India Macro Daily(Beta Mode)

Forex Reserves Drop as RBI Eyes Rate Hold

Market Snapshot

| Asset | Level | Change |

|---|---|---|

| Nifty 50 | 23,547.75 | -1.50% |

| Sensex | 74,775.74 | -1.44% |

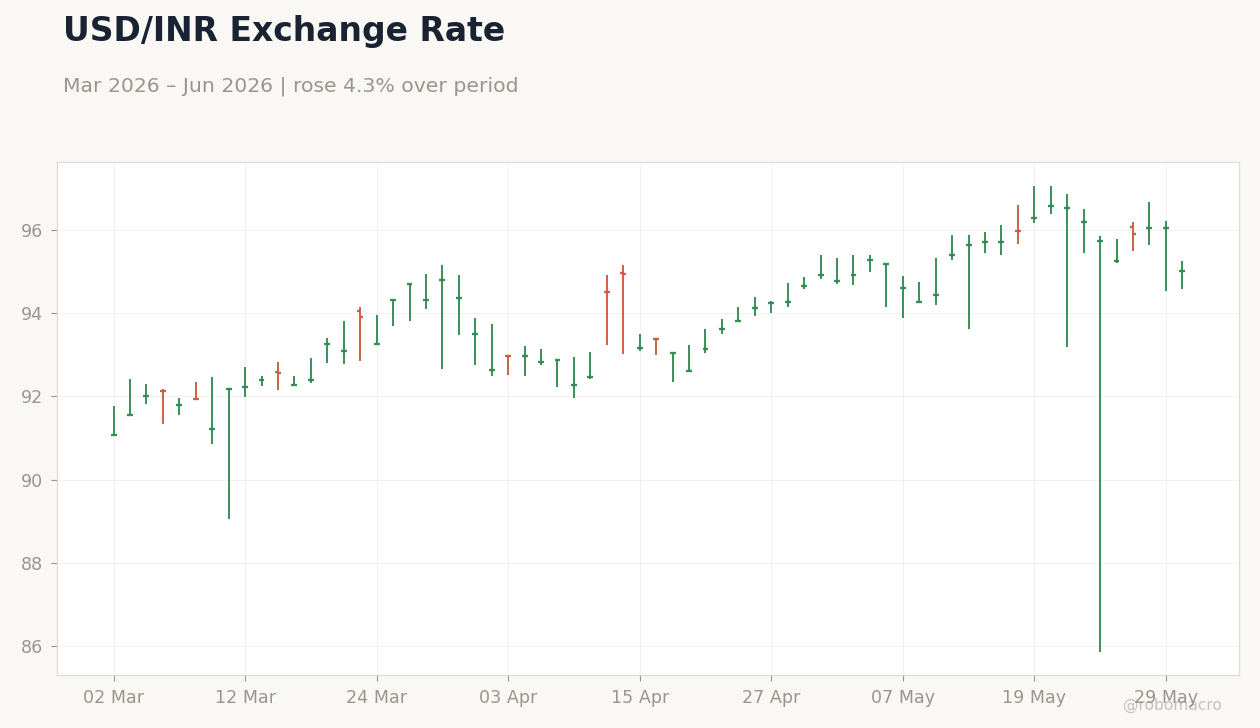

| USD/INR | 95.00 | -1.09% |

| EUR/INR | 110.71 | -0.65% |

| Reliance | 1,321.20 | -2.17% |

| HDFC Bank | 744.55 | -1.86% |

| Brent Crude | 94.93 | +3.13% |

| Gold | 4,515.10 | -1.00% |

| Bitcoin | 71,176.51 | -3.27% |

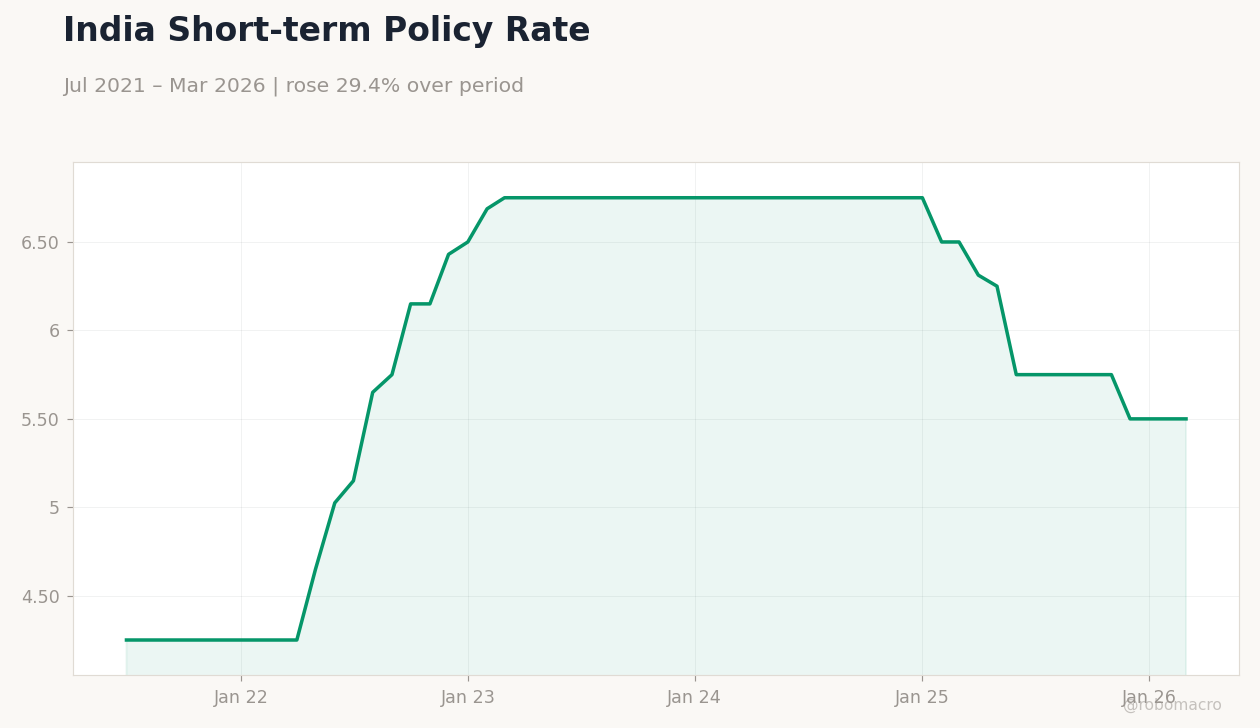

| India Short-term Rate | 5.50% | +0.00% |

| India Long-term Rate | - | - |

Prior Economic Events

| Data | Prior | Cons | Actual |

|---|---|---|---|

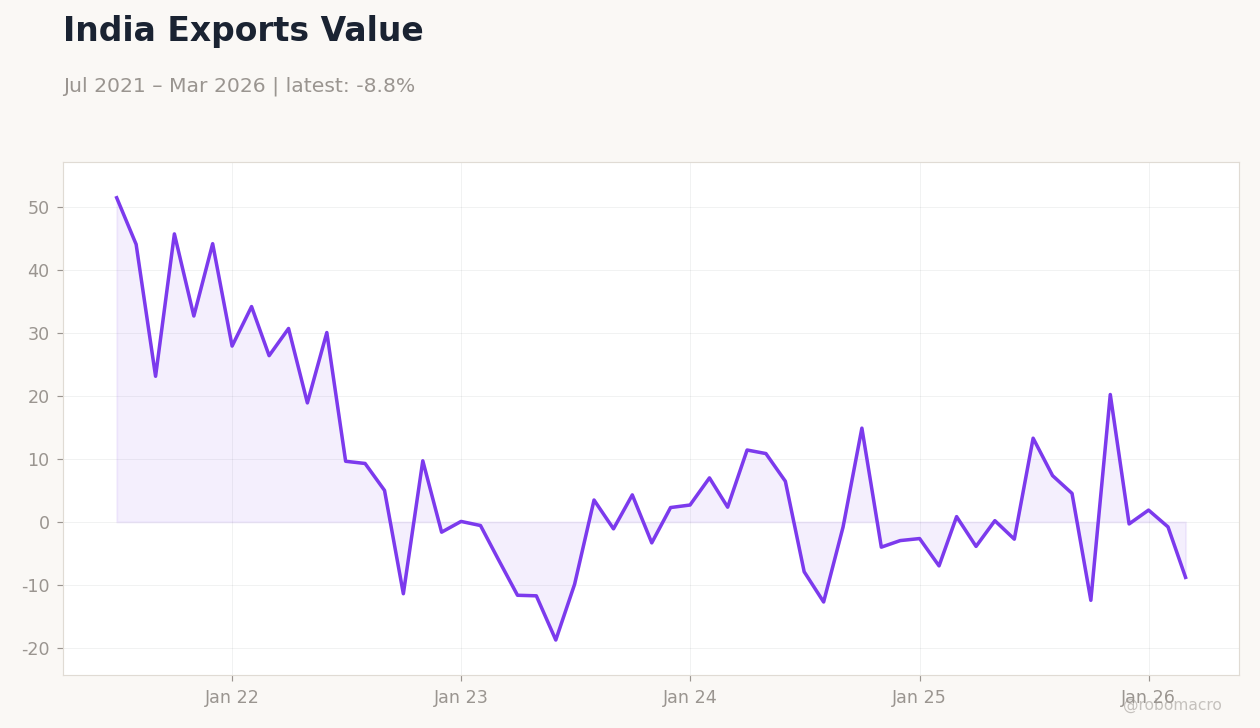

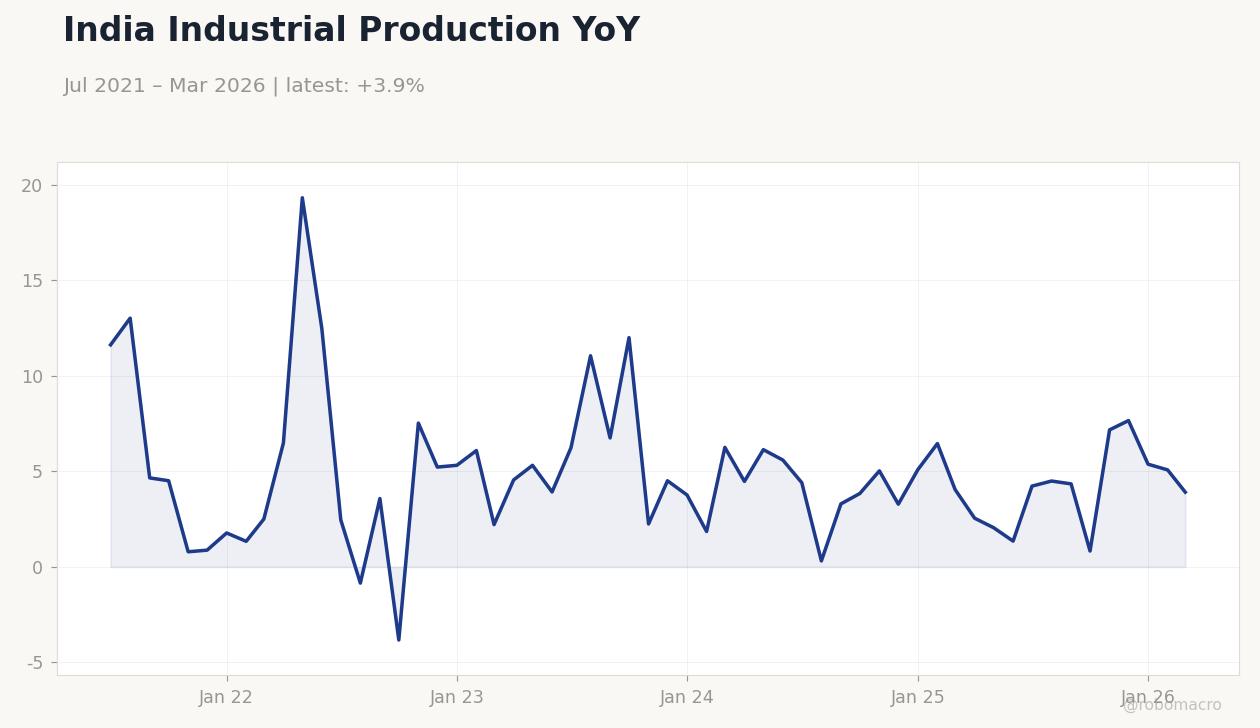

| Industrial Production Year-over-Year | 4.10 | 3.80 | - |

| Manufacturing Production Year-over-Year | 4.30 | - | - |

