India Macro Daily(Beta Mode)

IIP Beats as RBI Decision Nears

Market Snapshot

| Asset | Level | Change |

|---|---|---|

| Nifty 50 | 23,405.60 | -0.33% |

| Sensex | 74,346.17 | -0.41% |

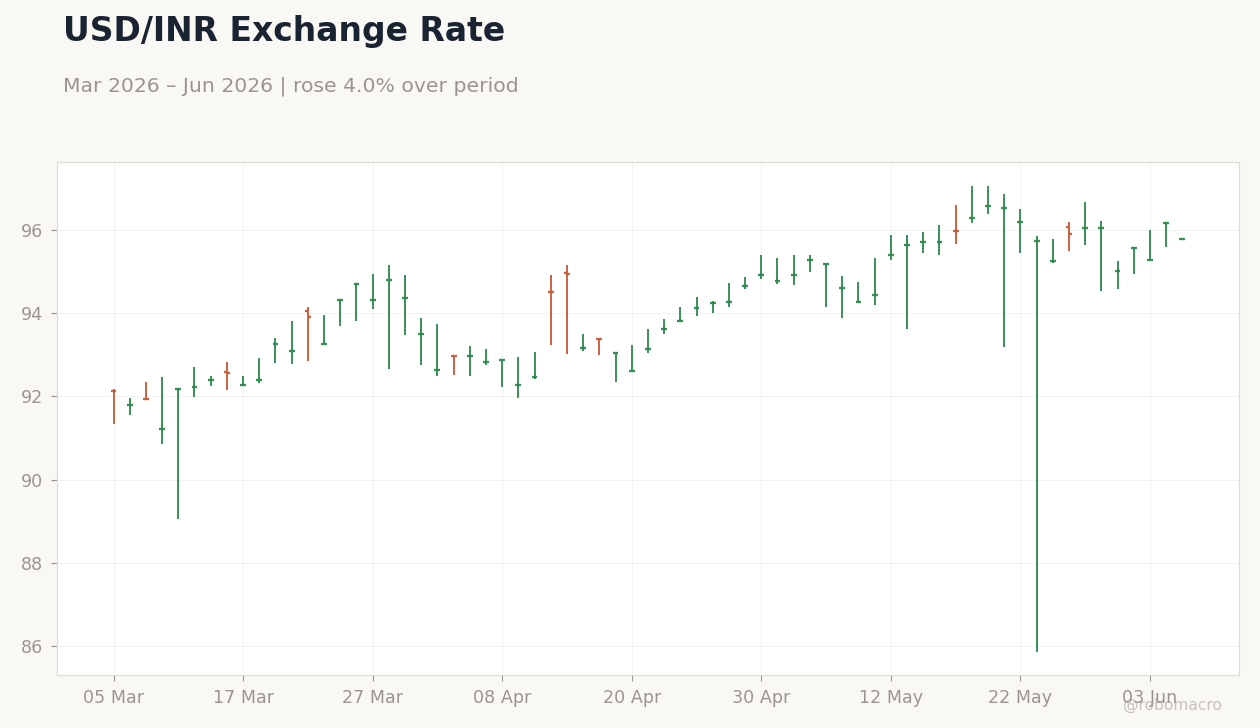

| USD/INR | 95.78 | -0.41% |

| EUR/INR | 111.25 | +0.20% |

| Reliance | 1,303.70 | -0.72% |

| HDFC Bank | 754.20 | +0.07% |

| Brent Crude | 95.05 | -2.82% |

| Gold | 4,489.80 | +1.20% |

| Bitcoin | 63,296.00 | -1.12% |

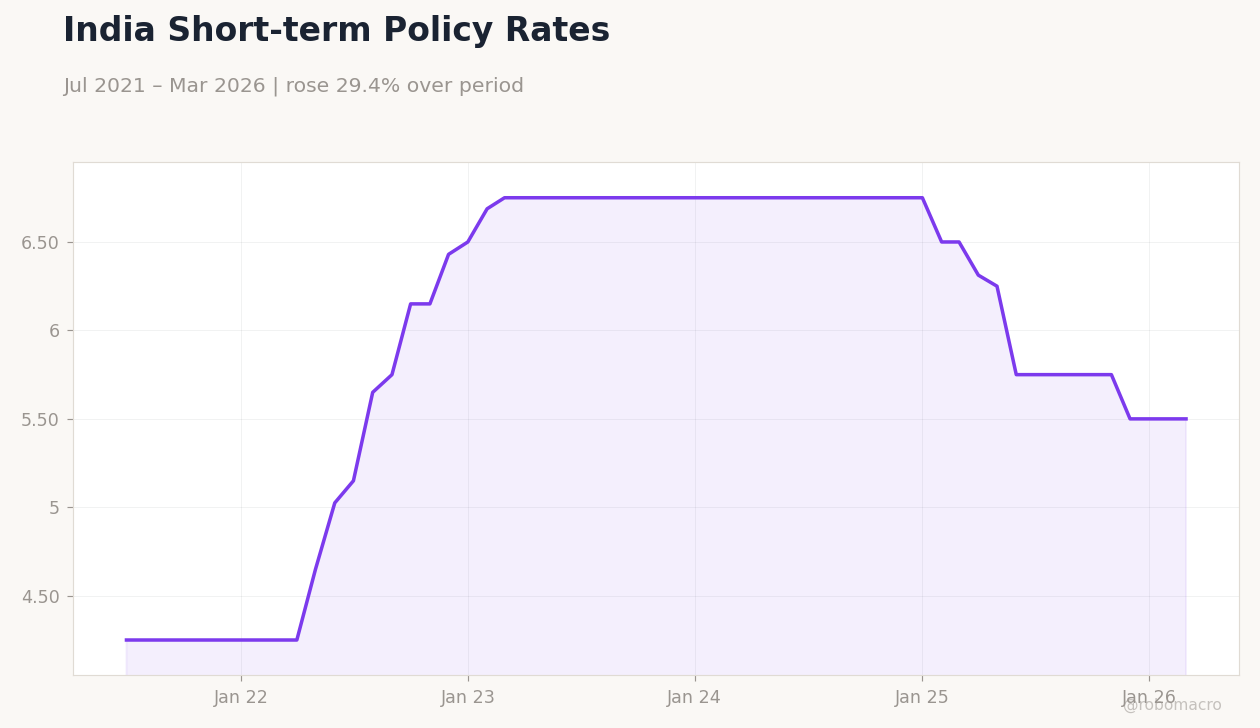

| India Short-term Rate | 5.50% | +0.00% |

| India Long-term Rate | - | - |

Prior Economic Events

| Data | Prior | Cons | Actual |

|---|---|---|---|

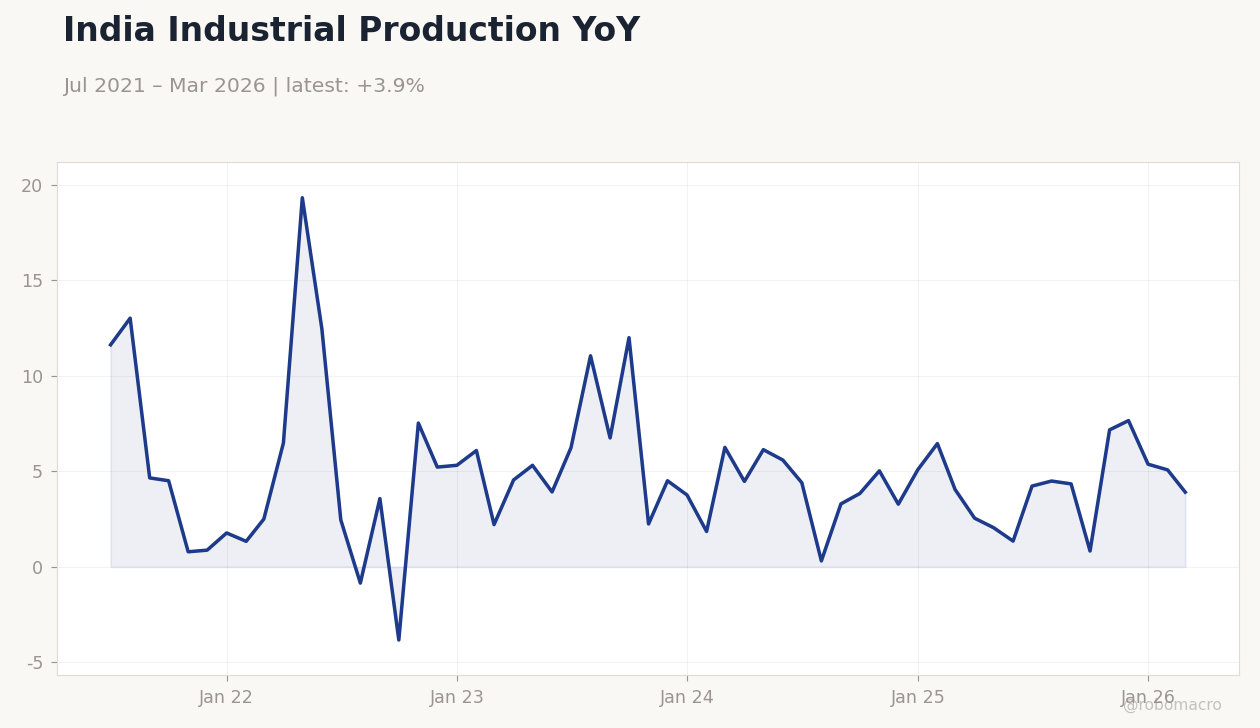

| Industrial Production Year-over-Year | 4.10 | 3.90 | 4.90 |

| Manufacturing Production Year-over-Year | 4.30 | - | 6.20 |

India Industrial Production YoY | Type: macro_line | YoY %: 3.911 (2026-03-01) | Range: -3.835–19.33 | Trend(5pt): 11.63,3.575,2.246,5.091,3.911

India Industrial Production YoY | Type: macro_line | YoY %: 3.911 (2026-03-01) | Range: -3.835–19.33 | Trend(5pt): 11.63,3.575,2.246,5.091,3.911

Today's Economic Events

| Data | Prior | Cons | Time |

|---|---|---|---|

| Friday (2026-06-05) | |||

