India Macro Daily(Beta Mode)

CAD Surplus, 3.93% CPI Lift Equities

Market Snapshot

| Asset | Level | Change |

|---|---|---|

| Nifty 50 | 23,622.90 | +1.99% |

| Sensex | 75,527.95 | +2.30% |

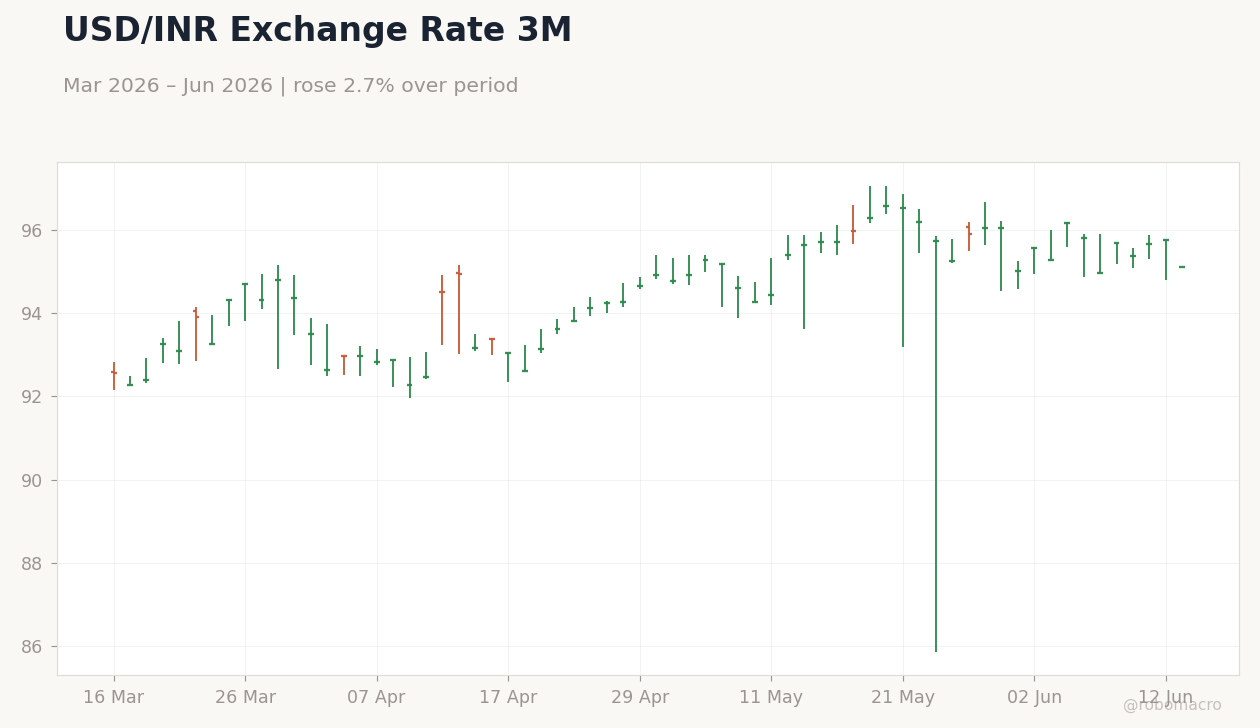

| USD/INR | 95.10 | -0.69% |

| EUR/INR | 110.44 | -0.30% |

| Reliance | 1,293.00 | +2.38% |

| HDFC Bank | 772.45 | +3.74% |

| Brent Crude | 83.59 | -4.28% |

| Gold | 4,323.60 | +2.58% |

| Bitcoin | 65,704.23 | +1.99% |

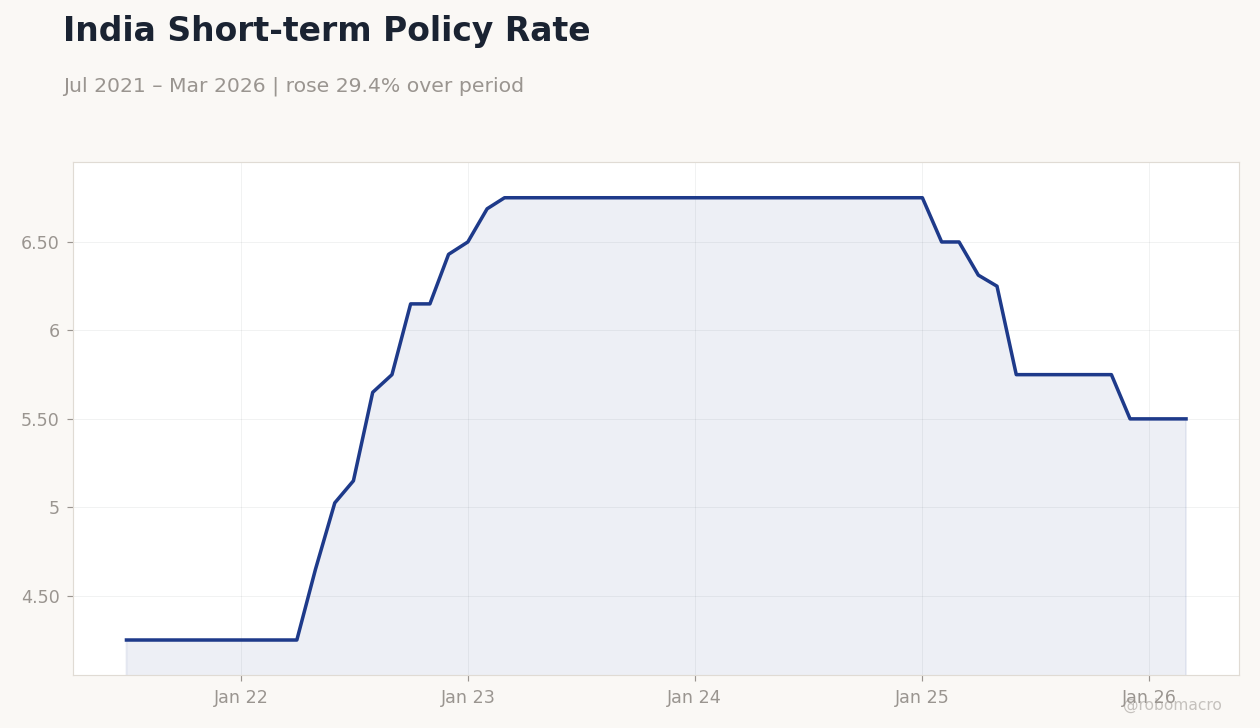

| India Short-term Rate | 5.50% | +0.00% |

| India Long-term Rate | - | - |

Prior Economic Events

| Data | Prior | Cons | Actual |

|---|---|---|---|

| Current Account Balance | -15,500m | -15,000m | 7,100m |

| Inflation Rate Year-over-Year | 3.48 | 4 | 3.93 |

India Short-term Policy Rate | Type: macro_line | Policy Rate %: 5.5 (2026-03-01) | Range: 4.25–6.75 | Trend(5pt): 4.25,5.75,6.75,6.75,5.5

India Short-term Policy Rate | Type: macro_line | Policy Rate %: 5.5 (2026-03-01) | Range: 4.25–6.75 | Trend(5pt): 4.25,5.75,6.75,6.75,5.5

Today's Economic Events

| Data | Prior | Cons | Time |

|---|---|---|---|

| No events available | |||

- Current account balance flipped to a $7.1 bn surplus in the latest quarter, beating consensus expectations of a deficit.

- May inflation accelerated to 3.93% YoY, remaining below the RBI’s 4% midpoint target.

- Nifty 50 climbed 1.99% to 23,622.90 while the rupee strengthened 0.69% to 95.10 against the dollar.

Yesterday's Recap

India reported a sharp turnaround in the current account balance to a $7.1 bn surplus against the prior quarter’s $15.5 bn deficit. May CPI printed at 3.93% YoY, up from 3.48% but below the 4% consensus. Equity markets responded positively, with the Sensex surging 2.30% to 75,527.95 and Nifty 50 advancing 1.99%.