India Industrial Production YoY | Type: macro_line | YoY %: 3.911 (2026-03-01) | Range: -3.835–19.33 | Trend(5pt): 11.63,3.575,2.246,5.091,3.911

India Industrial Production YoY | Type: macro_line | YoY %: 3.911 (2026-03-01) | Range: -3.835–19.33 | Trend(5pt): 11.63,3.575,2.246,5.091,3.911

Today's Economic Events

| Data | Prior | Cons | Time |

|---|---|---|---|

| Friday (2026-06-05) | |||

| RBI Interest Rate Decision | 5.25 | 5.25 | 20:30 |

| GDP Growth Year-over-Year | 7.80 | 7.30 | 02:30 |

- India's forex reserves fell to a one-year low of $681.4 billion, prompting RBI intervention to support the rupee.

- Nifty 50 declined 1.50% to 23,547.75 while Sensex fell 1.44% amid broad equity selling.

- RBI is expected to keep the repo rate at 5.50% at the June 4 meeting despite growth resilience signals.

Yesterday's Recap

Indian equities closed sharply lower with Nifty 50 dropping 1.50% to 23,547.75 and Sensex falling 1.44% to 74,775.74. The rupee strengthened as USD/INR declined 1.09% to 95.00 on reported RBI intervention. Brent crude rose 3.13% to 94.93 while gold eased 1.00%.