| RBI Interest Rate Decision | 5.25 | 5.25 | 20:30 |

| GDP Growth Year-over-Year | 7.80 | 7.20 | 02:30 |

- Industrial production rose 4.9% YoY in April, beating consensus of 3.9%, while manufacturing output jumped 6.2%.

- Nifty 50 fell 0.33% to 23,405.60 and Sensex declined 0.41% to 74,346.17 ahead of the RBI policy outcome.

- USD/INR eased 0.41% to 95.78 as markets priced a hold at the 5.50% repo rate.

Yesterday's Recap

April industrial production printed 4.9% YoY, above the 3.9% consensus and prior 4.1% reading, with manufacturing output surging 6.2% from 4.3%. The beat reflected stronger factory activity but left RBI expectations unchanged. Nifty 50 closed at 23,405.60, down 0.33%, while Sensex finished at 74,346.17, off 0.41%.

USD/INR traded 0.41% lower at 95.78 amid steady intervention signals. Brent crude fell 2.82% to 95.05 as supply concerns eased, while gold rose 1.20% to 4,489.80 on safe-haven demand. Equity volumes remained moderate with limited follow-through after the data release.

The Day Ahead

The RBI MPC is scheduled to announce its interest-rate decision at 20:30 IST today, with consensus pointing to a hold at 5.50%. Markets will scrutinize the accompanying statement for any shift in the neutral stance or rupee guidance. GDP growth data for the latest quarter follows at 02:30 IST tomorrow, with expectations centered on a 7.2% YoY print.

Services PMI figures are also due and expected to confirm continued expansion near 59.8. Traders will monitor any liquidity operations announced alongside the policy.

Other Economic Notes

India’s services sector maintained momentum in May as the HSBC PMI climbed to 59.8 from 58.8, supported by robust domestic demand. A parliamentary panel flagged concerns over rupee depreciation and subdued private investment, urging policy support. Minister Prasada emphasized India’s position among the fastest-growing major economies despite global headwinds, citing progress in manufacturing and AI.

Monsoon rainfall running above the long-period average has eased food-price risks for the coming months.

Global Macro News

Elevated Brent prices near 95 dollars continue to feed imported inflation risks for India despite the recent pullback. US-Iran tensions added volatility to global risk assets and supported gold inflows into Indian markets. Gita Gopinath noted that allowing the rupee to adjust remains appropriate policy, reducing pressure for heavy intervention.

<i>↓ p.2</i>