India Macro Daily(Beta Mode)

RBI Swaps Steady Rupee, Lift Banks

Market Snapshot

| Asset | Level | Change |

|---|---|---|

| Nifty 50 | 23,242.10 | +0.52% |

| Sensex | 73,918.76 | +0.54% |

| USD/INR | 95.36 | -0.34% |

| EUR/INR | 109.92 | -0.32% |

| Reliance | 1,258.80 | -0.82% |

| HDFC Bank | 746.85 | +1.15% |

| Brent Crude | 95.13 | +4.02% |

| Gold | 4,093.10 | -3.92% |

| Bitcoin | 61,766.72 | +0.20% |

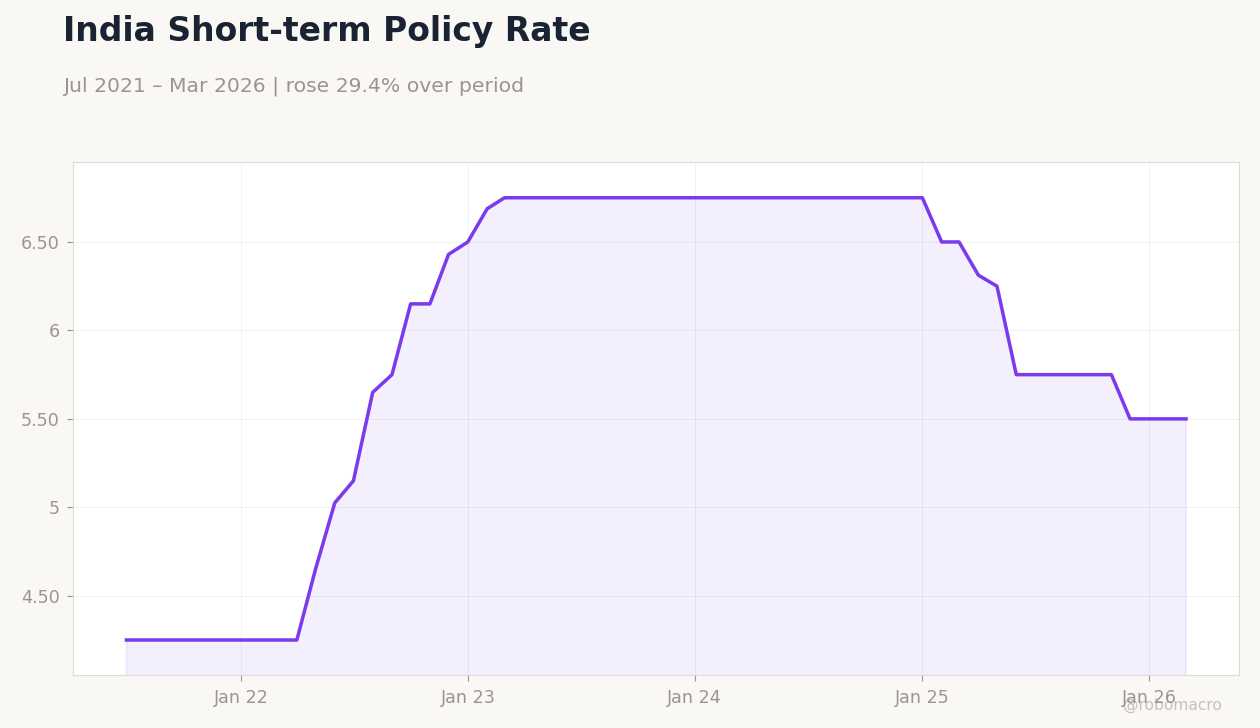

| India Short-term Rate | 5.50% | +0.00% |

| India Long-term Rate | - | - |

Prior Economic Events

| Data | Prior | Cons | Actual |

|---|---|---|---|

| Current Account Balance | -15,500m | -15,000m | 7,100m |

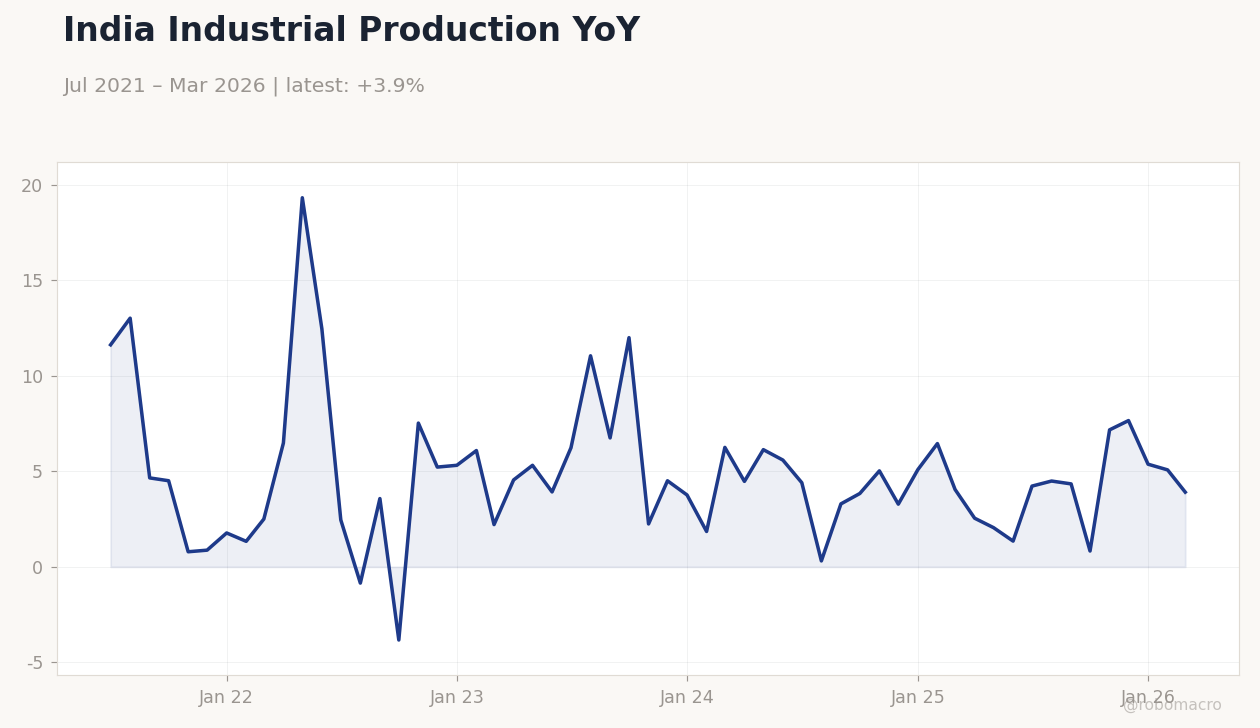

India Industrial Production YoY | Type: macro_line | YoY %: 3.911 (2026-03-01) | Range: -3.835–19.33 | Trend(5pt): 11.63,3.575,2.246,5.091,3.911

India Industrial Production YoY | Type: macro_line | YoY %: 3.911 (2026-03-01) | Range: -3.835–19.33 | Trend(5pt): 11.63,3.575,2.246,5.091,3.911

Today's Economic Events

| Data | Prior | Cons | Time |

|---|---|---|---|

| Friday (2026-06-12) | |||

| Inflation Rate Year-over-Year | 3.48 | 4 | 02:30 |

- Current account swung to $7.1 bn surplus in April, beating consensus by a wide margin and easing external pressure.

- Nifty rose 0.52% to 23,242 and Sensex gained 0.54% as banks rallied on RBI forex-swap facility.

- USD/INR fell 0.34% to 95.36 after likely RBI intervention and softer oil prices.

Yesterday's Recap

India posted a $7.1 bn current-account surplus in April versus an expected $15 bn deficit, reflecting stronger services exports and lower gold imports. Equity benchmarks advanced with Nifty 50 closing at 23,242.10 and Sensex at 73,918.76, both up more than half a percent. Banking stocks led gains after the RBI announced a forex-swap window to attract up to $65 bn in deposits.

