India Macro Daily(Beta Mode)

Forex Reserves Fall to One-Year Low, Stocks Drop

Market Snapshot

| Asset | Level | Change |

|---|---|---|

| Nifty 50 | 23,547.75 | -1.50% |

| Sensex | 74,775.74 | -1.44% |

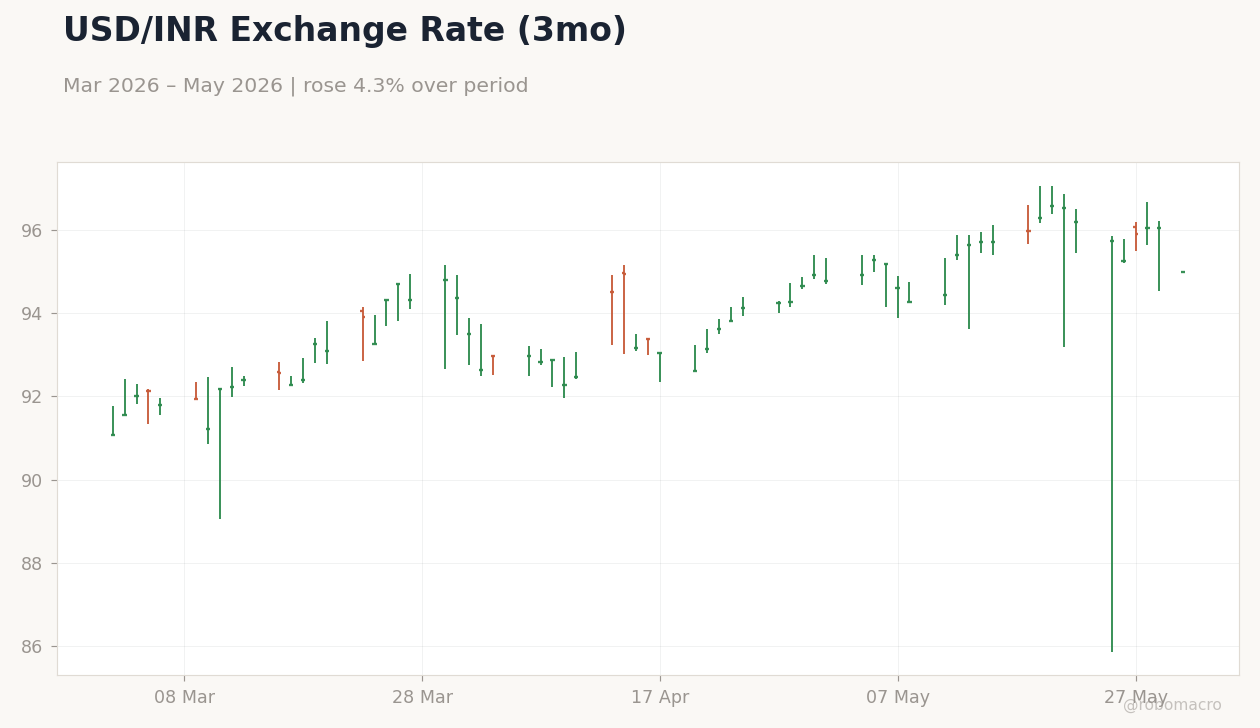

| USD/INR | 94.99 | -1.10% |

| EUR/INR | 110.74 | -0.61% |

| Reliance | 1,321.20 | -2.17% |

| HDFC Bank | 744.55 | -1.86% |

| Brent Crude | 93.35 | +1.41% |

| Gold | 4,569.00 | +0.19% |

| Bitcoin | 73,900.00 | +0.20% |

| India Short-term Rate | 5.50% | +0.00% |

| India Long-term Rate | - | - |

Prior Economic Events

| Data | Prior | Cons | Actual |

|---|---|---|---|

| No events available | |||

India Industrial Production YoY | Type: macro_line | YoY %: 3.911 (2026-03-01) | Range: -3.835–19.33 | Trend(5pt): 11.63,3.575,2.246,5.091,3.911

India Industrial Production YoY | Type: macro_line | YoY %: 3.911 (2026-03-01) | Range: -3.835–19.33 | Trend(5pt): 11.63,3.575,2.246,5.091,3.911

Today's Economic Events

| Data | Prior | Cons | Time |

|---|---|---|---|

| Monday (2026-06-01) | |||

| Industrial Production Year-over-Year | 4.10 | 3.80 | 06:30 |

| Manufacturing Production Year-over-Year | 4.30 | - | 06:30 |

| Friday (2026-06-05) | |||

| RBI Interest Rate Decision | 5.25 | 5.25 | 00:30 |

| GDP Growth Year-over-Year | 7.80 | 7.30 | 06:30 |

- India's forex reserves fell to $681.4 billion in the week ended May 22, the lowest level in over a year, as the RBI defended the rupee.

- Nifty 50 dropped 1.50% to 23,547.75 and Sensex fell 1.44% to 74,775.74, led by declines in Reliance and HDFC Bank.

- RBI reiterated that India remains the fastest-growing major economy despite global shocks and higher US tariffs.

Yesterday's Recap

Indian equity markets closed sharply lower on May 30 with Nifty 50 declining 1.50% to 23,547.75 and Sensex falling 1.44% to 74,775.74. Reliance Industries dropped 2.17% to 1,321.20 while HDFC Bank declined 1.86% to 744.55. The rupee strengthened modestly with USD/INR closing at 94.99, down 1.10%.

Brent crude rose 1.41% to 93.35 amid OPEC+ supply caution. No major data releases occurred on May 30. Gold edged up 0.19% to 4,569.00 while the short-term policy rate held steady at 5.50%.

Broader market breadth remained weak with limited buying interest in IT and banking sectors.

The Day Ahead

Industrial Production and Manufacturing Production data for April are scheduled for release on June 1 at 06:30 IST, with consensus forecasts pointing to a slowdown from prior prints. Markets will also monitor the RBI's June 5 interest rate decision, where consensus expects the repo rate to remain at 5.50%. GDP growth figures for Q4 FY26 are due the same day and are expected to show moderation from 7.8% to around 7.3%.

Traders will parse these releases for clues on consumption momentum and policy trajectory. OIS markets currently price limited rate cuts through year-end.

Other Economic Notes

The RBI's latest annual report highlights India's resilient growth path even as external risks from West Asia conflicts and US tariffs intensify. Forex reserve depletion reflects active rupee defense operations that have kept USD/INR volatility contained. The government scrapped cotton import duties for five months to support textile exporters facing supply shortages.

RBI commentary continues to stress the need for stronger corporate investment to sustain medium-term expansion. Services-led momentum remains the primary growth driver amid softening industrial indicators.