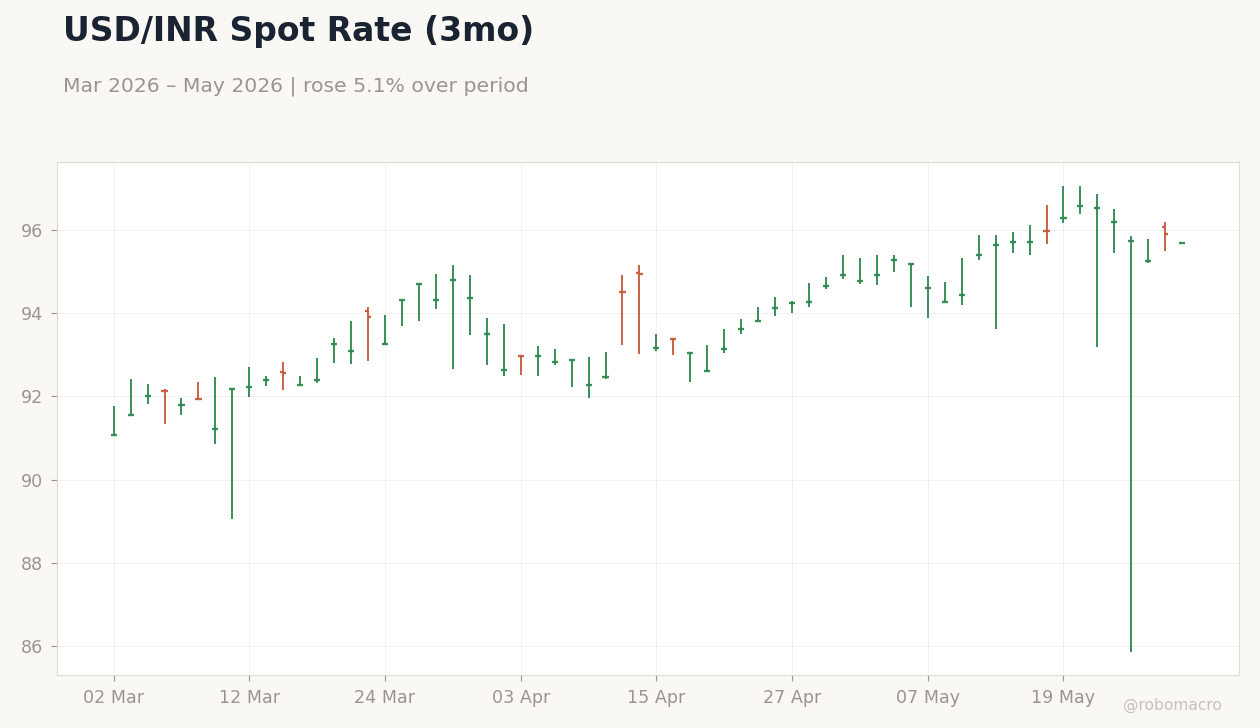

| USD/INR | 95.68 | -0.23% |

| EUR/INR | 111.23 | -0.06% |

| Reliance | 1,350.50 | -0.43% |

| HDFC Bank | 758.65 | -2.60% |

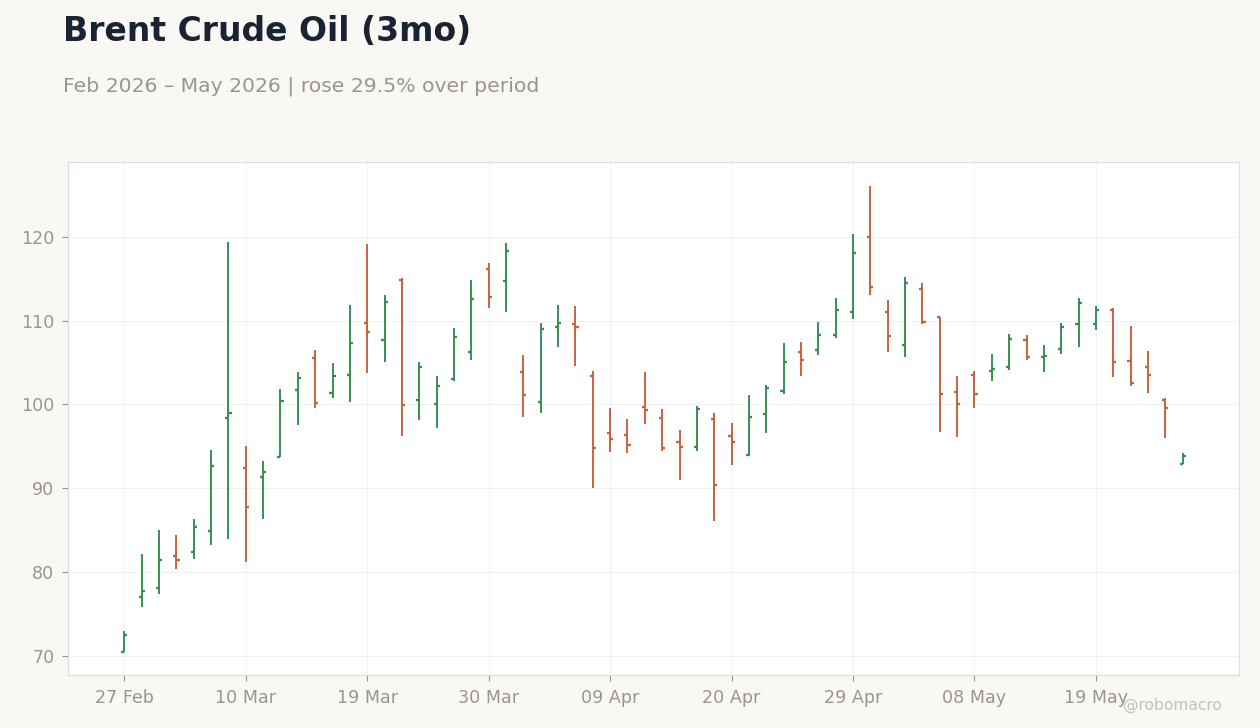

| Brent Crude | 94.19 | -5.41% |

| Gold | 4,484.80 | -0.35% |

| Bitcoin | 74,436.75 | -1.83% |

| India Short-term Rate | 5.50% | +0.00% |

| India Long-term Rate | - | - |

Prior Economic Events

| Data | Prior | Cons | Actual |

|---|---|---|---|

| No events available | |||

India Short-term Policy Rate | Type: macro_line | Policy Rate %: 5.5 (2026-03-01) | Range: 4.25–6.75 | Trend(5pt): 4.25,5.65,6.75,6.75,5.5

India Short-term Policy Rate | Type: macro_line | Policy Rate %: 5.5 (2026-03-01) | Range: 4.25–6.75 | Trend(5pt): 4.25,5.65,6.75,6.75,5.5

Today's Economic Events

| Data | Prior | Cons | Time |

|---|---|---|---|

| No events available | |||

- Nifty 50 edged down 0.03% to 23,907.15 while Sensex fell 0.19% to 75,867.80 amid thin volumes and selective selling in banks.

- USD/INR declined 0.23% to 95.68 as RBI stepped up dollar sales and a swap auction drew nearly double the bids offered.

- Brent crude plunged 5.41% to $94.19, easing imported inflation risks and supporting the rupee’s two-week high.

Yesterday's Recap

Indian equities closed nearly flat after a muted session driven by profit-taking in private banks. HDFC Bank dropped 2.60% while Reliance slipped 0.43%, weighing on the benchmarks. The rupee strengthened to 95.68 against the dollar as the central bank conducted aggressive spot interventions and a dollar-rupee swap that attracted heavy participation.