USD/INR eased to 95.36 on the back of the RBI measures and Brent crude slipping from recent highs. Reliance fell 0.82% while HDFC Bank rose 1.15%. The short-term policy rate remained unchanged at 5.50%.

Market participants viewed the current-account print as confirmation that external balances remain manageable despite capital-flow volatility.

The Day Ahead

May CPI data due Friday at 02:30 ET will be the next key release, with consensus at 4.0% y/y after April’s 3.48% print. No MPC speeches or minutes are scheduled before the weekend. Traders will watch whether the RBI extends the forex-swap facility or adjusts liquidity operations.

Any CPI upside surprise above 4.3% could prompt modest repricing of the 5.50% repo rate path. Equity volumes are expected to stay elevated as banks digest the new deposit scheme details.

Other Economic Notes

Reliance and Meta announced plans for an AI-enabled data centre in Gujarat, underlining continued foreign interest in India’s digital infrastructure. FY26 GDP growth reached 7.7% on strong agricultural output and private investment, yet FY27 faces headwinds from potential drought and elevated oil prices linked to Iran tensions. FDI inflows in April hit $7.8 bn, led by services and software, supporting the external account.

The RBI’s $50 bn rupee-support package is viewed as a crisis-era tool revived to anchor sentiment.

Global Macro News

Escalating Iran-related conflict is raising India’s oil-import bill and widening the import cover requirement. <i>↓ p.2</i>