The rupee firmed to 95.10 per dollar while Brent crude fell 4.28% to $83.59. Gold rose 2.58% to $4,323.60 per ounce amid safe-haven demand. Short-term rates held steady at 5.50%.

Reliance and HDFC Bank shares gained 2.38% and 3.74% respectively.

The Day Ahead

No major data releases are scheduled for today or tomorrow. Markets will monitor follow-through flows into equities and bonds after yesterday’s CAD and CPI prints. Traders will watch USD/INR for signs of further appreciation following the rupee’s 0.69% gain.

Global cues from US-Iran developments and oil price movements are expected to influence sentiment. RBI liquidity operations and any incremental FPI guidance will remain in focus.

Other Economic Notes

RBI measures are projected to support India’s FY27 balance of payments despite the recent CAD volatility, according to SBI Research. Foreign debt repayment capacity stands at 94% within a single day, underscoring external resilience. GDP growth for FY26 is projected at 7.6% by the RBI, with global risks flagged as the main downside.

FPI reforms could draw $50-100 bn into Indian debt markets over time. Banks have begun raising NRI deposit rates to attract foreign capital under RBI initiatives.

Global Macro News

Brent crude declined 4.28% to $83.59, easing imported inflation pressures for India. Gold advanced 2.58% to $4,323.60, reflecting ongoing safe-haven buying. Hopes of a US-Iran deal supported broader risk appetite and lifted Indian equities.

Bitcoin rose 1.99% to $65,704.23, tracking global crypto sentiment. Foreign bond inflows face limits in moving India’s $1.5 tn G-Sec market despite incremental RBI opening measures. <i>↓ p.2</i>