Brent’s sharp decline reduced pressure on the current account and import bill. Gold fell 0.35% to 4,484.80 and Bitcoin declined 1.83%, reflecting broader risk-off sentiment. Short-term rates stayed anchored at 5.50% with no change in liquidity conditions reported.

Market participants focused on RBI’s repeated signals that it would act to curb excessive rupee volatility.

The Day Ahead

No major data releases are scheduled for 27 May, leaving markets to track global oil prices and any further RBI liquidity operations. Traders will watch USD/INR moves closely after yesterday’s intervention-heavy session. Corporate results from mid-sized IT firms may provide incremental color on export demand.

GIFT Nifty points to a muted open following overnight weakness in U.S. indices. Bond desks await any fresh clues on RBI’s bond-buyback calendar.

Other Economic Notes

The larger-than-expected RBI dividend of ₹2.87 lakh crore improves the central government’s fiscal headroom but narrows the space for additional spending without breaching deficit targets. Economists note that rupee weakness has exposed India’s structural energy dependence and the need to revive corporate capex. Services exports remain the key buffer for the current account, yet softening global IT spending poses downside risks.

Corporate investment intentions have yet to show a sustained pickup despite improving capacity utilization readings.

Global Macro News

Global risk sentiment stayed cautious after mixed U.S. data and renewed worries over trade tariffs. Asian currencies traded mixed, with the Indian rupee outperforming peers on local intervention.

<i>↓ p.2</i>