Industrial Production and Manufacturing Production data were scheduled but actual prints remained unreleased. Forex reserves dropped to $681.4 billion in the week ended May 22, reflecting pressure from currency defense operations. Reliance and HDFC Bank shares fell 2.17% and 1.86% respectively.

The Day Ahead

Markets await the RBI Monetary Policy Committee decision on June 4 at 20:30 IST with consensus pointing to a hold at the 5.50% repo rate. GDP growth data for the latest quarter is due June 5 and is expected to print 7.3% year-over-year. May PMI manufacturing and services figures will also be monitored for signs of sustained expansion.

No other major domestic data releases are scheduled before the policy announcement. Traders will focus on any forward guidance regarding liquidity management and inflation risks.

Other Economic Notes

India scrapped cotton import duties for five months to support exporters facing supply shortages. Steel producers reported a surge in cheap Chinese imports, raising concerns over domestic margins. The central bank highlighted India's position as the fastest-growing major economy despite external shocks and higher US tariffs.

Food price risks have eased following the timely arrival of the southwest monsoon and improved Kharif sowing prospects.

Global Macro News

Renewed Middle East supply concerns lifted Brent crude prices and added to imported inflation risks for India. Higher US tariffs imposed in 2025-26 continue to weigh on export-oriented sectors according to RBI assessments. Chinese finished steel exports to India more than doubled in April, intensifying competitive pressure on local manufacturers.

Global risk sentiment softened after softer US data, indirectly supporting selective buying in Indian IT shares. <i>↓ p.2</i>